Over this past weekend Russ Koesterich, CFA, who is the iShares Global Chief Investment Strategist, penned an article entitled "The Most Important (And Widely Ignored) Economic Number"wherein he states:

"While economic numbers like GDP or the monthly non-farm payroll report typically garner the headlines, the most useful statistic in my opinion– the Chicago Fed National Activity Index (CFNAI) – often goes ignored by investors and the press."

Russ is correct. The Chicago Fed National Activity Index is a composite index made up of 85 subcomponents which gives a broad overview of overall economic activity in the U.S. As Russ states ignoring the CFNAI could be a mistake:

Markets have run up sharply in recent months partly on the assumption that US economic growth is going to accelerate later this year and translate into faster earnings. But if recent CFNAI readings are any indication, investors may want to alter their growth assumptions for the third and fourth quarters.

Unlike backward-looking statistics like GDP, the CFNAI is a forward looking metric that gives some indication of how the economy is likely to look in the coming months.

The overall index is broken down into four major sub-categories which cover:

- Production & Income

- Employment, Unemployment & Hours

- Personal Consumption & Housing

- Sales, Orders & Inventories

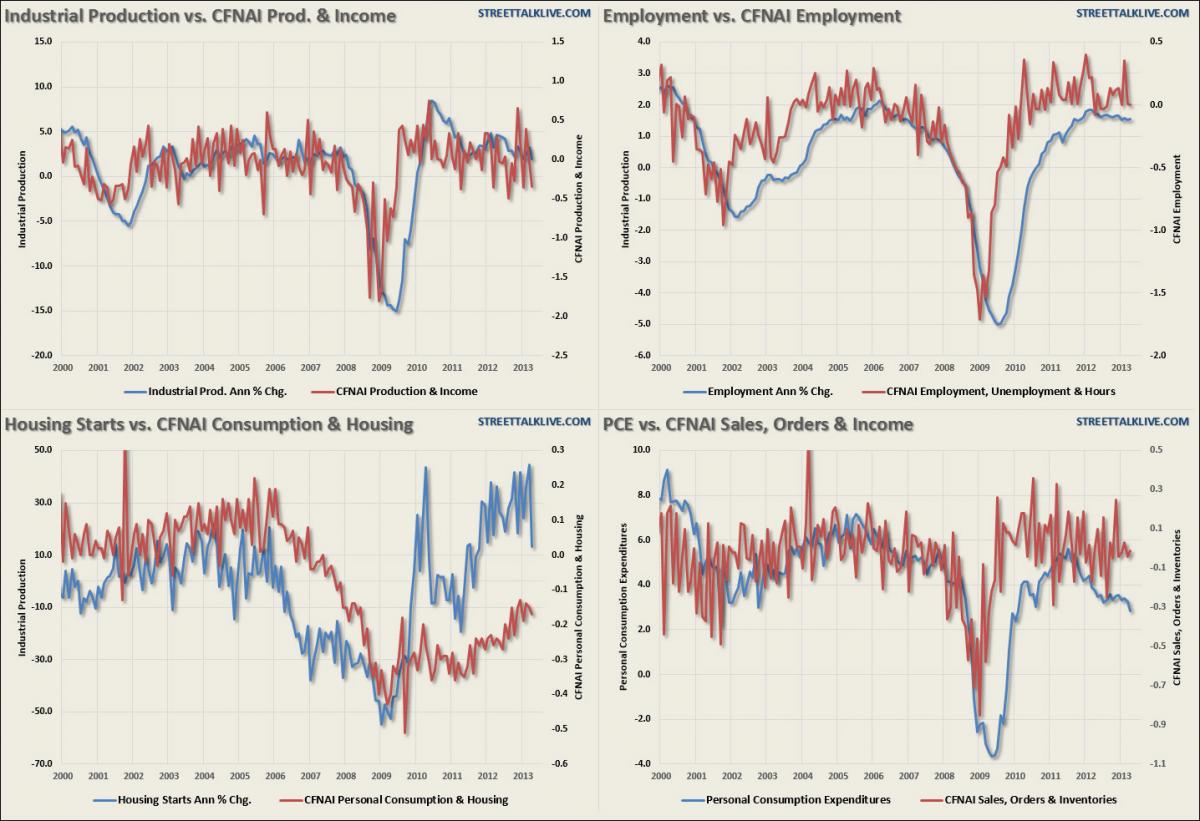

To get a better grasp of these four major sub-components I have constructed a 4-panel chart showing each.

