Introduction

How fast can the Canadian economy grow? What can Canadians expect now that commodity prices have plunged and the country is running a trade deficit?

These questions take on greater significance with the shift in political power to the Liberals who campaigned on growth through fiscal stimulation and government deficits. Government revenues are tied closely to a nation’s capacity to growth; higher incomes provide room to stimulate the economy without generating deficits. This blog discusses Canada's potential and expected growth against weakened commodity prices, a slowing international economy, and accompanying deflationary pressures.

Read: Canada Joins the Currency Wars

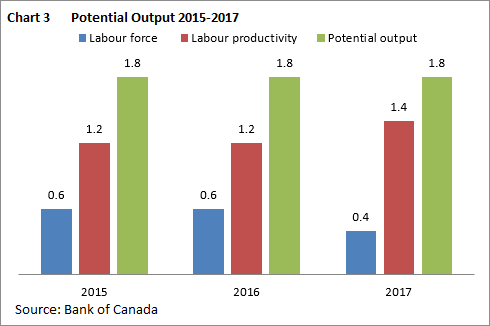

Estimating a nation's potential GNP is simple: combine yearly changes in the labor force with yearly changes in labor productivity. More workers and greater efficiency increases potential output. The gap between potential and actual GNP growth is the unemployment rate. Falling short of potential growth results in underemployment.

What Is Behind Canada's Poor Economic Performance

Both Canadian labor force and productivity have grown by 0.9% annually. The combined growth of 1.8% , however, is insufficient to provide full employment; unemployment averaged 7.2% over the period well above conventional estimates of full employment around 5%.

Changes in the labor force are basically predetermined by demographic trends, but changes in productivity are quite variable. Capital investment and technological innovation affects the efficiency of every worker. Human capital in the form of worker skill and experience also generates greater labor efficiency.

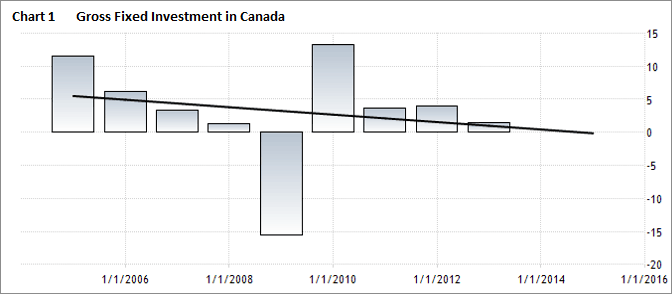

While Canadian capital investment varies from year to year, investment has steadily declined over the past few years. The trend is for increases in capital expenditures to continue to decline, especially in the resource sector. This steady reduction in the growth of investment contributes to the mediocre labor productivity.

One reason for the slowdown in capital expenditures relates to capacity utilization. As long as there is excess capacity, a corporation does not feel compelled to expand its facilities. Chart 2 shows the persist decline in the capacity utilization rates for Canada. Lower operating capacity means lower output levels and a reduction in the work force. The combined effect of low capacity utilization and jobs losses puts Canada even further below its potential growth path.

On the demand side, Canada continues to struggle. Gross Domestic Product over the past 12 months has increased by just 1%; industrial production rose only 0.6%; and the unemployment rate moved up slightly to 7.1%. Canada continues to operate below potential in part because domestic demand is insufficient to restore economic growth.

Destroying Capacity

This has been a major concern of the Bank of Canada (BoC). In its October 2015 Monthly Policy Report, the BoC raised the issue of how capacity continues to be destroyed.

The BoC points out that the boom in commodity prices since 2001 generated strong investment in the extraction sector, increasing demand for labor, raising wages, and attracting workers from other sectors. This significantly raised production capacity, especially in Western Canada.

However the energy sector's expansion resulted in other sectors contracting. Over the same period, non-energy sectors struggled mightily against the appreciating Canadian dollar. Industry Canada estimates that 300,000 manufacturing jobs have been lost in Ontario and Quebec since 2004. The BoC argues that "in the non-resource traded-goods sector, firm exit was widespread and some physical capacity was destroyed which would, therefore, be not available for subsequent expansion." Estimates for the amount of destroyed capacity range as high as 5% of total economic capacity.

Related: Gary Dorsch: “Hundreds of Billions” in Defaults if Commodity Crash Continues

Concluding Remarks

1. Canadian growth potential has been lowered in large part because of dramatic changes in the world markets for our goods, both energy and non-energy.

2. Non-energy firms need to improve their competitive positions and take advantage of the lower Canadian dollar with greater exports.

3. The resource extraction sector will continue undergoing painful adjustments as it aligns future capital investment to meet the reduced demand for oil, gas, and other commodities.

4. The big issue concerns the fiscal side. As the economy adjusts to slower growth, the concern is that governments at all levels will be challenged to generate revenues to meet voter expectations for new expenditure programs. Yet without greater fiscal stimulus the economy will not be able to return to move positive growth path.