“When the facts change, I change my mind. What do you do, sir?” – John Maynard Keynes

It was back on September 30th last year that the Economic Cycle Research Institute (ECRI) stuck their necks out and made a recession call. The following comments came from a release they posted on their website (emphasis added):

U.S. Economy Tipping into Recession (09/30/2011)

Early last week, ECRI notified clients that the U.S. economy is indeed tipping into a new recession. And there’s nothing that policy makers can do to head it off…

Why should ECRI’s recession call be heeded? Perhaps because, as The Economist has noted, we’ve correctly called three recessions without any false alarms in-between. In contrast, most of those who’ve accurately predicted a recession or two have also been guilty of crying wolf – in 2010, 2005, 2003, 1998, 1995, or 1987.

It has been nearly a year since the ECRI said the U.S. economy was tipping into a recession. In terms of market timing this was a horrible call as the S&P 500 went on to rally 32% in a span of roughly six months. Their press release on September 30th came just two trading days before the market bottomed on October 4th.

Source: Bloomberg

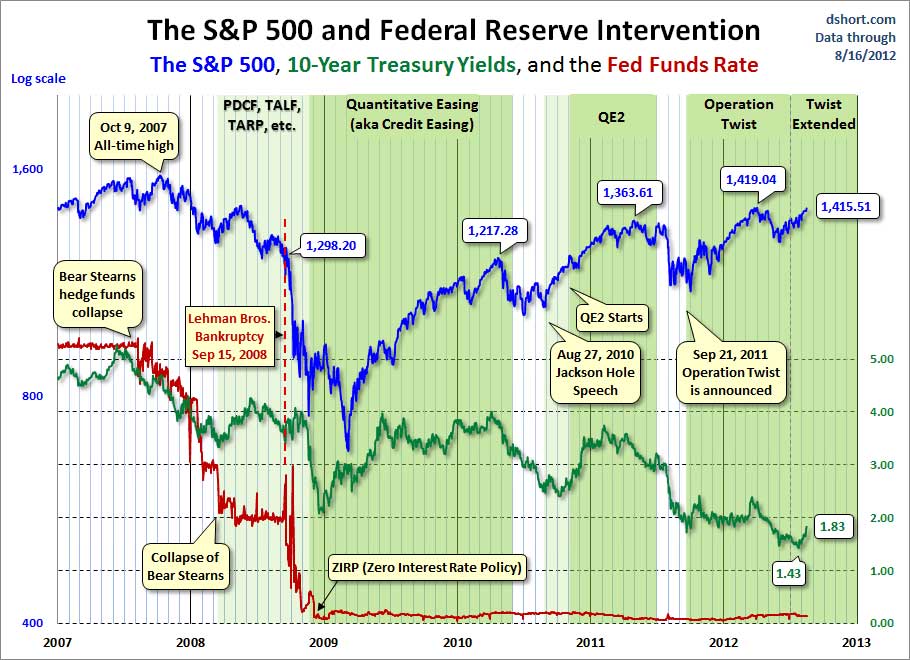

Not only did the ECRI make a recession call but they went as far as to say that a coming recession was set in stone and “there’s nothing policy makers can do to head it off.” To that comment I would like to present the following figure with the caption, “ECRI meet Fed Chairman Bernanke.”

Source: dhsort.com

The periods of central bank intervention are shaded in green and it is more than obvious that the S&P 500 has rallied during periods of monetary intervention and weakened when Fed Chairman Bernanke has taken his foot of the gas pedal. As the above figure highlights, policymakers CAN and HAVE headed off economic weakness by greasing the economic wheels with quantitative easing (QE).

Moving on, the ECRI last month came out in a Bloomberg interview and made the claim that we are currently in a recession but don’t know it yet.

Recession Here (07/10/2012)

Since that time the economy has continued to improve and even the ECRI’s Weekly Leading Index (WLI) has been consistently rising and WLI’s growth rate is on the verge of moving into positive territory.

Source: DismalScientist

The data just isn’t there to support a recession call at this time. One of my favorite indicators is the Chicago Fed National Activity Index (CFNAI), which is a composite of 85 different monthly indicators of national activity based on production and income, employment, consumption and housing, and sales. Readings below -0.70 on the CFNAI have often marked recession beginnings and at a reading of -0.20 for June shows that we are still a good distance away from any recessionary alarm bells ringing.

