The worldwide collapse in commodity prices is now working its way through the financial markets in Canada. Canada is just now experiencing fundamental changes in the financial community, the sector better known as FIRE (Finance, Insurance, and Real Estate). This sector accounts for approximately 20% of national income and employs more than one million workers, providing a broad spectrum of services to all parts of the economy. One subsector, in particular, the investment or securities industry has been hardest hit of late. This blog examines the adjustments in the securities industry; future blogs will look at the banks, life insurance and real estate markets.

To appreciate just how much the FIRE industry has suffered, we turn to the TSX and its major components as listed in Table 1. In the period of 2007 to 2014, the Canadian stock market as a whole fell by 4%. However, the financial sector as a whole performed relatively well increasing by some 21%, largely on the back of the commercial banks, supported by good loan growth and capital market activities. However, within the investment community, independent investment houses have taken quite a beating. The two publicly traded companies, GMP and Canaccord, have seen their corporate value truly decimated (a price drop of 80%). Finally, the lifecos have yet to recover from the 2008 crisis and continue to see their stocks trade well below pre-crisis levels (as much as 60% lower).

These trials and tribulations continued over the past 12 months as all segments of the FIRE industry have seen values drop further. Along with the decline of the TSX60, the finance sector is off a further 19%, partly in concert with the decline in world stock markets, but more reflective in the fall in oil and other commodity prices. Even the much vaulted Canadian banks are feeling the impact of losses in the energy sector. REITs which have been a haven for investors are now in decline (off by 18%). And, of course, the investment dealers continue their slide as they suffer under the weight of several factors unique to the industry. We now turn our attention to those issues.

Investment Industry Under Pressure

The securities industry and, in particular, the independent dealers are crucial to a well-functioning capital market. The big six banks swallowed up major investment dealers in the 1990s; they use these investment firms to continue to fund large publicly traded companies. Independents, on the other hand, supply funds to small and medium sized industries, especially in the resource and tech sectors. Often these companies are deemed too risky to qualify for conventional bank lending. Thus, they have filled an important gap in the capital markets and their current weakened position will have an adverse impact on the effectiveness of the Canada's capital markets to promote economic growth.

These are not happy days for the investment dealers. Revenues are weak, costs are escalating and the nature of their business is undergoing structural changes.

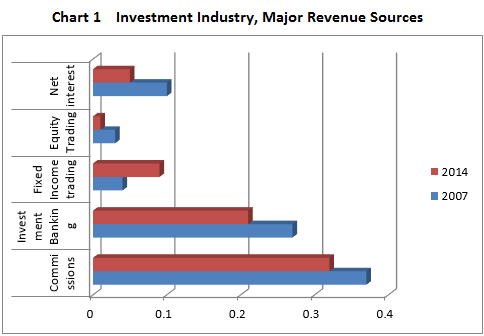

The number of firms have declined as part of a wider consolidation as profitability is squeezed throughout the industry. Chart 1 illustrates the change in revenue sources between 2007 and 2015.

With the exception of fixed income trading, all categories of revenues have declined, especially equity trading commissions and investment banking fees—two stalwarts of the past. Table 2 summarizes the main financial operating results of the past 12 months. The two notable impacts have been the reduction in revenues and the rise in the cost of operations. Overall, profitability is dismal compared to prior years—4.6% rate of return in an industry accustomed to rates of 20% or more. As a result, shareholders' equity has taken a beating, forcing weak companies out of business and others to shore up capital to meet regulatory requirements. What is behind this poor performance?

A series of radical changes has hit the industry simultaneously:

The collapse of the commodity markets. Many of the independent firms specialize in financing medium size resource/extraction enterprises; the collapse resulted in very few investment banking opportunities, shrinking that revenue segment of the industry significantly,

Technological driven price wars. There has been a relentless move towards lower commission prices and electronic trading, contributing to the fall off in revenues.

Compliance and regulatory changes. Ian Russell, the President of the Investment Industry Association of Canada (IIAC), estimates these costs have risen by 7% in 2015, on top of a 6% rise in 2014. He believes " the relentless rise in operating costs will squeeze profitably" in 2016.

The industry features many small independent, boutique-size firms that no longer can compete for capital; the bulk of the firms are capitalized at $10 million or less, precluding them from participating in larger financing deals. Russell expects a further consolidation as firms either merge and/or shut down.

The IIAC recently conducted a survey of its members on the outlook for the industry.

The majority of members remain pessimistic, citing the following:

Rising costs owing to higher compliance and new technology requirements; both add to staff and to total operating costs;

Weak economic conditions as Canada adjusts to the new realty in commodity prices and the slowdown in world trade;

Consolidation and restructuring. Over the past 4 years, 25% of the industry has left the business through mergers and amalgamations, closing operations entirely or transferring business out to competitors.

It is no wonder that the majority of the industry leaders expect further contraction in the coming years as part of a shake out in the industry. It may turn out, in the longer run, that the Canadian capital market will benefit from this re-structuring and may be stronger as a result. However, at present, the principal concern is that this consolidation will negatively affect the viability of the industry to participate in the financing of future economic growth.