Last week, Fed Chairperson Yellen indicated that the Fed was likely to raise its policy interest rates sometime before year end. Given the behavior of the sum of commercial bank credit and depository institution reserves at the Fed in the past three quarters, it is a mystery to me why the Fed would be contemplating a policy interest rate increase at this juncture. But if this is something the Fed just has to get out of its system, then the first increase is unlikely to be followed by a second interest rate increase for some time.

To briefly review my focus on the sum of commercial bank credit and reserves at the Fed , because depository institutions (commercial banks, savings institutions and credit unions) are required to hold only a fraction of the amount of their deposits as reserves at the Fed, they are able to create credit by an amount that is a multiple of their reserves. This credit is figuratively created out of thin air. The reserves that depository institutions hold at the Fed are, in fact, created by the Fed. When an asset item on the Fed’s balance sheet increases, say a Fed purchase of securities, a liability item on the Fed’s balance sheet also increases. One liability item on the Fed’s balance sheet is reserves owed to depository institutions. So, these reserves, which serve as the “seed money” for the credit created by depository institutions, also are figuratively created out of thin air.

[Listen to: Jim Puplava’s Big Picture: Slow and Shallow – The Next Fed Interest Rate Cycle]

Entities typically borrow in order to purchase something – a good, a service, a financial instrument. When the credit that is financing purchases is created out of thin air, net spending in the economy increases as the borrowers increase their spending and no one else cuts back on his/her spending. In contrast, when the credit that is financing purchases emanates from new saving, then the change in net spending in the economy is zero. Saving is the act of curbing one’s current spending and transferring this purchasing power to a borrower. So, the borrower increases his/her current spending and the saver decreases his/her current spending.

Plotted in Chart 1 are the year-to-year percent changes in the sum of depository institution credit and reserves held at the Fed along with the year-to-year percent changes in nominal Gross Domestic Purchases. Gross Domestic Purchases are expenditures by U.S. households, businesses and government entities on newly-produced goods and services. So, expenditures on imported goods and services are included in Gross Domestic Purchases while expenditures by foreign entities on U.S.-produced exports of goods and services are excluded. From 1953 through 2014, the contemporaneous correlation between percent changes in thin-air credit and percent changes in Gross Domestic Purchases is 0.59 out of a maximum possible 1.00. Gross Domestic Purchases does not include the value of used products purchased (e.g., used cars and existing homes) and does not include the value of financial instruments purchased. If a measure existed that added these excluded items to Gross Domestic Purchases, it is likely that the correlation between its changes and changes in thin-air credit would be even higher than 0.59.

Chart 1

So, now you know why I am obsessed with thin-air credit with respect to monetary policy. The behavior of thin-air credit plays an important role in behavior of nominal spending in the economy. If the growth in thin-air credit is rapid, the risk of the economy overheating and/or the formation of asset-price bubbles would be heightened. If growth in thin-air credit were rapid, increases in Fed policy interest rates would be entirely appropriate in order to prevent a rise in the inflation rate of goods/services and/or asset prices.

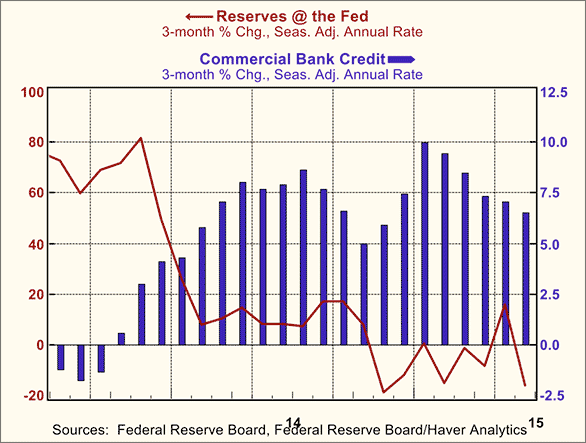

But, as shown in Chart 2, growth in a subset of total thin-air credit, the sum of commercial bank credit and reserves at the Fed, has been decelerating in recent quarters and is below its long-run median growth rate. Chart 2 contains growth rates in the sum of commercial bank credit and reserves at the Fed. Commercial bank credit accounts for over 80% of total depository institution credit. The Fed reports commercial bank credit weekly with a one-week lag, whereas it reports total depository institution credit only quarterly with about a one-quarter lag. The long-run median growth rate in the sum of commercial bank credit and reserves at the Fed is 7.1%. As shown in Chart 2, growth in the sum of commercial bank credit and reserves at the Fed was 6.0% in Q2:2015 vs. Q2:2014. Moreover, the growth in the sum of commercial bank credit and reserves at the Fed has been trending decidedly slower starting in Q4:2014, when the Fed terminated its QE program. Quarter-to-quarter annualized growth in the sum of commercial bank credit and reserves at the Fed slipped to 5.1% in Q2:2015 and its trend growth has been decelerating since Q4:2013. This current below “normal” growth in the largest component of thin-air credit implies that the dangers of a near-term overheated economic environment and/or inflation of an asset-price bubble are low.

Chart 2

The principal factor accounting for the recent slowing in the growth of thin-air credit is the Fed’s contribution, reserves at the Fed. This is shown in Chart 3, in which 3-month point-to-point annualized growth rates are plotted instead of growth rates of quarterly averages. Starting in November 2014, the month after the Fed’s QE program ended, the three-month annualized percent changes in reserves at the Fed, with two exceptions, have been in negative territory. That is, since the end of QE, reserves at the Fed have contracted on net. But the bank-credit component of thin-air credit also has demonstrated a slowing growth trend. After surging in the three months ended January 2015 at an annualized growth rate of 10%, growth in commercial bank credit slowed to a below “normal’ rate of 6.5% in the three months ended June 2015.

Chart 3

Again, the current behavior of thin-air credit does not portend an acceleration in the rate of price increases for goods/services or assets. And the recent behavior of these price changes would not seem to warrant concern by the Fed. Consumer price inflation, as represented by the Personal Consumption Expenditure price index, remains tame. In the three months ended May 2015, this measure of consumer price inflation had increased at an annualized rate of 2.2%, recovering from the price declines earlier in the year due to falling energy prices (see Chart 4). Commodity prices of all stripes have been trending lower in recent months, as shown in Chart 5. And asset prices are not racing to the moon (See Chart 6).

Chart 4

Chart 5

Chart 6

So, current inflationary pressures are quite mild here in the U.S. The current rate of growth in U.S. thin-air credit is below its “normal” rate, suggesting that credit creation is not fostering a future surge in U.S. inflation. And the global inflationary environment appears equally tranquil, if not more so. The Chinese economy, which already had experienced a growth slowdown, will now be negatively affected by its recent stock market swoon. And Europe is not exactly booming, Greece aside. Given all this, it is not clear what is motivating the Fed’s desire to raise its policy interest rates sometime later this year. Whatever the motivation, if the Fed does pull the interest-rate tightening trigger in 2015, it will not likely do so again for many months thereafter. In other words, for Fed interest rate hikes in 2015, it’s one and done.

Note: The views expressed in this commentary solely reflect those of Econtrarian, LLC.