There are a couple of important points to be made in reference to the chart above.

- The production, employment and sales components all appear to have peaked for the current economic cycle despite ongoing estimations of stronger economic growth in the last half of 2013.

- The consumption and housing component, while it has gotten stronger, remains well below its 2000 levels.

Russ stated that:

"And of all the indicators I've tested, the CFNAI has the best track record of forecasting future GDP. Since 1980 the CFNAI has explained roughly 40% of the variation in the following quarter's GDP, an extremely high proportion for a single indicator."

In order to assess that predictive capability I have created a second 4-panel chart with the four CFNAI subcomponents compared to the four most common economic reports of Industrial Production, Employment, Housing Starts and Personal Consumption Expenditures. In order to get a comparative base to the construction of the CFNAI I used an annual percentage change for these four components.

The correlation between the CFNAI subcomponents and the underlying major economic reports do show some very high correlations. This is why, even though this indicator gets very little attention, it is very representative of the broader economy.

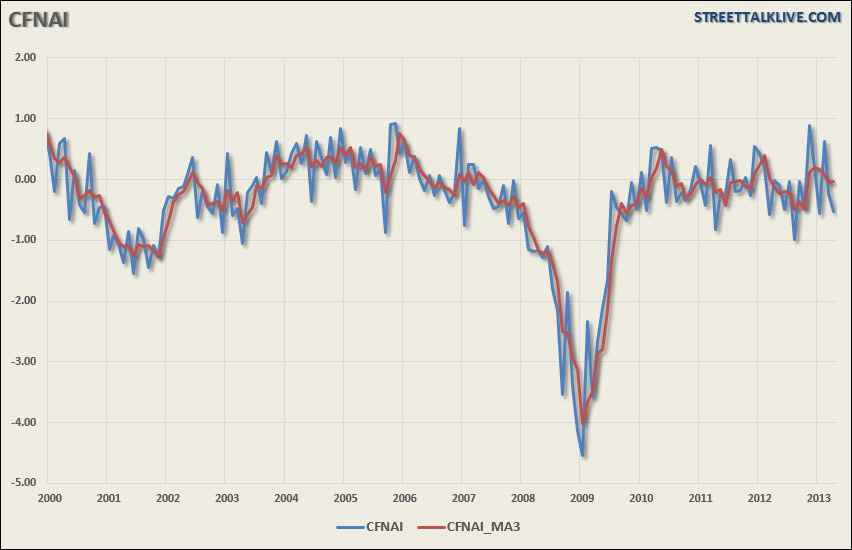

Currently, the CFNAI is not confirming the mainstream view of an "economic softpatch" that will give way to a stronger recovery by year end. The latest CFNAI report plunged to -0.52 for April and the index has been negative for the past few months. This is shown in the chart below which shows the CFNAI index as compared to its 3-month average.

Russ goes on to state that:

"While the CFNAI's current level is still consistent with economic growth, it does suggest that growth will sharply decelerate in the second and third quarters of this year, falling to about 1.8%."

This last statement is key to our ongoing premise of weaker than anticipated economic growth despite the Federal Reserve's ongoing liquidity operations. The current trend of the various economic data points on a broad scale are not showing indications of stronger economic growth but rather a continuation of a sub-par "muddle through" scenario of the last three years.

While this is not the end of the world, economically speaking, such weak levels of economic growth do not support stronger employment, higher wages or justify the markets rapidly rising valuations. The weaker level of economic growth will continue to weigh on corporate earnings which, like the economic data, appear to have reached their peak for this current recovery cycle.

The CFNAI, if it is indeed predicting weaker economic growth over the next couple of quarters, also doesn't support the recent rotation out of defensive positions into cyclical stocks that are more closely tied to the economic cycle. The current rotation is based on the premise that economic recovery is here, however, the data hasn't confirmed it as of yet.

The reality is that either the economic data is about to take a sharp turn for the positive or the market is set up for a rather large disappointment when the expected earnings growth in the coming quarters doesn't appear. From all of the research that I have done as of late, it is the latter that seems the most likely of outcomes as there does not seem to be a driver, currently, for the former. Maybe the real question is why we aren't paying closer attention to what this indicator has to tell us?

Source: Street Talk Live