Source: Bloomberg

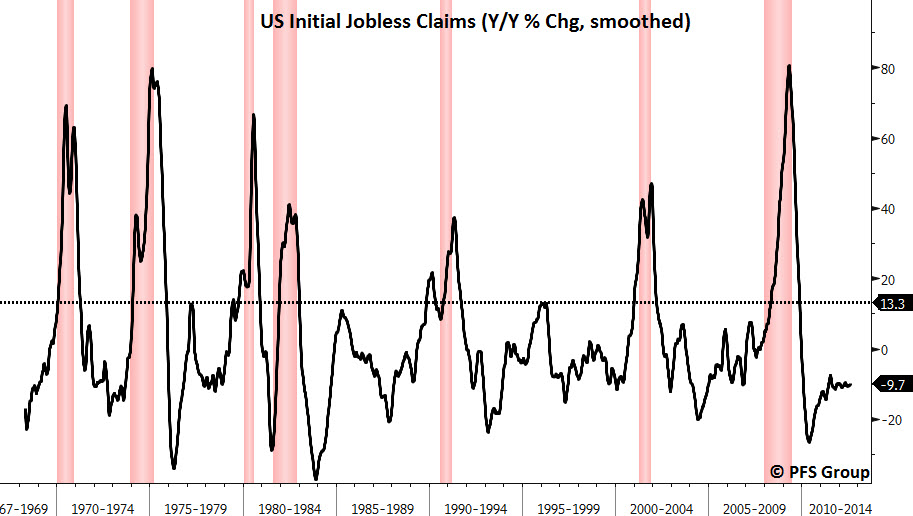

Another great indicator to use to track recessionary risks is the year-over-year (YOY) rate of change in weekly jobless claims. We typically see a 20% YOY jump in jobless claims just as a recession gets underway and we are currently still seeing declines in the YOY rate and well below levels that would indicate a recession may be right around the corner.

Source: Bloomberg

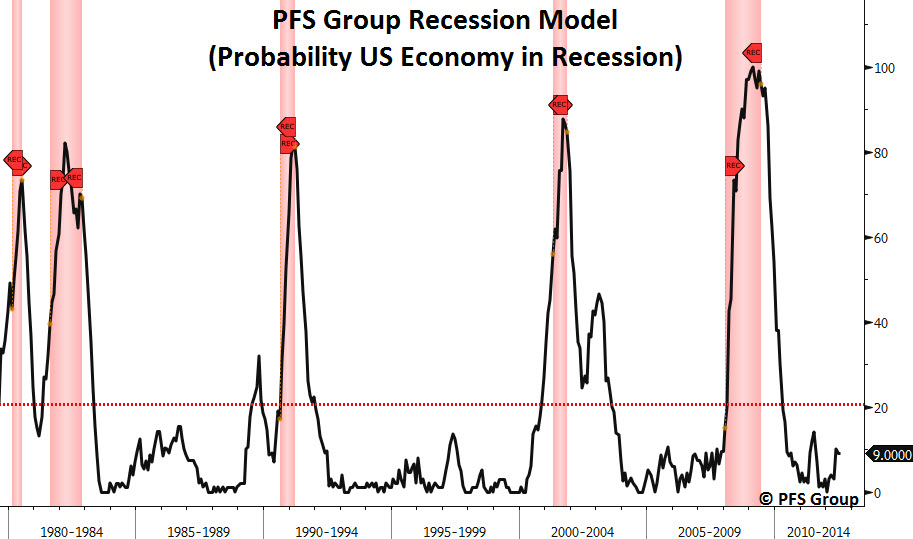

Even our own recession model suggests the risk of a U.S. recession is currently a low probability event.

Source: Bloomberg

Not only are recessionary risks low but they are likely to moderate even further in the months ahead based on past disinflationary stimulus coming from weaker energy prices. There is a strong correlation between oil prices and future economic surprises. The Citigroup Economic Surprise Index (black line below) often traces the inverse path of oil prices (oil prices in red below, inverted) and the decline we witnessed in oil earlier in the year suggests that economic releases should continue to come in better than the consensus for most of the rest of the year. However, the recent gains in oil prices suggests inflationary pressures may hit the economy heading into Q1 2013.

Source: Bloomberg

Being early and being wrong are sometimes one and the same thing. The Economist has stated they made three recession calls without any false alarms, which the ECRI used to highlight the importance of their recession call and distinguish themselves from others who have “been guilty of crying wolf.” However, the ECRI has been flatly wrong on their recession call they made nearly a year ago and the economic landscape dramatically changed after their call and they failed to recognize the change and act accordingly as the facts came in. Since they made their July 2012 call that the U.S. is currently in recession we have seen economic data improve and the market recover.

I was right there with the ECRI calling for a recession last year (September-October Recession Call for U.S. Getting Stronger), but as the data improved I was forced to reevaluate my thesis and became open to the idea of an economic and stock market recovery (A Window of Opportunity). I became even more bullish when I saw the credit markets and equity markets fall back in sync (Finally, equity and Credit Markets in Harmony Again). The important point is to remain flexible and not dogmatic if one is to survive and prosper in the post credit bubble environment with record central bank intervention. One must change as the facts themselves change.

There is nothing wrong with being wrong, everyone is at some time, but a failure to admit when one is wrong is sure to erode credibility. The ECRI would be well to learn from the famous economist John Maynard Keynes who highlighted the importance of intellectual flexibility when he said, “When the facts change, I change my mind. What do you do sir?”