Every month, pundits comment on average wages. But median wages best explain how the Fed's policies crucify workers.

The meme of the day is wage growth is accelerating.

I disputed that notion on February 7 in Acceleration in Wage Growth is a Statistical Mirage.

On February 16, I reported Congratulations Workers! You Make One Penny More Than a Year Ago.

That penny more a year is by the hour, in "real" inflation-adjusted terms. The calculation is from the BLS.

Nonetheless, the Fed is not happy with wage destruction. Various Fed presidents seek still higher inflation.

Inflation Targeting

Instead of using an inflation target of 2%, San Francisco Fed President John Williams proposes the Fed use a price-level target, that would allow inflation to run higher during expansions to make up for prior shortfalls.

We need that discussion, but in the opposite sense, because the Fed’s insistence inflation in a disinflationary world has seriously harmed median and average wage earners.

Occupational Employment Statistics (OES) from the BLS supports this view.

The following charts are from OES data downloads at the state and national level coupled with additional CPI data from the BLS.

Data for these charts are from May 2005 through May 2016. Those are not arbitrary dates.

The latest OES data is from May of 2016 and prior to May of 2005, the OES used varying months. Having all yearly data from May allows easy comparison of wages vs. year-over-year CPI measurements.

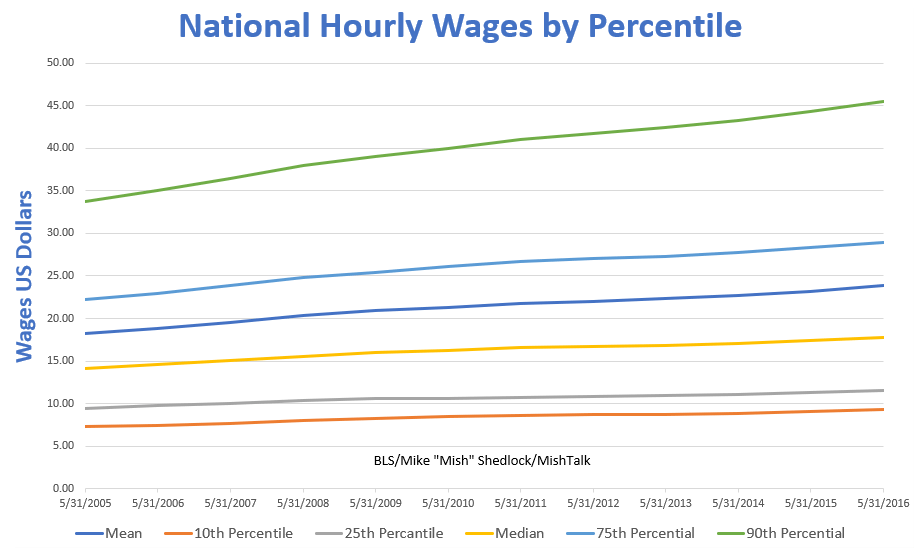

National Hourly Wages

Wage Differentials Mean vs. Median Hourly Wages by State

Every month, analysts track the monthly jobs report for “average” wage increases. Such analysis is misleading because most of the benefits go to the top tier groups.

This behavior is not unexpected, but it makes it very difficult for the bottom half of wage earners, who do not own a house, to buy a house.

Who Can Afford a Home?

The median wage rose from .15 in 2005 to .81 in 2016, a percentage increase of 25.9%.

The median new home price rose from 8,300 in 2005 to 5,400 in 2016, a percentage increase of 46.9%.

Rising Tide Lifts All Boats?

Some claim that a rising tide lifts all boats but, the median wage earner is falling further and further behind. This contributes to asset price chasing and “better buy now” philosophies as happened in the housing bubble years.

Inflation-adjusted charts show the situation is even worse.

“Real” Year-Over-Year Percentage Increases

The chart shows “real” inflation-adjusted median wages declined in 2007, 2009, 2011, 2012, 2013, 2014, and 2015.

Mean inflation-adjusted wages declined “only” in 2007, 2009, 2011, 2012, and 2013.

Disturbing Results

Congratulations to the top ten percent whose real wages rose 8 times in 11 years. At the 75th percentile level, the score is 6-5.

It’s simply too bad for the median and bottom twenty-five percent whose real wages fell seven times in 11 years.

Don’t Blame Corporations

Many blame “greedy” corporations for wage stagnation.

Corporations have a responsibility to do what is best for shareholders, not employees. Sometimes those interests align and sometimes they don’t.

Don’t Blame Minimum Wage Laws

Minimum wages are also not the problem.

There is no reason to expect minimum wages to keep up with home prices. Home prices are not even in the CPI.

The Fed ignored rising home prices from 2003-2006, and they did it again recently. Central banks fail to learn from past mistakes.

Asset prices are in another massive bubble with plenty of blame to share.

