Originally posted at Briefing.com.

Not that long ago, one of the main storylines in the market narrative was that the US economy was headed for a recession. With a string of some better than expected economic data of late, that storyline has been re-written and now the narrative suggests the US economy is not headed for a recession.

Surging oil prices and a surging stock market have been huge factors contributing to the shift in the narrative and to the dramatic turn in market sentiment that has resulted in a 10.1% gain for the S&P 500 over the last month.

With the way things have been going, though, it probably won't be long now before the narrative shifts again, only the next shift is apt to have that concerning tone to it again.

Why? Because many of the factors that were touted as ultimate sources of support for the economy and the market during the downturn earlier this year are morphing into ultimate sources of resistance for the economy and the market in the wake of the recent upturn.

Oil

How long have we been hearing that falling oil prices and falling gas prices are ultimately a good thing? They are a cost savings for many companies using oil and its derivatives for production inputs and a de facto tax cut for consumers.

Well, as we have discussed in past posts, profit margins have been coming down for many companies despite the lower oil prices and consumers have been slow to step up their discretionary spending, opting instead to pay down debt and/or to save their gas price savings.

Accordingly, with oil prices moving from nearly $26.00 per barrel to nearly $40.00 per barrel since February 11, energy costs won't be thought of as the tailwind they used to be.

See Gary Shilling: All-Out Price War Could Send Oil to $10 to $20 a Barrel

Average gasoline prices, meanwhile, have bumped up to $1.84 from $1.72 in mid-February.

That average price is still 25% below the average from a year ago, yet a newly-established uptrend wouldn't necessarily be the friend of consumers just ahead of the summer driving season, knowing, in particular, the reluctance consumers have shown in spending their gas price savings on the way down. That de facto tax cut, then, could soon be mentioned as a fading source of support.

Market Rates

Falling interest rates have been touted as an important source of support for the housing market and the stock exchange. They have been climbing of late, though, and pretty rapidly at that as the US recession premium has been rinsed out of the Treasury market.

The yield on the benchmark 10-yr note is still 33 basis points below where it started the year, but again, the new trend has taken away some of the lusters from the argument that declining rates can help justify a premium valuation for the stock market and a potential boom in home purchase demand.

Valuation

We touched on the matter of valuation in last week's column, yet it is relevant for this week's article as well.

With the run in the stock market, the S&P 500 now trades at 17.3x estimated forward twelve-month earnings, according to S&P Capital IQ. Long-term rates have come down some since the start of the year, but so have earnings growth estimates.

The latest report from S&P Capital IQ indicates calendar 2016 earnings are expected to grow just 1.7% now versus 7.4% on January 1. As an aside, first-quarter earnings are projected to decline 6.8%, which is down from the 1.2% growth rate expected on January 1.

Sure, it's nice to know that an economic recession may not happen in the US, yet it would be remiss not to note that we are in an earnings recession.

Check out Strategist that Warned of Market Peak in 2007 Says to Get Defensive

The first quarter would be the third straight quarterly decline in earnings based on S&P Capital IQ data. What's more is that second quarter earnings are currently projected to decline 2.0%.

Hence, the S&P 500, which traded down to 1810.10 on February 11, and was deemed "attractive" at 15.5x estimated forward twelve month earnings at the time, is no longer as attractive at 17.3x estimated forward twelve month earnings today with the yield on the 10-yr note 30 basis points higher than it was on February 11.

The 15-year average forward P/E ratio is 16.0x.

The Fed

Speaking of rates, there is that little thing called the Fed funds rate. A short time ago, when global stock markets were convulsing, credit spreads were widening, and economic data was disappointing, the Fed funds futures market priced out any probability of another hike in the fed funds rate until 2017.

Traders there have been forced to re-think that outlook now that global stock markets have come roaring back, and economic data has been surprising more to the upside (which isn't the same as saying it has been strong).

The latest data from the Fed funds futures market shows a 52% probability of a rate hike at the July meeting. If the economic data continue to produce positive surprises, and oil prices keep rising, there is likely to be some growing angst that the Fed will raise rates multiple times this year on its path toward normalization.

This could be problematic because the fed funds futures market, for the most part, continues to be positioned for the "under" regarding how many times the Fed could raise rates this year.

The March 15-16 Federal Open Market Committee meeting, and subsequent press conference to explain the Fed's projections will soon provide new insight for market participants to digest.

Sentiment

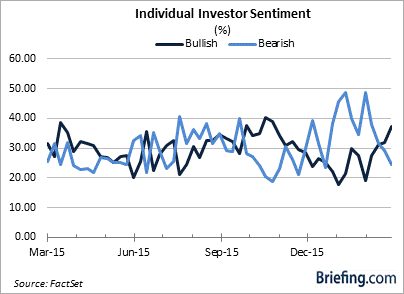

Finally, investor sentiment was a great tailwind for the market in mid-February, not because it was so good, but because it was so bad.

The American Association of Individual Investors reported bullish sentiment stood at just 19.2% on February 12, which was well below the long-term average of 38.6%. Bearish sentiment stood at 48.7%, which was well above its long-term average of 30.3%.

With investor sentiment being a contrarian indicator, it was said then that the market was primed for a big rebound effort, and, boy, has that proven accurate.

With the aforementioned rebound, bullish sentiment has pushed up to 37.4% in the latest report while bearish sentiment has dropped to 24.4%. The tailwind of negative sentiment, then, isn't as opportunistic as it used to be. On the contrary (pun intended), the improved sentiment is turning into a headwind.

What It All Means

This market rally has been extraordinary. We knew the potential was there for a rebound of some kind, yet we didn't envision the scope of the rebound we have seen.

What we can't get past at this point, though, is that the rally has transpired as earnings estimates have continued to decline; moreover, it has been forged on the otherwise inauspicious reason that the US economy isn't going to suffer a recession soon.

Okay. That's somewhat akin to being overjoyed that you're not going to see your pay cut even though you also aren't going to get a raise soon. No raise is certainly better than a pay cut, or losing one's job altogether, but when there are rising bills to pay, the enthusiasm for not getting a pay cut eventually dies down.

The stock market has had a great run since mid-February. There is no denying that. The reasons why have been expressed in the market narrative, and there will continue to be a lot of discussion about the meaning of the rally.

You may also like Technician: Still Looks Like a Bear Market Rally

We're not sold, however, on the notion that the stock market is on course now for big gains this year. It can't be—or certainly shouldn't be—given the declining state of corporate earnings and the otherwise sluggish state of the global economy.

Despite the big rally, that fundamentally important narrative still hasn't changed.