As everyone is well aware, Europe is an absolute mess and while the U.S. stock market has been remarkably resilient, it has finally succumbed to news across the Atlantic and is now the final region to experience a decline. The U.S. economy has been fairly strong this year with a continued improvement in the labor market at the same time inflation has been kept at bay. While Fed Chairman Bernanke would like to launch another round of quantitative easing (QE3), he has not had the latitude to do so as weakness in Europe and a declining stock market have not provided the Fed with enough of cover to hit the print button.

However, things are changing in Bernanke’s favor as odds for QE3 to be announced at the June FOMC meeting are rising. As every investor across the globe should realize by now, if central banks step up to the plate we are likely to see the market’s “switch” tuned back from risk off to risk on. While it is anyone’s guess at which point central banks will intervene and where stock prices will be when they do act, we can expect a capital flight out of bonds and into stocks when it occurs as stocks’ investment appeal over the U.S. Treasury market is back to levels not seen since March 2009. Given that investor sentiment is also back to the depths of despair seen at the March 2009 lows, the stage has been set for central bankers to spring the market higher at a point of near maximum pessimism.

Europe Unraveling

The market’s selloff accelerated this week partly on news that Greeks have pulled about $898 million in deposits from Greek banks since the May 6th elections (see article) and market participants feared a bank run on Spanish and Italian banks would be next. Their fears soon materialized as Spain’s Bankia shares plummeted as much as 29% yesterday on concerns about a deposit drain (see article). Spanish banks have been absolutely decimated and have taken out their March 2009 lows as the following equally-weighted Spanish Bank Composite shows.

Source: Bloomberg

While not shown, European bonds have been selling off strongly and pouring into German Bunds which have soared as European investors seek safety. Momentum is building to the point that central banks will be forced to act or watch things unravel before their eyes.

