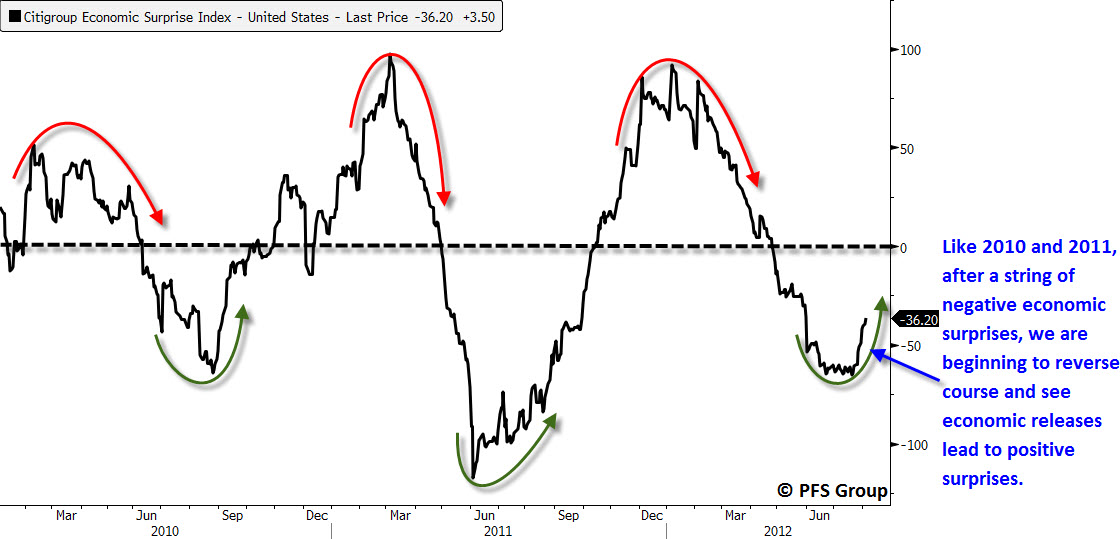

It’s beginning to look a lot like the 2010/2011 economic and market cycle is being repeated again. Here's how the pattern goes: A strong first third of the year followed by a weak middle in which markets sell off and recession fears rise only to see a turnaround in the last third of the year as economies and markets recover. Associated with the economic and stock market rollercoaster we’ve been on now since 2010 are swings in economic surprises. Economists have a tendency to take recent past history and extrapolate the data into the future and so they are consistently missing the mark in this rollercoaster environment. Investors can use this to their advantage as watching for turns in economic surprises can help identify economic and market turning points. We are currently witnessing more and more economic releases surprise to the upside which indicates we have seen an economic inflection point and the economy is likely on the mend.

Source: Bloomberg

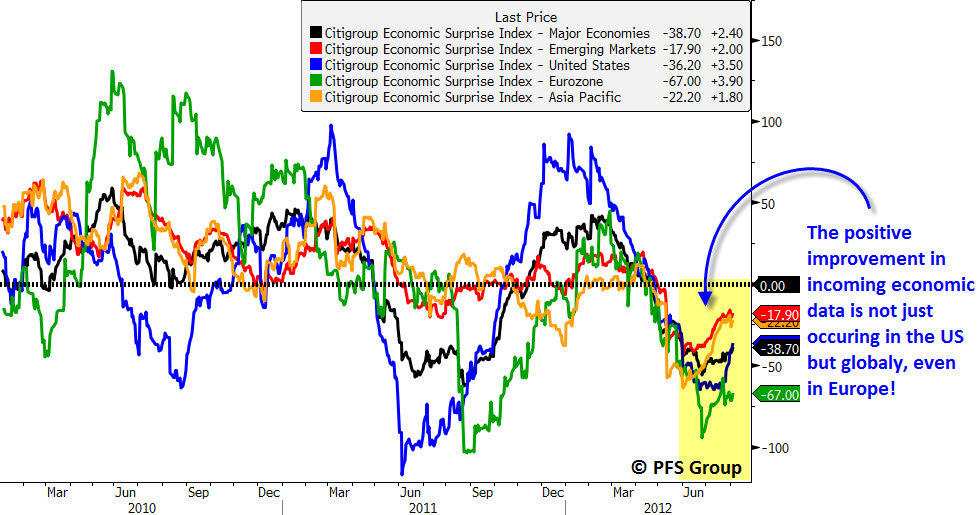

The string of positive economic surprises is not just a US development but global. With the improvement in economic momentum recent recession calls should begin to fade and ECRI’s head Lakshman Achuthan’s recession call may prove to be inaccurate.

