You should open a Roth if…

- You’re single and your modified adjusted gross income is less than $122,000.

- You’re married, filing jointly and your modified adjusted income is less than $193,000

- You have a traditional or rollover IRA, open a Roth, start Roth conversions using a “fill the bucket” approach.

- Your work offers a Roth 401(k) option, take advantage of it. There are no income limits for a Roth 401(k).

With the new tax laws in place, there has never been a better time to start preparing for what the future might hold. Where do you think taxes are going? Up or down?

During World War II, we saw federal income tax rates up to 94%. From 1936 to 1981 the top federal income tax rate never went below 70%. If you’re upset about the highest bracket being 37% right now, imagine how you will feel should history repeat itself. Protecting your assets now while taxes are low is the best way to set yourself up for the future. Who doesn’t want tax free income? If I can give you some advice, pay Uncle Sam while taxes are low.

Two Things to Know Before Opening a Roth

- In order to open a Roth IRA, you must have earned income and fall below the income limitations stated above (Unless you’re doing a Roth conversion, then there is no income limitation). The amount you can contribute is 100% of your earned income but maximum for 2019 is $6,000. If you are 50 or older, you can start making “catch up contributions” meaning you can add an additional $1,000 to your contributions each year.

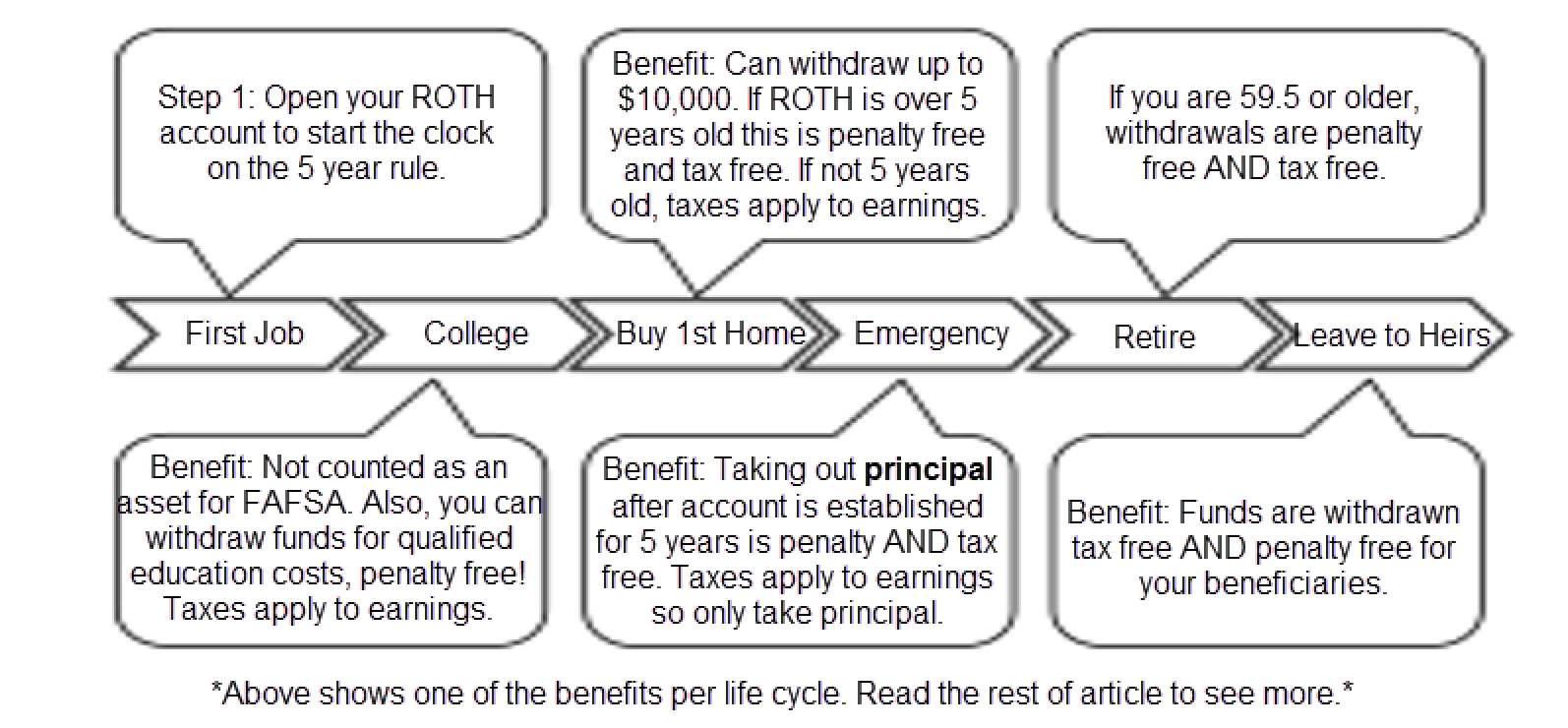

- The “five-year rule” is always going to apply to you unless you are 59 and a half or older. The five-year rule states that when you establish your Roth, or do a Roth conversion, you must wait five years to touch the money in order to make the distribution penalty free.

