The dollar has been in a long term structural decline since 2001 with the USD (United States Dollar) Index down roughly 40% into its 2008 lows. Since mid 2010 when Bernanke hinted at QE 2 the dollar’s intermediate term picture has also been negative. However, over the last few months it has been gaining strength and its short term bullish trend is currently colliding with its long term bearish trend. Given the dollar’s reserve currency status and interconnectedness with world financial markets, the resolution of whether its short-term bullish trend or bearish long term trend win out will have major investment implications ahead.

Long Term Bearish Picture

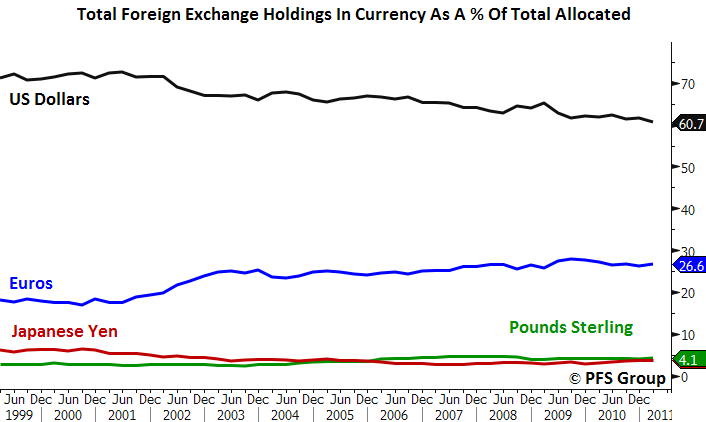

Ever since the USD Index peaked in 2001 it has lost ground relative to global currencies. Much of the decline occurred in the first two years in which the USD fell over 30% against a basket of world currencies by its 2004 low. Former Fed Chairman Alan Greenspan began to hike short term US interest rates in 2004 which gave a boost to the dollar as country interest rate differentials with the US decreased. However, the relative long term bullish fundamentals of foreign countries relative to the dollar, particularly emerging markets, asserted themselves and the dollar quickly lost ground. Since 2001, its share of world currency holdings has fallen from more than 72% to a recent low of 60.7% this year. The Euro has served as the primary benefactor by rising from a low of 17% of total world foreign exchanging holdings in 2001 to its recent level of 26.6% this year.

Source: Bloomberg

As stated above, the first leg down in the secular bearish trend for the dollar occurred between 2001 to the 2004 low in which the USD Index fell 33.4%. The second leg of the decline occurred from the 2005 top to the 2008 low which saw the USD Index fall 22.7%. Since 2008 the Index has been in a broad trading range making a series of lower highs and higher lows. However, its consolidation over the last several years ended this year as it looks like the dollar started its third leg down in its secular bearish decline. This can be seen below with a break of the bullish support line connecting the 2008, 2009, and 2010 lows.

Source: Bloomberg

Short Term Picture is Bullish

Of note is that the bearish intermediate term trend (yellow line above) that has been in place since mid 2010 when Bernanke hinted of QE2 has been broken to the upside with the USD Index now above its 200 day moving average (green line) and hitting the underside of the broken 2008-2010 trend line. We are at a key pivotal moment in which we do not know if the 2011 breakdown in the USD was a continuation of another major leg down or just a false breakdown with another major USD rally ahead. This is of key significance as so many asset class returns are related to USD performance. This can be seen below in which the correlation of asset classes and equity sectors to the dollar is shown. As you can see, dollar strength would have a negative affect on the Euro, emerging market stocks, commodities, the S&P 500, and commodities like oil and to a lesser extent gold, but be beneficial to corporate bonds and other fixed income assets. The lower table below shows that every S&P 500 sector shows a negative correlation to the USD to the same degree. What the data below shows is that if the USD is going to rally then we would likely expect foreign currencies to decline as well as stocks, and commodities, while the fixed income market would benefit.

Source: Bloomberg

However, if this is just an oversold rally to test the underside of the broken 2008-2010 trend line, then the reverse would occur in which stocks, commodities, and foreign currencies would do well while fixed income investments would fall. Unless Ben Bernanke comes out with another massive QE3 program to devalue the dollar, the current intermediate bounce looks like the real McCoy given the weakness in foreign currencies relative to the dollar over several time frames. Most importantly, it is not just gaining strength against the Euro but also against nearly every other world currency (including the four major metals: gold, silver, palladium, and platinum) as the table below shows:

Source: Bloomberg

Absent a significant QE3 program by the Federal Reserve it looks like we will be treated to an intermediate bounce in the dollar which will cause most assets to decline except for US Treasuries. However, if Bernanke significantly expands the Fed’s balance sheet we may be treated to the third major leg down in the dollar with risk assets benefiting the most, particularly precious metals. It will be important to keep a close eye over the next week to see if it will break back above the 2008-2010 bullish trend line or if it will get rejected and set the stage for another leg down in the devaluation of the USD.