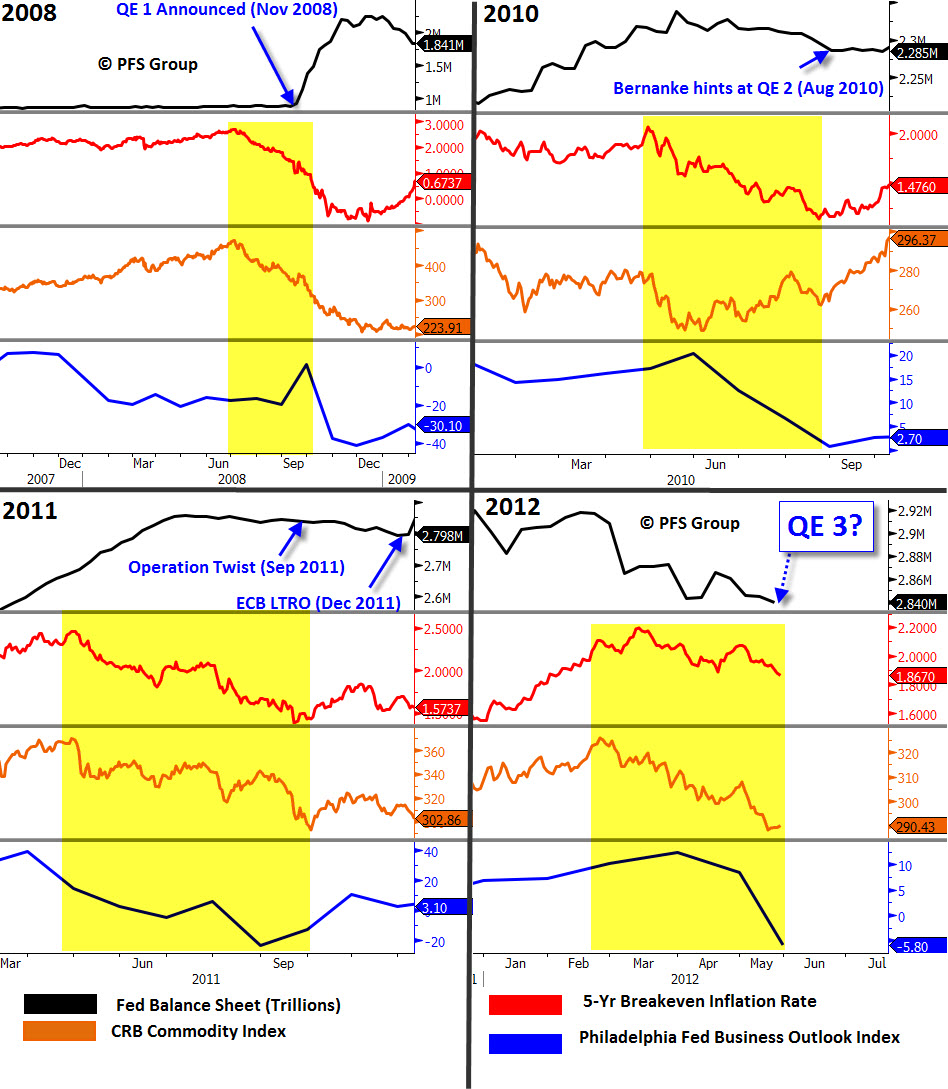

Bernanke Has His Trifecta!

For Bernanke to have cover to launch yet another round of quantitative easing (QE) he generally needs conditions just right for justification. That is, falling commodity prices, falling inflation expectations, and a weakening economy. When all three of these conditions are in place we often see “Helicopter Ben” fire up the Fed’s printing press. Commodity prices have been tanking since March as have inflation expectations (as measured by breakeven inflation rates), but the economy so far has remained resilient—resilient that is until now.

The Philadelphia Fed’s Business Outlook Index for May came out this week and it was a HUGE negative surprise, coming in at -5.8 versus its prior reading of +8.5 and consensus expectations for +10.0. Negative readings relate to a contracting economy while a positive reading indicates expansion. On the positive side of things, the Empire Manufacturing Survey came in at 17.09 and above consensus but when you average the two together to estimate with the national ISM Manufacturing PMI will be you get a sub 50 reading of 47.7, indicating contraction.

Source: Not Jim Cramer Blog

Bernanke has stated that the Fed remains ready to act if the economy weakens and now, with a sub-50 ISM reading not seen since 2008-2009, he has all the room he needs to launch QE3. As highlighted below, prior to previous periods in which the Fed has acted we saw falling commodities, falling inflation expectations, and a weakening economy, or what I call the “Bernanke Trifecta.” These trifecta periods for previous Fed action and the current situation are shown below and highlighted in yellow.

(See color legend at bottom)

Source: Bloomberg

Stocks Should Rally Strongly on Central Bank Action, Incredibly Attractive Relative to Bonds

As we have seen now for four straight years, when central banks spring into action we see a powerful move in stocks as the following graphs illustrate:

Source: https://fingfx.thomsonreuters.com/2012/04/11/0744388e09.htm

While it is hard to know when exactly the Fed and other central banks will act, or where stock prices will be at the time they do, currently we are being given a very attractive buying opportunity in stocks relative to bonds. Also, once central banks do act we are likely to see a strong move from bonds to stocks. For example, with the 10-Yr UST yield currently resting at a mere 1.72%, the S&P 500’s dividend yield of 2.19% has reached the same spread as it did at the 2011 lows and is closing in on where it was at the March 2009 lows (see lower panel below).

Source: Bloomberg

With the current decline in the stock market and rally in the bond market, coupled with a trend in companies increasing dividends, the abundance of stocks with dividend yields greater than the 10-year Treasury is also matching levels seen at the March 2009 lows.

