“In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.” – Rudiger Dornbusch

Ben Bernanke made some surprisingly frank confessions in his House testimony about Fed portfolio risk. When asked what the effects of a mortgage refi program would be on his trillion mortgage portfolio, Ben responded that the Fed would suffer losses. He then said he couldn’t really quantify how much. In another sly legend in his own mind statement Ben warned that if “investors lost confidence” in US fiscal policy (but certainly not his policy), there would be nothing the Fed could do about arresting higher rates. He should have added that marked to market and given the duration of its holdings, that the Fed will lose $2 billion on every basis point increase in rates. That’s $200 billion for a modest one percent uptick in rates.

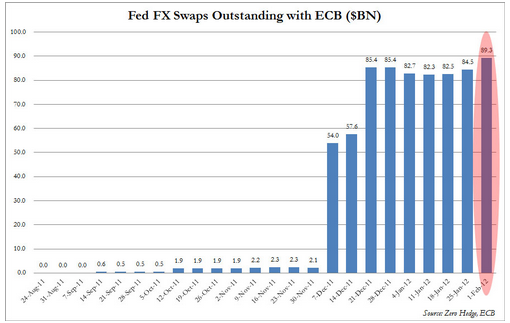

I would add that the minute the Fed slows down on its US Treasury debt buying binge, that rates will rise. He failed to mention that the Fed is the dominant buyer of 58% all Treasury issuance since Twist began, and even higher in long dated paper. He also failed to address if lending money via swaps to the increasingly poorly capitalized ECB constituted portfolio risk (more on ECB Ponzi exposure).

This post is reprinted from Russ's premium service, Russ Winter's Actionable. Click here to subscribe to Russ Winter's Actionable, and get instant access.