You can only stretch a rubber band so far before it snaps back or is torn, so too is the case with government indebtedness. There eventually comes a point when the road ends and the can hits a brick wall. It appears that Japan is rapidly approaching that brick wall and there are two likely outcomes. One option is that the bond vigilantes revolt and yields on Japanese debt spike or the second option is a massive debt monetization by the Bank of Japan (BOJ). Given the massive amount of debt relative to the Japanese economy and associated interest payments on the debt, Japan can’t afford a sharp rise in yields. Thus, it appears the BOJ is likely to step in and monetize the debt and the currency markets may be signaling this very outcome.

Japan’s Debt Mountain Time Bomb is Here

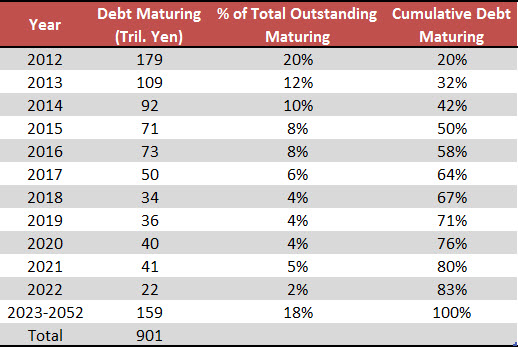

Japan has over 900 trillion yen in sovereign debt outstanding and the bulk of that is set to mature in the next 2.5 years. In the last half of 2012 alone Japan has 20% of their total outstanding debt mature as 178 trillion in Japanese sovereign debt is maturing with 108 trillion in yen due next year. The maturity of Japan’s outstanding debt is show below and as is clearly visible, Japan will be rolling over a tremendous amount of debt in the next few years.

Source: Bloomberg

As the table below highlights, by the end of 2015 Japan will have to roll over half their entire debt outstanding, or just over 450 trillion in debt.

Source: Bloomberg, PFS Group

The large percentage of Japanese sovereign debt maturing over the next few years could not have come at a worse time as Japan’s Baby Boomers retire and pension funds begin to make payouts rather than accumulate assets. For the first time in nine years Japan’s Government Pension Investment Fund (GPIF), the world’s largest pension fund, sold a net 443.2 billion Yen of Japanese government bonds (JGB) in its fiscal 209 to March 2010 as rising benefit payouts exceeded pension reserves (article link). This is a major concern for Japan as the GPIF owns nearly 12% of all outstanding JGB and has been a major buyer of JGB for decades and is now transitioning to a seller of JGB and plans to sell 8 billion worth of assets between 2012-2013, a large portion of which will include JGB to generate cash to meet pension payouts (article link).In the fiscal 2010-2011 year the GPIF sold 4.77 trillion yen worth of assets, of which 91.61% were JGB.

Japan Central Bank Likely to Monetize Debt

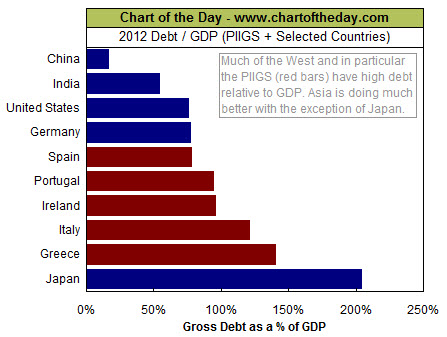

Give that Japan is the most indebted major developed country in the world with more than a 200% debt-to-GDP ratio (bigger than Greece), Japan can simply not allow interest rates to rise as the debt servicing costs would eat up too much of their annual budget.

Source: Capitalogix

The biggest buyer of Japanese debt has been their own citizens and their demographic trends show that more and more citizens will be retiring and selling their assets to support themselves during retirement rather than accumulating assets, which as highlighted above is already beginning to occur as the GPIF has turned into a net seller of JGB. If Japan can’t turn to their own citizenry to be net buyers of JGB’s and their paltry yields are unlikely to interest foreign buyers, who else can support the massive amount of debt that will be maturing every month over the next five years?

The likely buyer will be the BOJ as they monetize the debt to suppress interest rates and keep the debt servicing costs low. The BOJ has already been monetizing JGB’s for some time and I expect they will increase their purchases over the next 2.5 years and reclaim the title as the central bank with the world’s biggest balance sheet relative to their economy.