From Negative to Positive Surprises

As mentioned above, we are finally witnessing a larger number of economic releases in the US and globally coming in better than consensus forecasts, just as occurred in the middle of 2010 and 2011 which signaled that economies were on the mend. We are seeing this again as major economies, emerging markets, and even the Eurozone are seeing economic releases with positive surprises and it looks like the worst may be behind us for now as the surprise index for major economies is expected to continue to improve into November.

Source: Bloomberg

Francois Trahan, voted top Wall Street Institutional Investment Analyst in four of the last six years, has noted that with zero-bound interest rates, inflation has become the new Fed Funds rate.

Recommended listening: Francois Trahan, Co-author of “The Era of Uncertainty: Global Investment Strategies for Inflation, Deflation, and the Middle Ground”

Francoi’s thesis is that changes in short-term interest rates influenced by the Fed do not change trend very much. Once central bankers begin an interest-rate raising cycle they tend to last for a prolonged period followed by a pause and then perhaps an eventual interest-rate cutting cycle with the entire cycle playing out over a period of years. Historically, it has been the interest-rate cycle that has been the biggest factor in determining business cycle durations. However, in a zero-bound interest rate environment, short-term interest rates obviously can’t be used to explain the record volatility we are seeing.

For that Francois maintains that swings in inflation act as economic depressants and stimulants and take the role that interest rates once played. One of the biggest swing factors for inflation are commodities and just as interest rate movements are a leading economic indicator, it then follows that commodity prices have become leading economic indicators.

To see what I mean, take a look at the figure below which shows the price of oil advanced and inverted along with the Citigroup Economic Surprise Index for major economies. The relationship illustrated is that rising oil prices lead to future negative economic surprises while falling oil prices lead to future positive economic surprises. Given the decline in oil prices from more than 0 a barrel in West Texas Intermediate Crude oil to a low around a barrel, we are likely to see more economic positive surprises heading into the end of October followed by a return to neutral heading into December.

Source: Bloomberg

No Evidence of an Immanent Recession

One example of an economic release coming in better than expected was today’s release of the nonfarm payrolls for July. The average economist estimate based on 89 different forecasts was for a gain of 101K while the actual was 163K. Of those 89 economic forecasts, only one economist estimated a higher number (165K) than the actual result.

Source: Bloomberg

With payroll gains remaining in positive territory it is highly unlikely that we are currently in recession as Economic Cycle Research Institute’s (ECRI) head, Lakshman Acuthan, maintains.

Recession Here (07/10/2012)

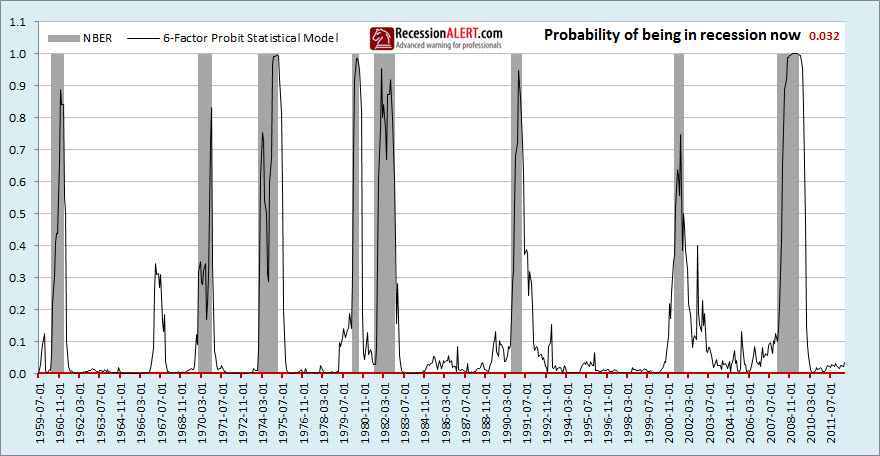

The official arbiters of recession dating is the National Bureau for Economic Research (NBER) and they use four different coincident indicators from which they determine recession start and end dates. Lakshman cites the coincident data to make the claim that we are currently in recession now. However, Dwaine Van Vuuren from RecessionAlert.com argues against this. Using data from the four coincident factors that NBER uses to date recession he calculates only a 3.2% probability that the US is currently in recession.

