Markets had a mini riot at the start of the year with the release of the Federal Open Market Committee’s (FOMC) December meeting minutes. As many are now aware, the Fed changed course and tied its zero-interest-rate-policy (ZIRP) to economic measures, stating the Fed would keep rates near zero as long as unemployment remained above 6.5% and inflation below 2.5%. To help achieve sustainable growth and to foster full employment the Fed embarked on what some call QE4 in which it added to the $40B/month mortgage debt purchase program (QE3) by announcing an additional $45B/month of Treasury purchases. The combined $85B/month asset purchase will add more than $1 trillion to the Fed’s balance sheet to the tune of $4 trillion total by the end of the year.

What startled the markets was that investors assumed that both ZIRP and QE were being tied to the economy while the minutes made clear no such language was made explicit for QE as reflected in the following Bloomberg article:

Fed’s Bullard Sees Difficulty Tying QE to Economic Levels

Minutes of the Fed’s December meeting show a split among policy makers over how soon the QE program should end. “Several” members of the FOMC said it would “probably be appropriate to slow or stop purchases well before the end of 2013,” according to the minutes. A “few” were willing to let the program run to the end of the year while “a few others” didn’t give a time frame.

Although Bullard said he thinks that a drop below 7% unemployment may be the threshold to end QE, investors will be looking for clarity when the Fed Chairman Bernanke speaks on Monday. While there is great uncertainty for the market to gauge how long the Fed will maintain QE with some fearing it may end later in the year, I can give you $3 trillion reasons why the Fed won’t end QE this year, and $4.5 trillion reasons why we will likely be talking about QE through 2017.

Before the year is out the US government has $2.90T in Treasuries maturing this year and will be paying more than $212B in interest on its debt. As shown in the figure below of the government’s debt distribution, the U.S. will be paying more than $1T in debt repayment and interest annually from now through 2017.

Source: Bloomberg

Back in 2012 I did a study on Japan’s debt distribution and simply looking at the maturity schedule of Japan’s debt outstanding made it clear that the Bank of Japan (BOJ) would need to be an active buyer as there was just too much debt that needed to be rolled over for the financial markets to absorb.

Consider Massive Japanese Debt Monetization Is Coming, Yen to be Devalued

You can only stretch a rubber band so far before it snaps back or is torn, so too is the case with government indebtedness. There eventually comes a point when the road ends and the can hits a brick wall. It appears that Japan is rapidly approaching that brick wall and there are two likely outcomes. One option is that the bond vigilantes revolt and yields on Japanese debt spike or the second option is a massive debt monetization by the Bank of Japan (BOJ). Given the massive amount of debt relative to the Japanese economy and associated interest payments on the debt, Japan can’t afford a sharp rise in yields. Thus, it appears the BOJ is likely to step in and monetize the debt and the currency markets may be signaling this very outcome.

I performed the same analysis on the world’s top 10 debtor nations, which led me to conclude Global QE Is Coming: Let the Gold Mania Begin!, where I reported:

Nearly 50% of the total outstanding debt of the world's top 10 debtor nations needs to be rolled over by the end of 2015. While fears over a European contagion and a hard landing in China have driven investors into sovereign debt like the U.S. and Japan, how long can this continue and will investor demand for sovereign debt be able to soak up the total supply over the next few years? It is my belief that global central banks will be the buyers of last resort and will be monetizing the debt in massive quantities over the next two and half years. This may perhaps be the catalyst leading to the mania phase for gold as investors all over the world attempt to protect themselves from global quantitative easing and global currency debasement.

Looking at how much debt the US government is going to have to roll over this year and in the years to come, I can’t foresee how the financial markets will be able to absorb all that debt and it is likely that the Fed will continue to be a major buyer of U.S. debt for years to come.

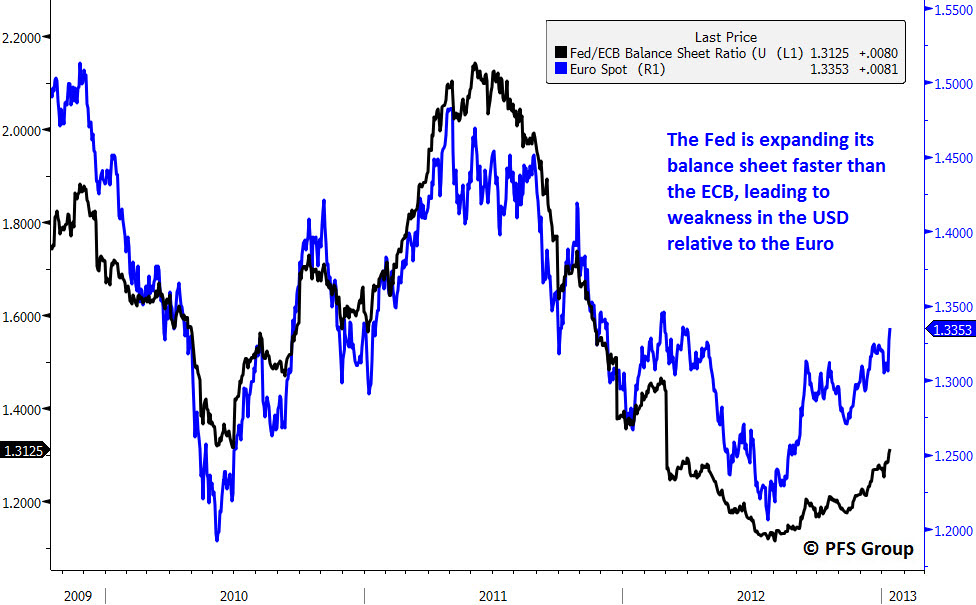

Asset purchases by central banks are not only being used to absorb various governments’ massive debt rollovers, but also to help stimulate their economies through currency wars (Click for video link, “Jim Rickards: A Currency War Simulation”). By expanding one’s balance sheet at a faster pace relative to others, a central bank can cheapen its currency to help spur exports. The link between currency exchange rates and central bank balance sheets is clearly demonstrated by the charts below for the EUR/USD a YEN/USD exchange rates.

Source: Bloomberg

Source: Bloomberg

With sluggish economic growth due to burdensome debt levels in developed economies coupled with massive sovereign debt rollovers for years to come, we are likely to not only see the Fed continue its QE program but also other global central banks. So when you hear commentary about the end of QE out of strategists and FOMC members, remember we heard this as other QE programs were winding down only for the Fed to launch yet another QE program. Until we work through our trillion dollar debt rollovers out to 2017, QE is here to stay.