Source: ft.com

Central Bank Balance Sheets Drive Exchange Rates

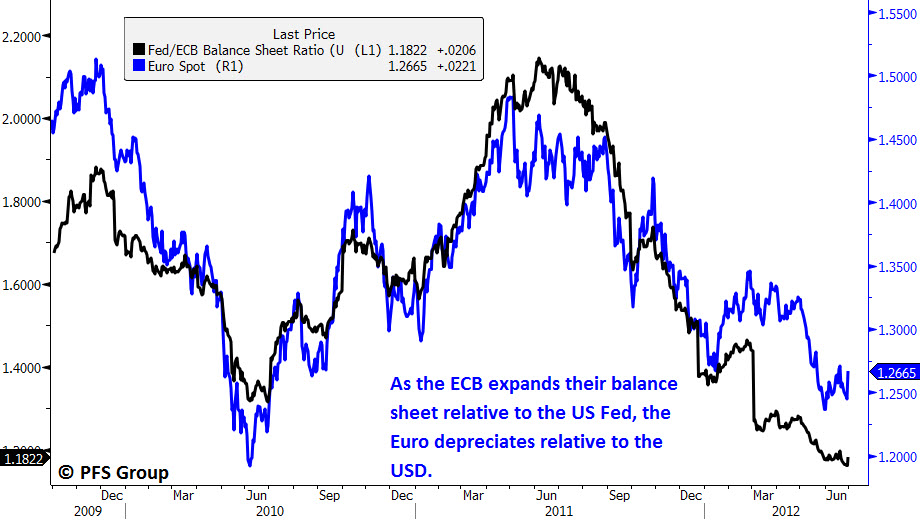

With the unprecedented central bank intervention we have seen since 2008, one coming theme has been a global race to devalue one’s currency to stem exports and the economy and increase economic activity relative to the debt burden. As a result, we have seen a direction correlation between the relative size of central bank balance sheets and foreign exchange rates. A perfect example of this is the relative balance sheets of the Fed versus the ECB and the EUR/USD exchange rate. This is shown below and it is incredibly difficult to determine which is the exchange rate and which is the balance sheet ratio as the two are virtually identical.

Source: Bloomberg

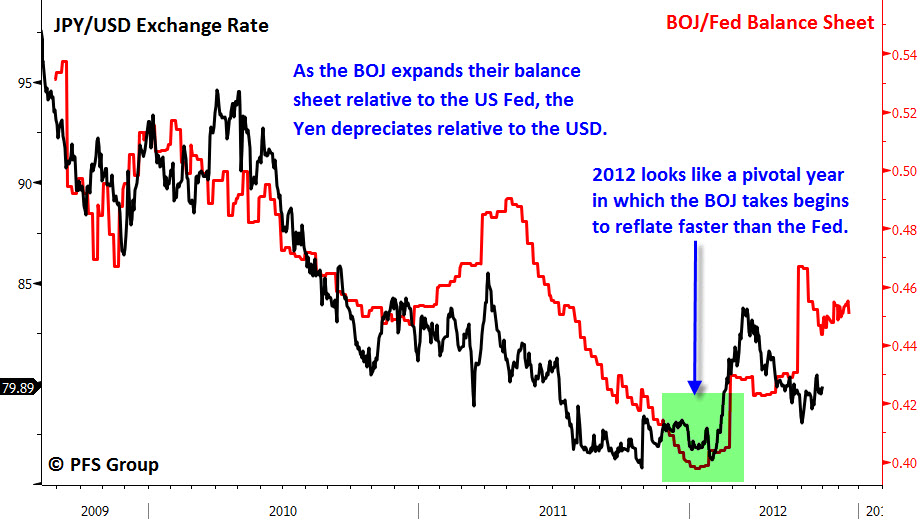

The same is true for the BOJ and the US Fed, though their relative balance sheets tend to lead the currency exchange rate by a few months. This can be seen below when looking at the BOJ/Fed relative balance sheets relative to the Yen/USD exchange rate. As the BOJ intervenes in the currency market by buying JGB’s they weaken the Yen relative to the USD if the Fed keeps its balance sheet constant.

Source: Bloomberg

The Yen Appears to Have Peaked, Currency Markets Sniffing out Debt Monetization to Come

It appears that June has been a pivotal month for the Yen as it is weakening globally as world markets may be starting to discount massive Yen devaluation to come over the next two years.

Source: Bloomberg

In terms of the Yen/USD exchange rate, the Yen has strengthened relative to the USD for five years but we appear to be witnessing a major shift in this trend as the trend line was broken earlier in the year in which the Yen sharply devalued relative to the USD by more than 10% from early February to late March. It appears that the JPY/USD breakout that occurred came back to test the breakout and is heading higher once more.

Source: Bloomberg

One of the primary beneficiaries of a weaker Yen are Japanese exporters who are likely to see greater demand for their goods as they become cheaper to foreigners which will boost corporate sales and thus the Japanese equity market. The Nikkei 225 Index has a strong correlation to the JPY/USD exchange rate and a weaker yen ahead could lead to a major rally in Japanese equities.

Source: Bloomberg

Stepping back a bit and looking at the global situation, we see Europe focusing more and more on growth and less on austerity as their austerity measures of the last few years have simply not worked. What is likely to be associated with a greater growth focus in Europe is more debt monetization by the ECB and combine that with the likelihood that the BOJ begins to monetize JGBs in earnest, we may be in the early stages of a strong global reflationary wave ahead. Given corporations have some ability to pass through inflation into their goods they will likely benefit from global debt monetization, particularly if the monetized debt is used to increase economic activity. The likely plan ahead for indebted domestic economies is to bring down debt-to-GDP ratios by reflating their economies and increase nominal GDP relative to their debt levels.

Circling back to the notion that the BOJ is likely to begin a massive debt monetization ahead, US investors are likely to benefit in two key ways. The first is that the USD will appreciate relative to the Yen making imported goods from Japan like cars, TV’s and other electronic goods cheaper. Additionally, a stronger USD will also bring down commodity prices which are priced in USD’s, leading to overall lower inflation levels. Keeping inflation rates low while maintaining positive (but meager) GDP growth will keep real interest rates low and lead to lower debt-to-GDP levels, what Ray Dalio of Bridgewater Associates calls a “Beautiful Deleveraging.”

I would keep a close eye on the JPY/USD exchange rate as an indication of how active the BOJ is likely to be in monetizing Japan’s massive debt burden. Given a large portion of Japan’s mountain of debt is maturing over the next two years we will not have long to wait. If the BOJ begins a massive debt monetization program and Europe begins to focus on growth and not austerity, equity bears and bond bulls beware!