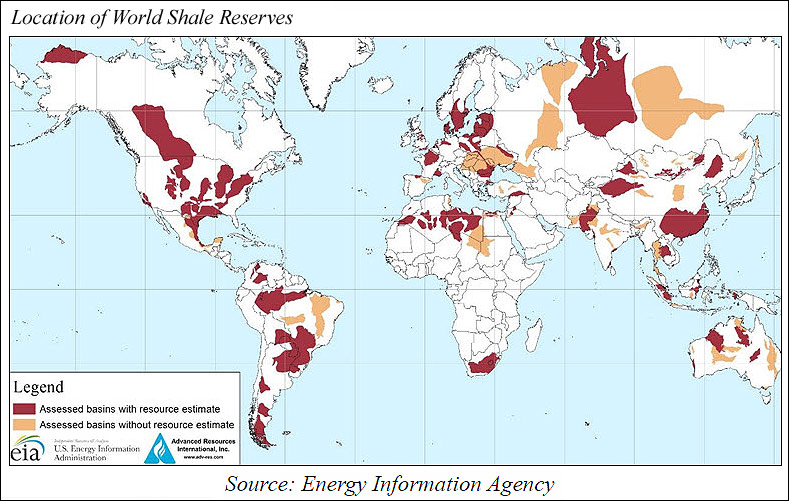

Last month the Energy Information Agency (EIA) published an update to its 2011 assessment of shale oil and gas resources in 41 countries outside the United States. After just two years, there was enough new data to warrant a new report; this is a field where information is scarce and subject to radical revision on the basis of new discoveries.

The current report adds about 11 percent to global technically recoverable shale oil reserves, and about 47 percent to global technically recoverable shale gas reserves. There were some sharp changes in estimates, which is to be expected given the preliminary nature of the data.

Estimated reserves were revised sharply down for fields in Norway, Poland, and South Africa. More modest downward revisions were made for China and Mexico. We can anticipate many more such revisions in the future as exploration continues and more potential fields come under competent geological scrutiny.

Nevertheless, the breakdown by country is interesting:

We noted immediately the size of China’s gas reserves. Does this mean that the potential renaissance of U.S. industry, fueled by its comparative advantage in energy costs, is in jeopardy? Not necessarily.

The key is the distinction between technically recoverable resources and economically recoverable resources.

While technically recoverable reserves, which are what the EIA report evaluates, are comprised of all resources that can be recovered with current technology, economically recoverable reserves includes only those resources which would be profitable to extract at current market prices. In short, the usefulness of hydrocarbons in the ground depends fundamentally on political and economic conditions above the ground. And here, the advantage is still with North America. The report notes:

“Recent experience with shale gas in the United States and other countries suggests that economic recoverability can be significantly influenced by above-the-ground factors as well as by geology. Key positive above the ground advantages in the United States and Canada that may not apply in other locations include private ownership of subsurface rights that provide a strong incentive for development; availability of many independent operators and supporting contractors with critical expertise and suitable drilling rigs and preexisting gathering and pipeline infrastructure; and the availability of water resources for use in hydraulic fracturing…

“The market effect of shale resources outside the United States will depend on their own production costs, volumes, and wellhead prices. For example, a potential shale well that costs twice as much and produces half the output of a typical U.S. well would be unlikely to back out current supply sources of oil or natural gas. In many cases, even significantly smaller differences in costs, well productivity, or both can make the difference between a resource that is a market game changer and one that is economically irrelevant at current market prices.”

We believe that despite the presence of significant shale oil and gas reserves outside North America, the factors referred to above will continue to make U.S. shale oil and gas extremely competitive compared to the unconventional resources of other countries lacking the U.S.’ industrial, legal, and political infrastructure. Very bullish for the US.

To Learn How to Receive the Full Premium Commentary, Please Click the Following Link: Gold Subscription