Markets cheered the notion that the Fed may be close to being done with its rapid pace of tightening on Powell’s comment that the Fed had reached the neutral rate, the interest rate where monetary policy is neither expansionary nor contractionary for economic growth. What is key is that the theory is not centered around stable prices or the Fed’s ideal 2% annual inflation rate, but rather its focus is on economic growth or essentially the economy’s stall speed. There are two points that the market missed that indicate the Fed is not likely to be done as soon as some may think and is why, I believe, last week’s hurrahs will end up as future disappointments.

First off, what was lost by the market is that to bring inflation down you must bring economic demand down and thus weaken the economy even further by hiking rates ABOVE the neutral rate. While everyone is currently fixated on the monetary “neutral rate,” there is another neutral rate that relates to the other side of the Fed’s mandate which is “full employment”. Just as the neutral rate is a theoretical concept that can vary from one institution’s econometric calculation of it from another, the definition of full employment is also a theoretical concept with no definitive answer. Conceptually, full employment is a situation in which there is no cyclical or deficient-demand unemployment. Full employment does not imply the disappearance of all unemployment as there could still be structural unemployment.

Like the concept of the neutral interest rate, full employment is achieved when the unemployment rate falls to the natural rate of unemployment derived by economists. An unemployment rate above the natural rate of unemployment signifies that there is labor slack in the economy and further room for job gains and the labor slack is likely to keep wage inflation in check. Conversely, an unemployment rate below the natural rate of unemployment indicates a tight labor market which is likely to pressure wages higher as workers are in short supply to meet employer demands for labor. The Congressional Budget Office (CBO) puts out a quarterly estimate of their calculation of the natural rate of unemployment, which currently stands at 4.272%. In contrast, our current unemployment rate of 3.6% is well below that indicating that wage inflation pressures will likely continue to be with us for some time, implying that the Fed will likely need to go ABOVE the neutral rate to slow the economy down to reduce the inflation rate.

Secondly, even if the Fed pauses soon, Powell made it clear that the Fed will be ramping up quantitative tightening (QT) by shrinking its balance sheet by double the rate between now and September at $95 billion per month. QT is the Fed’s second mode of tightening and there is no “neutral rate” of QT guiding the Fed. Furthermore, there was no comment from Powell even hinting they may be close to being done shrinking their balance sheet. Hence, a pause in rate hikes is not a true pause but rather a reduction in the pace of overall tightening if the Fed carries on with QT.

Stay ahead of the news! Subscribe to our premium weekday podcast

While economic growth is highly sensitive to the direction and level of interest rates, the stock market’s valuation, such as the P/E ratio, is more sensitive to liquidity—that is, the amount of money being injected into the financial system. An acceleration of liquidity drives price multiples up and a deceleration of liquidity drives them back down. It is no coincidence that the peak in the M2 money supply growth rate occurred at roughly the same time the P/E ratio for the S&P 500 peaked last spring, but, more importantly, is that the M2 growth rate is likely to continue to fall and drive price multiples down if the Fed continues with its expected pace of quantitative tightening.

We should take note that other global central banks are tightening as well, and this phenomenon of decelerating global liquidity will likely impact US market prices as capital is free to flow all around the world:

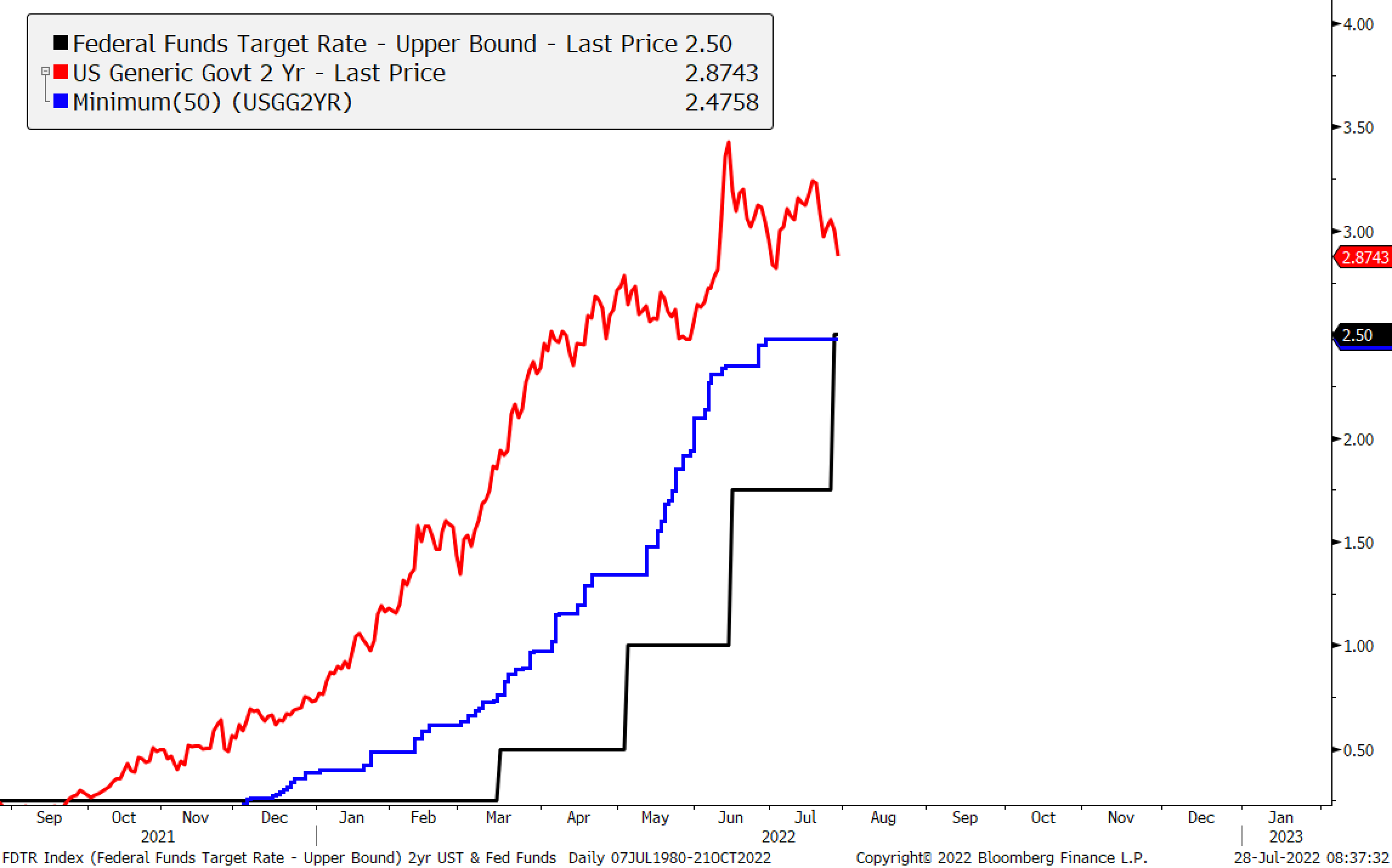

A true pause by the Fed means an end to rate hikes AND an end to shrinking its balance sheet. The market is cheering that we may be getting closer to the former but, I believe, has yet to come to grips with the latter. Given the market is currently fixated on the interest rate pause button, we would like to share an important piece of research we conducted earlier in the year to estimate when the timing of this is likely to occur. Simply put, when the 2-year UST yield hits a 2-month low, on average the Fed makes its last rate hike within two months. Given the recent evolution in rates, according to the historical pattern, we could see the last rate hike as soon as their September meeting.

Now here is where things get interesting. The market is currently pricing in a 100% chance of a 50 basis point (0.5%) hike and a 24% chance the Fed goes 75 basis points (bps) in September. Let’s assume the Fed raises the upper target by 50 bps to 3%. If that occurs, and the 2yr UST yield falls to 2.5% by then or lower, that will mean the 2yr is at least 0.50% lower than the fed funds rate. When that happens, on average, the Fed begins to CUT rates within two months, which would imply rate cuts may be possible as early as the Fed’s very next meeting in November.

For all of this to play out there would have to be a balance between the risks of the Fed’s dual mandate of price stability and full employment by then. As we just learned last week, Q2 GDP came in at -0.90% to mark the second consecutive quarter of negative growth. While the White House has stated that this does not meet the long-held official definition of a recession as defined by the National Bureau of Economic Research (NBER), it is important to understand that we have NEVER had two consecutive quarters of negative real GDP outside of an officially NBER-defined recession in the post-WWII era. I would say that the Fed’s scales of risk that were heavily lopsided towards price stability are becoming more balanced by the day. Should economic data continue to disappoint, then we very well could get a Fed rate pause occurring over the next two meetings. That said, as discussed earlier, there is still the issue of ongoing quantitative tightening, which was what led to a major market disappointment in December of 2018.