The NBER co-incident Recession Model – “confirmation of last resort”

Source: RecessionAlert.com

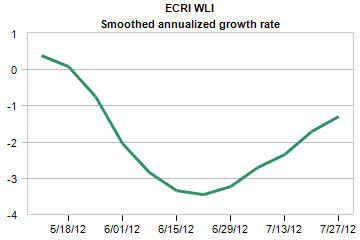

Other anecodotal evidence also suggests the likelihood that the US is currently in recession is quite low. Even using the 6-month percent change for the ECRI’s own Coincident Index shows the probabilities of recesion remain low. For that to occur we would need to see the rate of change of the coincident index fall into negative territory and given that the ECRI’s own leading economic indicator (WLI, second figure below) has bottomed we are likely to see coincident data turn up as well.

Source: Bloomberg

Source: DismalScientist

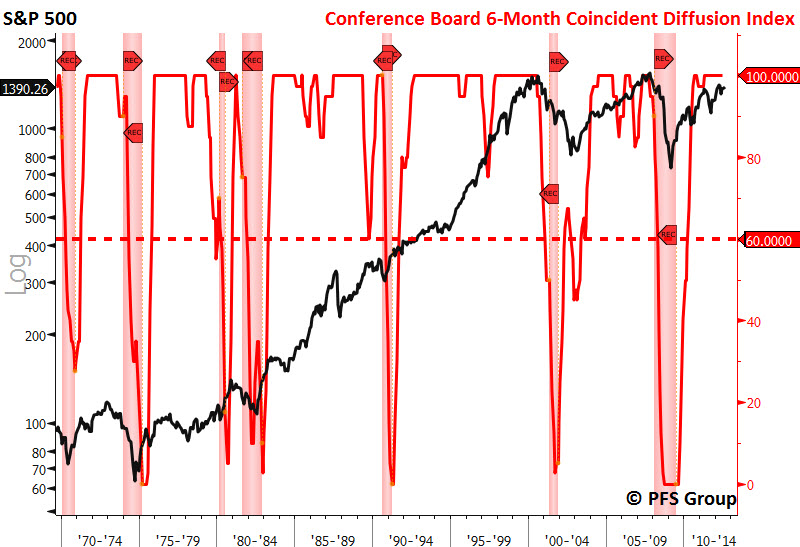

Other sources of coincident data also suggest the likelihood of the US currently in recession remains low. For example, the Conference Board’s 6-month Coincident Diffusion Index currently rests at a perfectly bullish reading of 100%, while readings south of 60% are often typically needed before recessionary alarm bells are raised.

Source: Bloomberg

Even the Philadelphia Fed’s Coincident Index suggests that we are still far away from the recessionary threshold which is seen when the month-over-month change falls into negative territory.

Source: Bloomberg

Given that economic releases are likely to surprise to the upside based on the leading tendencies of oil (as seen above) and that employment gains are likely to continue through the rest of the year based on leading employment indicators (see below), it is highly unlikely that the US is currently in recession nor will be in recession in the near future.

Source: Bloomberg

Conclusion

In a zero-interest rate environment the big swing factor for economies and thus financial markets is no longer short-term interest rates but rather swings in inflation primarily caused by swings in commodity prices. We have recently seen a string of positive economic surprises both here in the US and global and one of the primary factors of this was a decline in oil prices and other commodities which tend to lead economic data by several months. The decline in oil prices that occurred from February to June should lead to a positive global economic stimulus heading into November. This in turn means that we are likely to see a pickup in coincident economic activity based on the leading tendencies of oil which will lead to diminishing risk of recession. As it becomes apparent to market participants that the risk of recession is receding they are likely to reenter the markets and bid prices higher heading into the end of the year. This is exactly what occurred in 2010 and 2011 and looks to be repeating again for the third straight year.