No matter what stage of your life you’re in, you should have a Roth IRA or something set up in a tax-free account. Whether you’re entering the workforce, or planning to leave money to your heirs (if you choose to do so), you will never regret having a Roth.

Entering the Workforce

If you’re in high school and land your first minimum wage job, or if you just graduated from college and landed your first full time job, open a Roth! Start saving for your retirement and start that five-year clock. It's never too early to start saving for retirement— it will be the biggest expense you will encounter. A friend of mine once told me if you're looking to retire without proper savings, “You can either spend less, work more, or die sooner.” None of those sound appealing, so as you can see the earlier you start, the better!

If your employer offers you a Roth 401(k), do yourself a favor and put your retirement funds there. You’ll have to pay taxes on it before it’s invested, but chances are, you’ll still be in a lower tax bracket. It’s beneficial to pay the taxes now rather than in the future when you start to make more money and will likely be in a higher tax bracket.

Another reason to start filling your retirement bucket early is the effect that compounding has on your savings. If a 20-year-old were to save $379 every month into a Roth, by the time they reach 65 they will retire with over $1 million dollars, tax free! Now, compare that to if a 40-year-old started saving and wanted to retire by age 65, they would have to save $2,102 every month! This assumes a six percent annualized return, compounded annually.

College and FAFSA

College expenses can be a serious burden to students and parents. Having a Roth IRA set up can greatly help for a couple of reasons.

The best benefit of having a Roth IRA, or any retirement account, is that it’s not a countable asset for FAFSA. This means if you’re a student or parent, anything in a retirement account cannot negatively impact what you’ll receive in financial aid.

As stated previously, you can withdraw funds for qualified education costs, (i.e. tuition, fees, books, supplies etc.) penalty free. However, taxes may apply to any earnings so only take principal contributions to avoid paying taxes. The stipulation to keep in mind is if you are eligible for FAFSA, any withdrawals for qualified education costs will count as income and may affect your eligibility for need-based help the next year.

Buying Your First Home

At this stage in your life if you have had your Roth account open for over five years, you can take a qualified distribution of up to $10,000 penalty free and tax free. If you are married and both you and your spouse are first-time homebuyers, each of you can take distributions up to $10,000 without penalties or taxes. This can dramatically help with a down payment for your first home.

Emergency Savings

A Roth should not be your first source of emergency funds but in the event of an emergency, and your Roth has been open for five years, you can withdraw your contributions at any time penalty and tax free! The only portion that is taxed are your earnings, so make sure you are only withdrawing principal.

Roth IRAs are taxed using the FIFO method, meaning first in, first out. When you withdraw from your Roth the contributions come out first, and earnings come out last. Keep track of your contributions in case you ever do run into an emergency and need to withdraw from your Roth.

Home Stretch to Retirement

Once you reach age 50 you can start making “catch up contributions” meaning you can add an additional $1,000 to your contributions each year. So, for 2019, instead of the maximum contribution of $6,000 you can contribute $7,000.

If you have a large traditional IRA or traditional 401(k), you may want to consider starting to do some Roth conversions. The best way to go about this is by implementing the “fill the bucket” approach. Whatever tax bracket you’re in, you’ll take a distribution of the amount that takes your income just below your marginal tax bracket and does not push you into the next higher tax bracket.

Social Security taxation is yet another reason to have your money tied up in a Roth. Roth distributions are not taxable and do not count as income. Social Security is taxed based on your provisional income which includes wages, earnings, interest, required minimum distributions from qualified retirement accounts and other taxable income that is reported on your tax return. Half of your Social Security benefits are added to arrive at your income figure to determine what portion of your benefits are taxable. If your only income is Roth distributions and Social Security, you’re in a really great place.

Leaving a Legacy

Two things are inevitable in life: death and taxes. I’m trying to mitigate the taxes for you, but death is just something I can’t help with. However, I can help by letting you know that when your money is in a Roth your beneficiaries receive those funds tax free! No matter their age or income, that money will remain tax free for them.

Now Open That Roth

Roth IRAs have so many benefits of which most people remain unaware. As you can see at every stage in life there is some type of benefit that Roths provide. The best thing you can do for yourself is to set up your Roth, contribute consistently, don’t touch it and let the compounding do its magic. Should you need to take money from the account to fund education, help pay for your first home, or you encounter an emergency— your Roth is a place you can turn to. Once you hit retirement and can take that money out tax free, you will only be thanking yourself!

If I have not convinced you to open a Roth IRA or contribute to a Roth 401(k) at work, then prepare for taxes to be your best friend because they will always be around! If I have convinced you then contact us at Financial Sense Wealth Management, and we can get you set up.