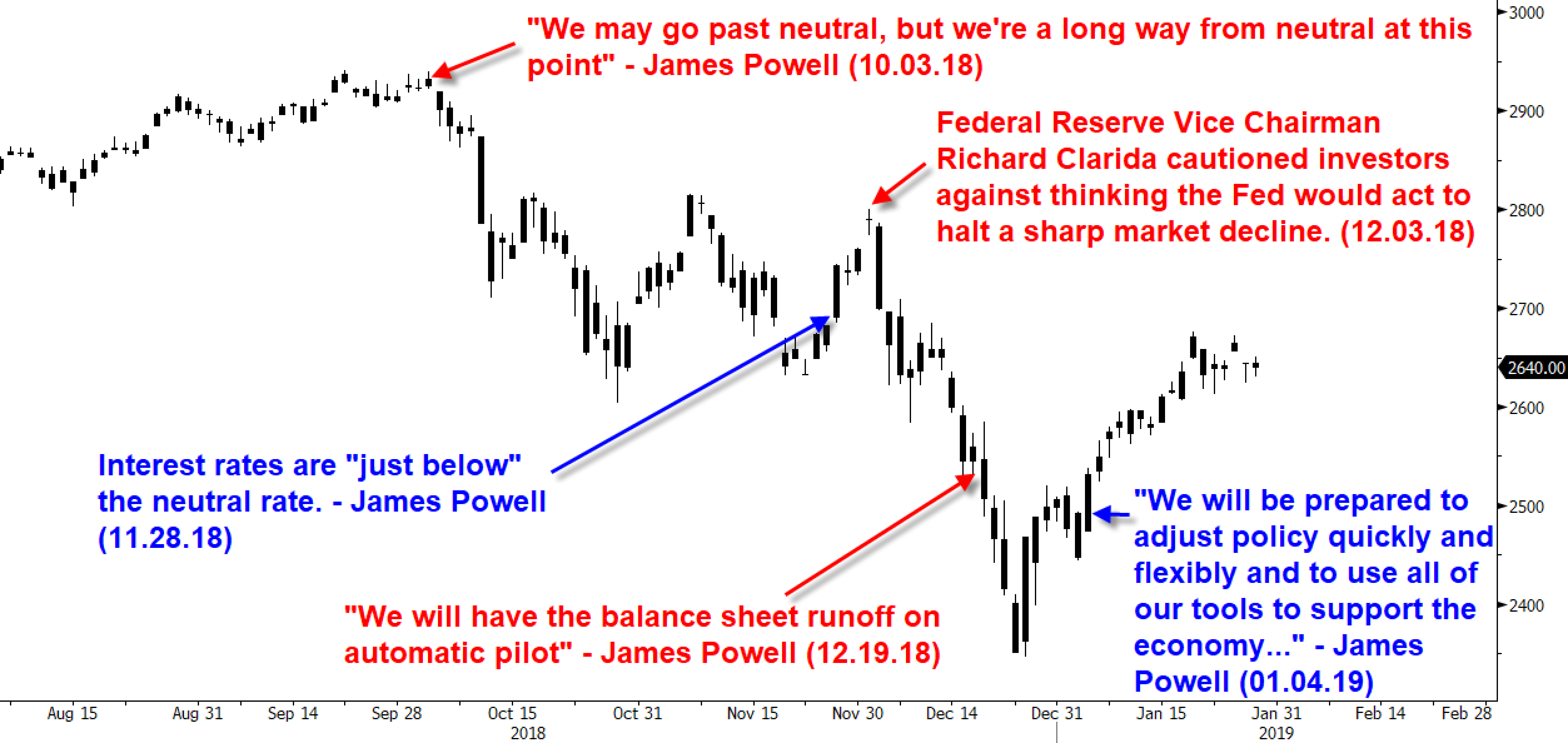

December 2018 Déjà vu?

We could be setting up for a major disappointment by the Fed given it appears to be focusing more on the 40-year highs in inflation and that wage inflation is likely to be sticky. The market, in particular the bond market, is signaling an end to tightening is now in view as it begins to focus more on the economy and the deteriorating growth outlook than inflation. In 2018, the comments by Powell and other Fed officials heightened market volatility by flip flopping their views on the path of Fed policy tightening. Economic growth began to materially disappoint in Q4 2018 and yet the Fed kept raising rates and eventually in December of 2018 the junk bond market seized. During that time, no new issues came to the market so by the Fed’s last 2018 meeting on December 19th, the market was looking for Powell to throw the market a bone that it would stop putting fuel to the credit market fire. Instead, the Fed Dot Plot that month showed the Fed was looking for 3-4 rate hikes in 2019 along with continued shrinking of its balance sheet. The comment during the press conference that the market was particularly troubled by was Powell saying that the Fed’s balance sheet reduction would happen in the background on automatic pilot and that it was essentially a non-event. The market thought otherwise and fell 8% from the prior day to the low on December 24th.

Applying this to today, the Fed said it wants to see several months of consecutive declines in the inflation rate before adjusting course. With two more inflation readings by the September meeting, a drop in CPI inflation is unlikely to meet the Fed’s observations and could set the market for an unpleasant September surprise just like the December 2018 Fed surprise.

