Originally posted at Briefing.com

The reflation trade has taken hold of the stock market again, and, to a certain extent, it has taken hold of the Treasury market.

Hear Stress-Test of US States Yields Troubling Results

The reflation hold on the Treasury market is plain to see at the front end of the curve, where the yield on the 2-yr Treasury note has soared 32 basis points since September 11 to 1.58%. Similarly, the yield on the 10-yr Treasury note has jumped 38 basis points over the same period to 2.43%.

That adjustment, however, isn't a purebred reflation trade. If it were, the yield on the 10-yr Treasury note would be much higher and the spread between the 2-yr note yield and the 10-yr note yield would be much wider.

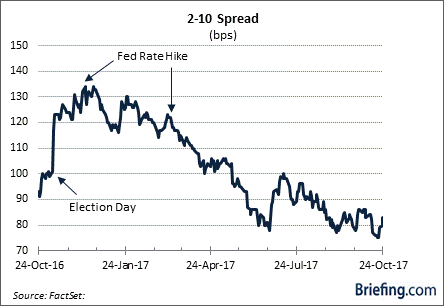

Melting Away

As it so happens, the 10-yr note yield is five basis points less than where it started the year while the spread of 85 basis points between the 2-yr note yield and the 10-yr note yield is 37 basis points less than the spread seen at the start of the year and 49 basis points less than its post-election peak.

The curve flattening since the start of the year has been driven by the 2-yr note yield. It is up 32 basis points since the end of 2016. The entirety of that shift has occurred over the last six weeks, too, which is when the market has priced in the prospect of a third rate hike this year at the December FOMC meeting.

Additionally, the market seems to have acquiesced to the notion that a synchronized pickup in global growth, and the possibility of lower tax rates in the US, make further rate hikes in 2018 a likely proposition.

The reflation narrative, however, seems to have gotten lost in translation at the back end of the curve where yields remain compressed.

Sure, they have risen in recent weeks, yet the narrowing spread between the 2-yr note yield and the 10-yr note yield is not the dynamic one typically associates with a view that stronger economic growth will produce higher inflation.

Party Pooper

Why is the 10-yr note yield acting like the party pooper at the reflation party? The answer is debatable.

Some think it stems from the Bank of Japan and the European Central Bank maintaining ultra-low policy rates and aggressive monetary policy accommodation, which is fueling a continuation of interest-rate differential trades

Some think it is a demographic factor, with retiring baby boomers emphasizing the preservation of capital over a return on capital

Some think there is a bit of defensive-oriented gravitas to the move as market participants fret about the possibility of a big correction coming for the stock market

Some think it is a simple reflection of the view that inflation is under control and will remain under control

Some think it is a sign that the market believes the Federal Reserve is on course to make a policy mistake by raising rates too much, too soon, and choking off economic growth prospects

And some think it reflects an ingrained view that the US economy is destined to remain in a low-growth stupor for some time due to weak productivity and labor force growth.

What It All Means

The spread between the 2-yr note yield and the 10-yr note yield hit a 10-year low last week, yet it remains a good bit away from inverting, which many market watchers construe as a harbinger of weak economic growth and possibly a recession.

All in all, the 2-10 spread is a peculiar relationship in the context of a market that is courting the reflation model.

The fact that the spread has been narrowing at a time when economic growth expectations are picking up is out of line with the natural order of a reflation trade.

What you have is a yield curve that is reflecting reflation without the inflation.

It's a sure-minded view of matters that could give way to quite a pain trade at the back end of the curve if inflation rears its ugly head.