US pension funds do not have a pretty probability path going forward, a Moody’s report pointed out. The potential that certain pension liabilities increase at a time when reliance on pension funds avoiding major investment losses is a demographic and investment management issue. What about the situation right now? Moody’s starts out by stating: US public pension funds’ adjusted net pension liabilities (ANPLs) surpassed $4 trillion nationwide in 2016, reflecting poor investment results and declining discount rates.

Moody’s says pension fund investment returns are more critical now than ever

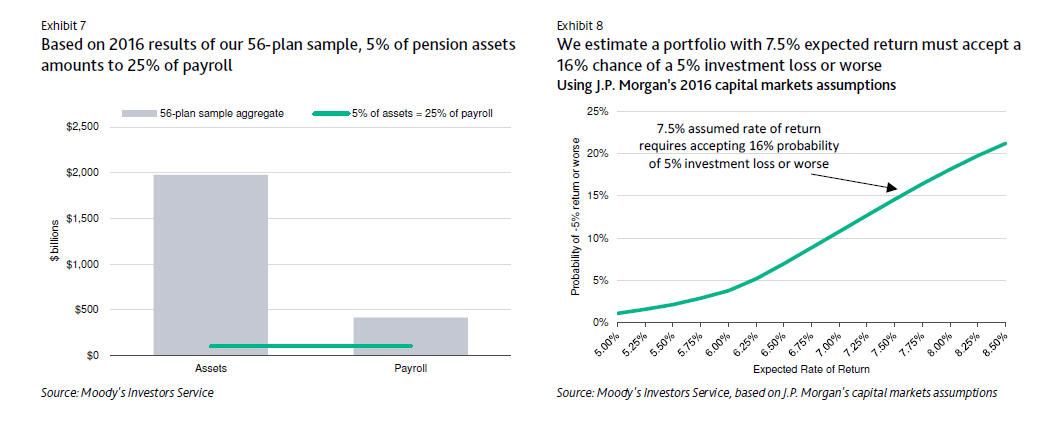

Moody’s: Just a 5% Loss in US Pension Funds Investment Returns Equates to 25% of Payroll

Examining forward-looking modeling, Moody’s analysts Thomas Aaron and Timothy Blake see a probability path filled with potholes for pension funds, including investment performance.

Pointing to a 5% loss in pension returns equating to “increases unfunded liabilities by an amount equal to 25% of payroll,” the June 20 report points to a potential 3 billion shortfall. “Pension fund investment performance has never been more critical to government credit quality.”

Read Don Coxe on Brewing US Pension Crisis, Stimulus vs. Rising Rates

This “budget shock” scenario carries a 16% probability path weighting, pointing to a heavy reliance on “allocations to volatile investments.”

Those “volatile investments” were not identified, but the process assumed a Capital Asset Pricing Model most often associated with the stock market:

To assign the probability of a 5% investment loss materializing, we derive an “efficient frontier” using J.P. Morgan’s capital markets assumptions. The frontier provides the expected volatility, or standard deviation, for any given level of expected return. For our sample, the weighted average assumed rate of return was 7.5%, which corresponds with expected volatility of 10.7% on the frontier we derived, based on 2016 capital markets assumptions. Assuming a normal distribution, the probability of a -5% return or worse given these return and volatility expectations is 16%

The problem of even a small 5% drop in investment performance comes as a pension shock could be in the offing.

See The Public Pension Time Bomb Is Starting to Explode

Moody’s: Retirement Liabilities Could Rise, But Also Modulate Depending on Interest Rates

Looking at both upside and downside probability paths – and assigning a different weighting to each – Moody’s notes that Net US Pension funds Liabilities (NPLs) could increase by as much as 59% in the worst case scenario. Such costs might only have potential to drop by 1%.

Reported NPLs are a mirror of the use of discount rates that are linked to future assumed rates of investment return, the report noted, pointing to an approach that “tends to significantly understate the point-in-time market value of government pension promises to employees.”

Check out Brian Reynolds: How Public Pensions, Not The Fed, Are Driving Epic Bull Market

Looking at NPLs offer only a partial glimpse, as the more positive adjusted net pension liabilities (ANPLs) have a tighter range of outcomes with less fat-tail exposure. Moody’s estimates a 13% upside to scenario liabilities decreasing – due largely to interest rate fluctuations – while such costs might only increase 7%, the report predicted.

With all the latest news about the dire state of US pension funds, it might be time to start saving up your money for retirement.

By Mark Melin