Source: Wolfe Trahan & Co. (Portfolio Strategy Update, 05/15/2012)

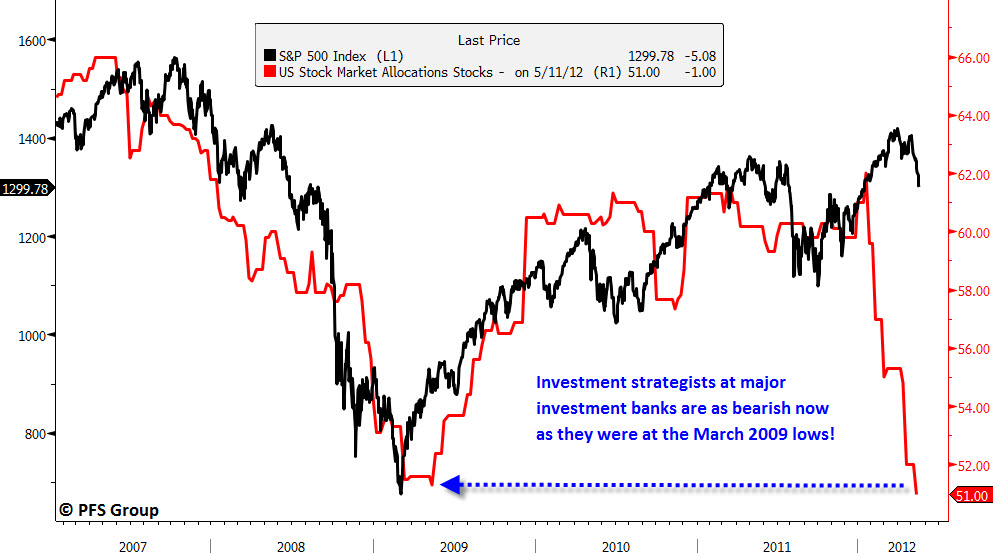

Rampant Pessimism May be Springboard for Equity Rally

We are closing in on correction status (10%+ decline) with the S&P 500’s 9.17% decline from the April 2nd top to today’s lows, and what is astonishing is how quickly bulls have capitulated. The decline in bullish optimism towards stocks is usually associated with more severe declines than what we typically see and is likely a result of the chronic market volatility. For example, Bloomberg surveys the top strategists from various investment banks as to their asset class recommendations and the strategists recommended allocation to stocks has, once again, collapsed to the previous 2009 lows. By the time strategists were this bearish towards equities (and indirectly bullish on bonds/cash) in March 2009, the S&P 500 had declined by 57.7%. This is amazing in that it merely took a 9.17% decline to match the same pessimism strategists had at the actual market bottom in 2009.

Source: Bloomberg

Even the American Association of Individual Investors (AAII) percent bulls survey shows readings associated with market bottoms.

Source: Bloomberg

Market Ripe for a Bottom

There are five indicators I use to help spot intermediate bottoms in the stock market and all five have reached levels associated with prior intermediate lows. As seen in the image below, the five technical indicators in the panels below the S&P 500 have reached at least two standard deviations below their average and we should see some relief in equities ahead as selling begins to abate and shorts cover and lock in their profits.

Source: Bloomberg

While we have reached extremely oversold conditions, being oversold is not a catalyst for a market rally, but simply a measure of how coiled the rally spring is. We need to have some type of news event to lift markets, whether that is some favorable economic report or central banks playing lip service to the market. While I believe a relief rally is imminent, I do not know how far equities will rally without central bank intervention given that problems in Europe remain unsolved. If Europe blinks and prints more Euros then the can will be kicked down the road a bit further and allow the markets some breathing room. Additionally, while the Fed does not meet again until June, that didn’t stop Bernanke in 2010 by leaking his intentions to print money at the August 2010 Jackson Hole Symposium. Bernanke can easily telegraph his intentions of QE3 in a speech sometime before the Fed’s June meeting to help arrest the decline in the markets.

Summary

At the present time selling pressure continues to pick up momentum and the fact that equities can’t stage a rally in the final hours of trading suggests that lower prices are in store in the days ahead. We have yet to see capitulation in the market with a strong decline followed by a sharp intraday rally on high volume. Until we see such an event or hear of central bank intervention, investors should remain defensive with cash on the sidelines. However, when we do get central bank intervention investors have been given a very attractive opportunity to reallocate to stocks and away from bonds as the S&P 500’s dividend yield relative to the 10-Yr UST is back to where it was at the March 2009 lows. Bonds at current rates are simply not an attractive option particularly with yields below the rate of inflation, and with pessimism as rampant currently as it was at the March 2009 lows the Fed has a strongly coiled spring with which to push the stock market higher.