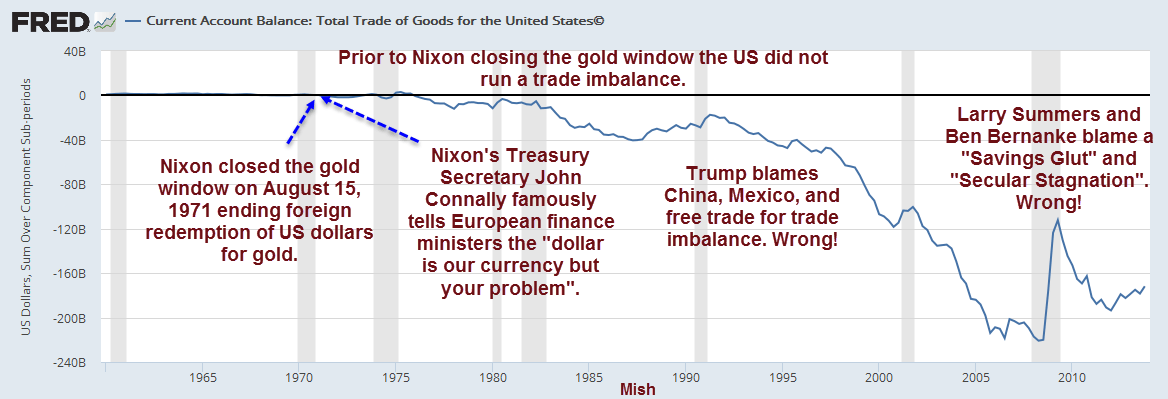

Blame the Fed, Congress, Nixon

- Blame Nixon for closing the gold window in 1972; that allowed Congressional deficit spending at will.

- Blame the Fed for insisting on 2% inflation in a technological price-deflationary world.

- Blame Congress for massive fiscal deficits every year.

- Blame fractional reserve lending for being the enabler of trillions of dollars worth of mortgage and other loans, constituting money borrowed into existence chasing rising asset prices.

- Blame the media and academics for parroting the ridiculous notion that there is a benefit to rising prices. In the real world, standards of living improve when goods are cheaper.

Price Deflation Not a Problem

The Fed desperately seeks more inflation, but a BIS Study on the Historical Costs of Deflation shows routine price deflation is not a problem.

According to the BIS, “Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive.”

Counterproductive Fed Policy

The Fed’s policies are extremely counterproductive. To produce 2% inflation in a price-deflationary world, the Fed helped inflate asset prices to the extremes seen in 2007, 2000, and 1929.

Another Fed-induced asset-price bust is baked in the economic cake.

Meanwhile, a debate is taking place why economic growth is so low.

Secular Stagnation Thesis

In 2014 economist Larry Summers proposed Secular Stagnation is what ails the economy. Summers proposed “It may be very difficult for investment to absorb all saving.”

In 2017, Summers doubled down on his secular stagnation thesis. He blames austerity for the lack of inflation. His purported cure is a more public investment.

Savings Glut Thesis

In 2005, former Fed chairman Ben Bernanke proposed economic growth was slow because of a Savings Glut.

Bernanke defines the glut as an imbalance between savings in China and consumption in the US.

Quick Rebuttal of Bernanke, Summers

To Larry Summers, I suggest that deficit spending is out of control globally. If more public spending was the answer, Japan would be the shining beacon of global excellence.

To Ben Bernanke, I say, "Let’s not confuse “savings” with monetary printing. In the classic sense, savings = production minus consumption."

The bulk of what’s been “produced” is dollars out of thin air, yuan out of thin air, euros out of thin air, and yen out of thin air.

In their analysis of “savings” both Summers and Bernanke ignore the massive buildup of debt that has occurred.

To the extent there is an imbalance between the wealthy and not wealthy, Fed policy exacerbated the problem.

History Lesson

The Fed bailed out the banks in 2000. At that time banks were troubled by soured dotcom bubble loans and loans to foreign countries like Argentina.

The result was a housing bubble, as Greenspan kept interest rates too low, too long.

In 2009, the Fed bailed out the banks when the housing bubble burst.

Since then, the Fed’s inflationary policies benefited the asset holders, the banks, and the top 10% of wage earners at the expense of everyone else.

Current Account Balance

Credit Explosion

Here is an excellent article on President Nixon: The Man Who Sold the World Fiat Money.

Prior to Nixon's closing the gold window, countries could not run massive fiscal deficits for years on end without hiking interest rates.

Summers believes we need still more public spending stimulus. Japan provides convincing evidence that Summers’ thesis is false.

Discussion Needed

The Fed’s inflation policies are contrary to BIS findings, contrary to common sense, and contrary to the real-life results of median-wage earners falling further and further behind.

Please, let’s have a genuine discussion regarding the Fed’s inflation policies.

That discussion needs to incorporate ideas outside the Fed’s “group-think” box of more inflation, secular stagnation, and savings glut theories, all of which are easily proven wrong.

Discussion Rejected

The Wall Street Journal rejected this Op-Ed submission via a robot or a non-thinking person imitating a robot.

I know this because I sent in an inquiry to Editorial Features Editor, James Taranto, asking to speak with him about the rejection, and guess what.

My short Email request to speak to Taranto, not a submission, received the identical rejection notice. Thank you, WSJ!

My submission title was "Fed’s Inflation Policy Destroys the Median Wage Earner". It started with the discussion of inflation targeting. The wage acceleration mirage and the BLS penny admission happened after my op-ed submission.

At least the WSJ responded. The Financial Times, which claims to get back within three days, didn't bother.

Mainstream media does not want to discuss what's happening and why. They already "know". Nearly everyone but the Austrians believes "secular stagnation" is caused by "savings gluts".

Besides, criticisms of the Fed, Larry Summers, or Ben Bernanke would ruffle too many feathers to be published.