This year promises to be unlike any other. Yes, I say that every year … but this time change really does seem to be upon us. As we kick off the new year, let’s take a step back and look at the broad themes of last year that are likely to continue into 2017.

Rising Earnings

With so much attention focused on the presidential election, many investors did not realize that corporate earnings recently climbed out of a five-quarter slump. According to Thomson Reuters, third quarter, 2016 earnings are expected to rise 4.3% from prior year levels. Excluding the energy sector, that figure is closer to 8%.

Revenues followed suit, but weren’t up as much as earnings, rising 2.6% during the third quarter. The gains here are widespread, with 9 of the 11 sectors expected to see revenue growth after all is said and done.

Listen to Tax Cuts, Earnings, and Expectations

The resumption of earnings growth is currently expected to continue, with earnings expected to rise 6.1% in Q4, 13.8% in Q1 2017, 11.9% in Q2 2017, and 10.2% in Q3 2017 (Thomson Reuters figures). Of course, analysts are notorious for their rose-colored glasses, so take this with a grain of salt, but it gives you an idea of the street’s expectations.

Also keep in mind that Trump’s policies, wherever they land, will play a huge role in the outlook for corporate profits. More on this below.

Continued US Economic Growth

Since the recession ended in 2009, the economy has grown at about a 2% rate, marking the slowest average rate of expansion since the mid-1900’s. That paltry growth hasn’t held stock prices back, however, and they have more than tripled since their 2009 lows.

Recent figures show that 3rd quarter GDP rose at a 3.5% annual pace, which is the strongest quarterly growth rate in two years. But a strong quarter does little to lift the long-run trajectory which, as mentioned, sits near 2%.

Many economists expect the strong 3rd quarter reading to be an outlier figure, with 4th quarter GDP growth expected to come in around 1.6% - 1.9%. Longer run forecasts for economic growth during 2017 currently sit near 2.4%.

This suggests an economy similar to the one we’ve been experiencing, with growth, but not an abundance of growth. Once again, things could change drastically based on the new administration, but that’s the current view.

The first estimate of fourth-quarter GDP will come on January 27th.

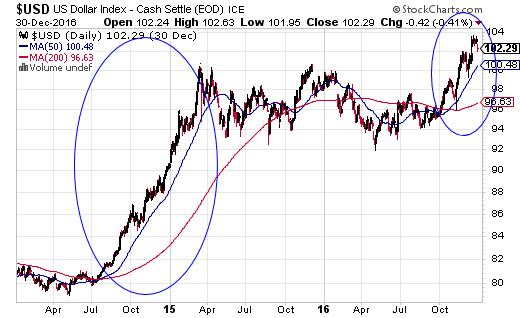

The Strong Dollar

The dollar traded flat to lower during most of 2016, but that all changed during the 4th quarter. As you can see in the chart below, the dollar resumed its ascent, rising above the 100 level for the first time since 2003.

The greenback has been aided by a US economy that is stronger than its peers and interest rates that are higher than most other developed nations. These two factors, combined with a growth-oriented incoming administration, have caused the dollar to surge higher.

A strong currency is likely to be a factor during most, if not all, of 2017, and that may have negative consequences on some parts of the market.

Recall that the recent approximately 2 year period of economic and financial market malaise was preceded by a swift rise in the dollar during late 2014 and early 2015 (see chart below).

This massive shift in the trade-weighted value of the dollar was responsible for putting downward pressure on the US economy and crimping the profits of US-based multinational companies. It also put strong downward pressure on oil and commodities, helping to create the disinflationary environment we found ourselves in.

The dollar is likely to play a key role in 2017 and will continue to be one of the major bogeys investors will need to operate around. This is one reason we’ve seen the gains in domestic-oriented small-cap companies far exceed those of large-cap international firms during the post-election rally. The Russell 2000 is up 13.5% since Nov. 8th vs. 4.5% for the S&P 500.

In a stable equilibrium style dynamic, improvements to the underlying US economy are likely to be met with continued increases in the value of the dollar, which will work to siphon US growth off to some of our trading partners with weaker currencies. Too bad we can't have our cake and eat it too.

Inflation and Interest Rates

This is perhaps where some of the most significant changes will take place this year.

As most of you know, the Federal Reserve has been unable to hit its inflation target of 2% since the beginning of 2012. And even then, core personal consumption expenditures (the Fed’s preferred gauge), only reached 2.1% for a couple of months before retreating below that mark. Prior to 2012, the last time core PCE was consistently above 2% was during 2008, in the heart of the financial crisis.

As a result of below-target inflation levels, the Fed has remained very accommodative until just recently. Executing just two rate hikes since the financial crisis, the Fed is poised to continue its tightening cycle during 2017.

Of course, this will depend on how inflation fares, but so far it appears that inflation may rise materially this year. Analysis performed by DoubleLine Capital suggests that if oil is at /barrel one year from when it bottomed (last February), then headline CPI will begin to approach 3%. That’s a far cry from where we are now, with headline CPI currently at 1.7%.

If we do see a move to anything near a 3% CPI figure, you can bet that bonds will continue to sell off and interest rates will rise to accommodate lenders for the loss of purchasing power. Be watchful here.

Interview Shifting Landscapes

One last consideration is that a rise in inflation may cause investors to shift into riskier assets that are better suited to deal with rising prices. While there are offsetting effects, faster erosion of purchasing power could induce some investors who have been sitting in cash or low-yielding assets to move those funds into riskier assets, such as equities, whose underlying companies can pass on those rising costs to consumers.

Prospect of Tax Cuts and Fiscal Stimulus (and Protectionist Policies)

This, of course, is the big question mark of 2017. Just what does our president-elect have up his sleeve? And what can he get passed through Congress?

Since the election, the market narrative has been one of the reduced corporate taxes, reduced regulation, and increased fiscal spending.

All of these have been priced into the market to some degree, but how fully we do not know. We also have no guarantees as to whether any of these will actually come to fruition, though it’s likely they all will in some form or another.

But while the market has looked at proposed changes with a sense of optimism, we must be aware of the de-globalized world we may be entering. Trump’s focus on “America first” has the possibility of inducing other countries to take an “us first” approach as well. If this is the case, we could see other countries take retaliatory measures, including the establishment of further protectionist policies.

What lies ahead is anyone’s guess; the only guarantee is that it’s going to be an exciting and unique year. Will we see a return of animal spirits and a third-phase upside blowoff? Or will some snafu send us, and the rest of the world, into the grips recession and deflation? Only time will tell, so stay tuned.

The preceding content was an excerpt from Dow Theory Letters. To receive their daily updates and research, click here to subscribe.