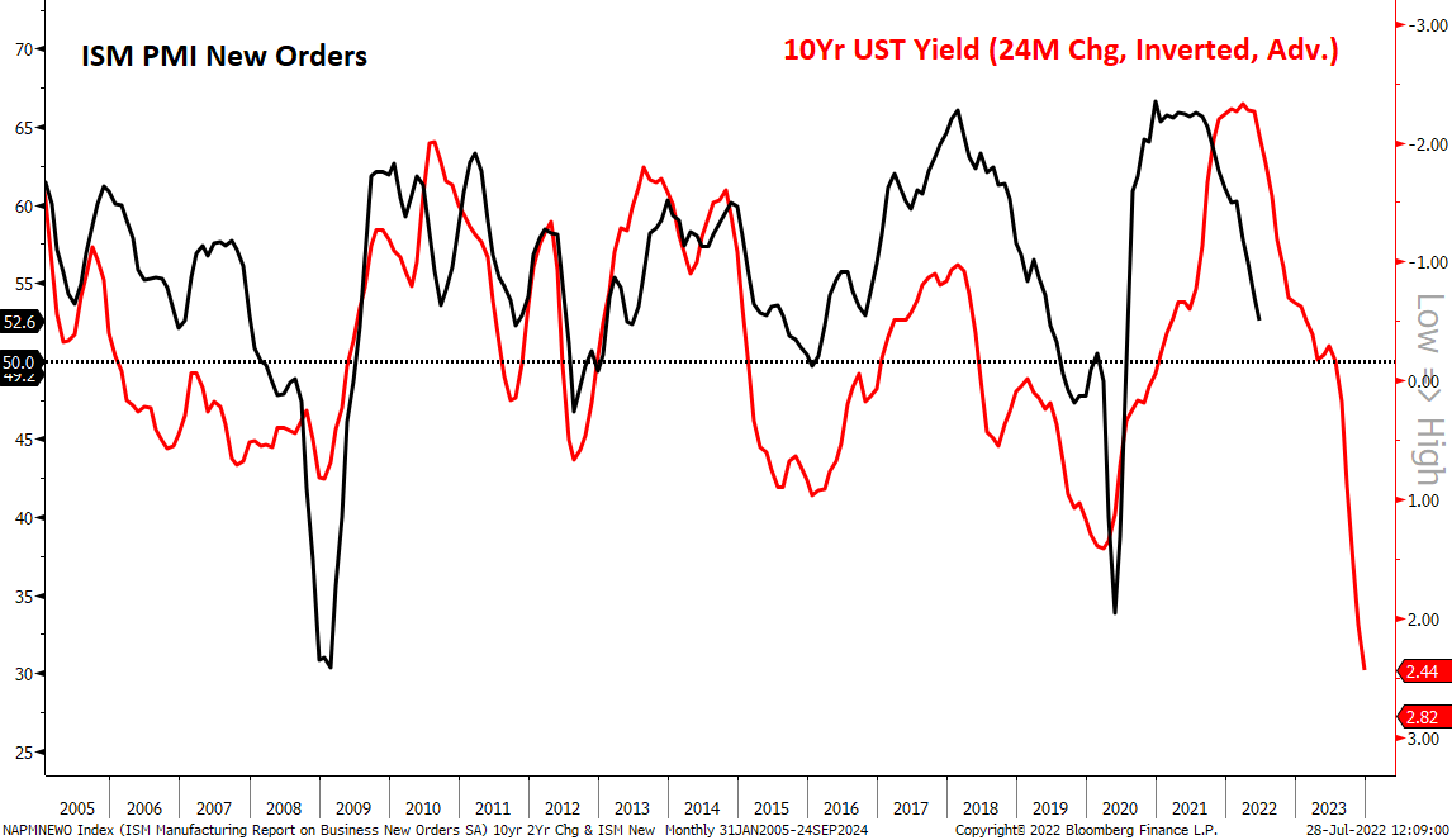

Ultimately, things boil down to whether the US economy will skirt an official recession and have that goldilocks soft landing or fall into an official recession. Since 2004, economic downturns where the PMI falls to a stall-speed reading of 50 and the economy does not slip into a recession, sees the S&P 500 fall between 20-25% below its bottoms-up price target. During recessions, it falls roughly 35% below its bottoms-up analyst target. At its worst, the S&P 500 fell 26% below the analyst target in June and would mark a major buying opportunity if the US can stave off a recession. If not, we have more pain to go where a 35% recessionary decline below the current 4,749.32 bottoms-up estimate would provide a price target of 3,087.

Monetary policy and market tightening impact the economy with a lag, such that the current jump in long-term UST rates and the fed funds rate argues the ISM PMI will be declining well into 2023, making the odds of a soft landing a highly unlikely event and argues the lows are not in.

To learn more about Financial Sense® Wealth Management, click here to contact us.

Advisory services offered through Financial Sense® Advisors, Inc., a registered investment adviser. Securities offered through Financial Sense® Securities, Inc., Member FINRA/SIPC. DBA Financial Sense® Wealth Management.

Copyright © 2022 Chris Puplava