At any given point in time there are several variables that affect the price of gold. There are times when gold’s price is driven by its perceived association with inflation and other times it’s seen as a “safety asset” or even a global currency. One variable in particular that was a constant driver of gold’s bull market in the 1970s was the presence of negative real interest rates—where inflation rates are higher than nominal interest rates—which means savers who park their cash at the bank are seeing their purchasing power eroded. The power of negative real interest rates as a major catalyst for gold has also been dominant in gold’s secular bull market this time around and currently argues for new highs. However, the USD’s strength at present has been keeping gold in check. That may soon change if the Euro begins to stabilize and money flows back out of the USD.

Gold Variables

As mentioned above, one of the strongest correlations to the price of gold is not the USD but actually real interest rates. This can been seen below in which the top panel shows the open interest for gold futures contracts, the middle panel shows gold along with real interest rates (inverted in red), and the bottom panel shows the USD Index along with gold (USD Index shown inverted for directional similarity). Real interest rates in the middle panel have had the most consistent relationship with gold over the years but that changed in the middle of 2011 when the USD Index began to rise (fall in bottom panel below), despite real interest rates falling to new lows which suggested gold should be hitting new highs.

Source: Bloomberg

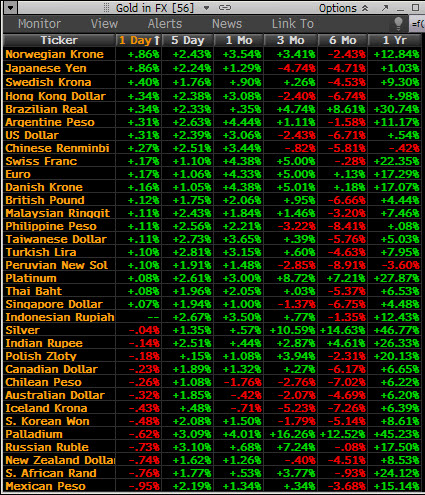

I believe that once we see the USD peak and the EUR stabilize we will see money flow out of the USD and into other currencies which will lead to weakness in the USD and strength in gold. I think a turning point is at hand as gold is already beginning to rally relative to global currencies as seen in the table below. Gold over the last month (middle column below) is up against virtually every world currency save but 3, indicating its recent strength is a global development.

Source: Bloomberg

We are also entering the seasonal strong period for gold in which it typically bottoms in the middle of August and then rallies into the end of the year due to seasonal gold buying by India for the upcoming wedding season.

Source: Bloomberg

Last year the demand from India was particularly weak and part of the reason for this was gold’s more than 37% move between early July and September when priced in Indian Rupee. Basically India went on a buyer’s strike due to the shock in prices. However, gold priced in Rupee has essentially gone nowhere and Indians have had time to adjust to higher prices just as the US has adjusted to higher gasoline prices, and so it is not likely that the current level of gold will be as major of a depressant on Indian buying this season as it was last year. Morever, the Chinese who have been major buyers of gold have seen it decline roughly 20% from last year to this year’s low and are likely buyers at these levels.

Source: Bloomberg

Technical Backdrop for Precious Metals is Very Attractive

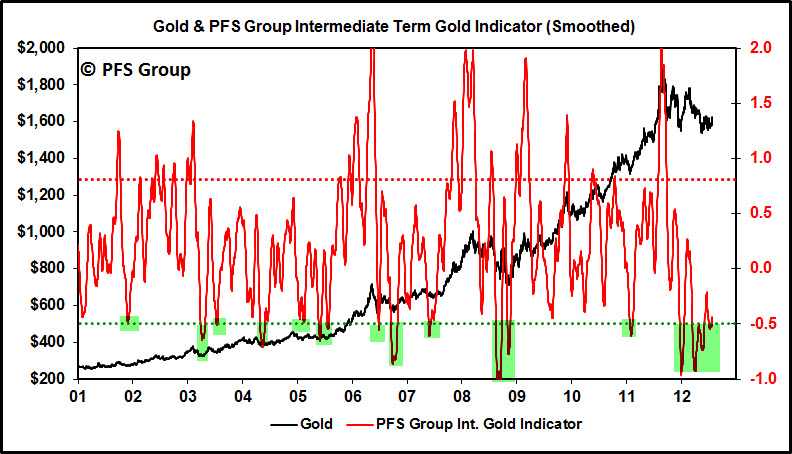

We are entering the normal seasonal strong period for gold at a time when gold and silver bullion and precious metal producers are near the most oversold conditions they’ve seen in the past decade, indicating this year might be a great buying opportunity. For example, our technical risk indicator for gold is at levels that have marked major lows for gold since the bull market began in 2001.

Source: Bloomberg

The same can be said for silver which remains very depressed and at levels last seen at the major 2004 and 2008 lows.

Source: Bloomberg

Precious metal producers as seen by the NYSE Arca Gold BUGS Index (HUI) are the most oversold they’ve been in years where one has to go back to the 2004 or 2008 lows to find gold stocks this oversold.

Source: Bloomberg

Given the collapse in the producers relative to the price of gold, the price-to-sales ratio for the HUI is roughly where it was back in 2008 as gold stocks remain incredibly cheap at current levels.

Source: Bloomberg

All Hangs on the Euro

Given the major factor holding gold back over the past nine months has been the USD, it is imperative that the Euro hold support and the USD weaken. We are presented with a very bullish setup for the Euro given it is testing the 2010 lows and holding at the same time the weekly MACD is on the verge of a buy signal and showing positive divergence with price (middle panel) and the 14-week RSI (bottom panel) is at levels associated with significant bottoms. If the Euro can stabilize here and hold and the USD weaken at the same time we head into the seasonal strong period for precious metals, we may have a decent move in metals heading into the fall. Given their very oversold condition and cheap valuations, metals appear to be presenting investors with an attractive buying opportunity. With all the rhetoric coming from ECB head Mario Draghi and the upcoming ECB meeting on August 2nd, we may be treated to some fireworks in the not too distant future that may shed light on whether or not the Euro holds. If the Euro breaks and the ECB underwhelms market expectations next week I would expect another round of selling in the gold sector, but if the ECB does begin to flood the system we may see a dramatic move in metals.

Source: Bloomberg