Leadership is an important consideration in any type of market, bull or bear. When market leadership is thin and quickly changes direction, it can signal a shift in the tone of the overall market.

The rally that has unfolded in recent months has been changing in character. Originally, the thrust began as a reflation trade, as signs of disinflation/deflation began to fade and global bond yields crept higher. The timing of this coincided with the election, which brought with it hopes of tax cuts, deregulation, and infrastructure spending. This boosted the prospects (and share prices) of cyclical companies – those that need an improving economy to do well.

But then both of these narratives began to fade. Inflation and economic data weakened, and it caused bond yields to fall from their highs near 2.6% to current levels around 2.2%. At the same time, it became clear that very little on Trump’s agenda could be counted on … at least for now.

Don't miss Has the Tech Bubble Finally Burst?

This led to another shift in leadership, as technology stocks took over the show.

Most tech firms, at least those that have been leading the way higher, are secular growth stories. This means that these firms don’t need a robust economy to do well. Instead, the products and services they sell are so unique that they’re almost always in demand.

You know many of the names I’m talking about … Facebook, Amazon, Google etc. These guys can grow revenues and earnings at a fast clip almost regardless of how the economy is doing. Of course, a strong economic backdrop doesn’t hurt, but it’s not a prerequisite.

As expectations about surging economic growth began to cool, many companies in the tech sector became direct beneficiaries of money that left economically sensitive areas of the market.

Consider this: As of last Friday, five stocks (Apple, Amazon, Alphabet, Facebook, and Microsoft) accounted for 41% of the S&P 500’s market cap gains for the year. That’s what we call “thin leadership” and it’s often a bad sign for the broader market, as it suggests that major indexes are being propped up by a handful of names while the rest of the market deteriorates.

But is that really what’s happening? And is the recent selloff in tech a canary in the coal mine for the broader market?

Let’s start with this ominous chart, which shows trading volume for the QQQ (an ETF that tracks the Nasdaq 100). As you can see, last Friday saw a major spike in volume that coincided with the tech sector of the S&P falling nearly 3%.

As annotated in the chart, these anomalous high-volume days have been associated with troubling developments, whether it be precursors to the financial crisis or the ETF meltdown in 2015. This latest bout of trouble, which began Friday, has already been dubbed the “tech wreck.”

One interesting thing to note is that the selloff in tech has already gone global. Following Friday’s declines in US markets, technology sectors around the globe got hit early Monday. Tencent, China’s largest social media company fell 2.5% in Hong Kong, while tech stocks in Europe’s Stoxx 600 fell more than 3%.

So is the tech wreck going to cause an ensuing pileup, taking down other sectors with it? Or is this more likely a case of profit taking?

Check out Ralph Acampora: Dow Theory Divergence Signals Caution

To answer that, it helps to have an understanding of tech’s recent performance, relative to its peers, and also an understanding of the earnings outlook for the sector.

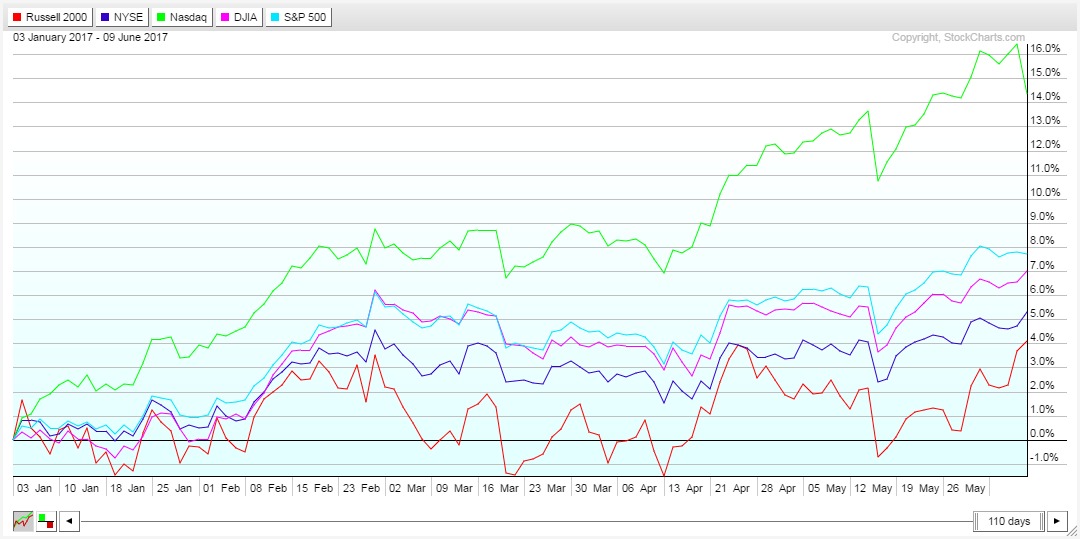

The chart below compares relative performance across the major averages going back to the start of 2017. As you can see, while all the averages experienced growth through the end of February, the Nasdaq has been the only one to continue chugging significantly higher.

Prior to Friday’s declines, the tech-heavy Nasdaq was up over 16% year-to-date. That’s a rather incredible feat when you consider that we remain in a 2% economy, but then again much of tech is secular, not cyclical.

With gains in the first half of the year so strong, valuation levels at historical extremes and volatility so low, it’s only natural to expect some profit taking. In my opinion, that’s what we’re seeing here, along with the help of algorithmic trading.

Just as we use technical tools to try and identify the primary trend, and invest accordingly, many firms out there employ algorithmic trading to do the same thing, just on a much shorter timeframe. These programs will use any number of inputs to automatically execute trades and seem to have a habit of exacerbating moves in the market, causing them to be more violent than they would have been otherwise. I think this is something we just need to get used to as more and more trading becomes automated.

There are a couple of other signs that make me think this is more likely to be a temporary phenomenon rather than the start of a much deeper correction. One is that the tech sector is still expected to report the second highest earnings growth for the 2nd quarter, at 9.3% (FactSet). This implies that from a fundamental basis the case for tech has not collapsed.

The other has to do with market breadth.

A look at both the NYSE Advance-Decline line as well as the “common-stock only” version – which excludes fixed income and a number of other issues – shows that participation in this rally remains widespread. Both indexes continue to notch new highs and remain above their respective 50 and 200-day moving averages.

If we were seeing a breakdown in market breadth, I would be much more concerned about the selloff in tech, expecting it to expand to other areas of the market. But since this seems to be localized selling in the hottest part of the market, I’m willing to keep a positive outlook for now and attribute most of this move to investors wanting to lock in profits after a solid run.

Taking a step back and looking at the broader landscape, David Stubbs, global market strategist at J.P. Morgan, recently said, “This era we’re in now of resilient but slow growth and low inflation is one that would favor tech.” I tend to agree and think that tech will likely rebound quickly and continue to be one of the top performing sectors in the months ahead.

The preceding content was an excerpt from Dow Theory Letters. To receive their daily updates and research, click here to subscribe. Matt is also the Chief Investment Strategist at Model Investing. For more information about algorithmic based portfolio management, click here.