The following is based on our recent podcast, which can be listened to on our site here or on iTunes here.

There are close to 76 million baby Boomers (born between 1946 and 1964) alive today representing 28% of the total US population. Starting in 2011, an estimated 10,000 Boomers have been retiring every day and that trend will continue for at least another 10 years. They represent the largest retirement contingent in US history placing strains on both Social Security and Medicare.

If current laws generally remain unchanged, the US government deficit will increase nearly every year over the next decade and, according to the Congressional Budget Office, rise to the highest average level in the last 50 years. The reason is growth in Federal revenues will be outpaced by spending, particularly for Social Security, Medicare and interest payments on government debt. Whether you refer to it as an approaching fiscal crisis or retirement crisis, the Baby Boomer retirement wave is the country’s biggest and most predictable train wreck.

Unlike their parents’ generation, who had guaranteed pensions and Social Security, Boomers are less fortunate. Most defined benefit pension plans have been replaced by defined contribution plans that offer no set guarantees in salary replacement. Boomers will be more reliant and dependent on their own savings and Social Security. Unfortunately, Boomer savings fall short of meeting retirement expectations. According to recent survey results from the Insured Retirement Institute, Boomer satisfaction, confidence, and retirement preparedness have fallen steadily since the survey's inception in 2011 despite positive equity returns, low market volatility, and improving consumer sentiment. Among the survey’s results are issues which plague successful retirement outcomes:

- Only 55% of Boomers have saved money for retirement.

- 59% of Boomers cite Social Security as their major source of retirement income.

- Health care costs consume 33% of income amongst Boomers age 60 and over.

- Economic satisfaction has fallen from 76% in 2011 to 43% in 2016.

- 1 in 3 Americans has __spamspan_img_placeholder__ saved for retirement.

- Women are less prepared for retirement than men.

- 28% of Americans over 55 have no retirement savings.

The facts listed above point to a trend in Boomer retirement that will be more difficult than their parents’ and, potentially, vastly different than the one they planned. Life expectancies have lengthened which adds strains to retirement nest eggs. Longer lifespans also mean healthier and more active lifestyles which consume more money. Medical costs are rising faster than average inflation rates for retirees and retirement nest eggs have been devastated by two bear markets and the lowest interest rates in recorded history. The combination of these factors—greater longevity, higher medical care costs, financial repression, and rising inflation—has led to the “four horsemen of the retirement apocalypse”: major obstacles that could impact Boomer retirement outcomes leading to one out of five Boomers ending up broke at the end of their retirement.

First Horseman: Longevity

According to data compiled by the Social Security Administration:

- A male age 65 today can expect to live, on average, until age 84.3.

- A woman age 65 today can expect to live, on average, until age 86.6.

- One out of every four 65-year olds today will live past age 90.

- One out of ten 65-year olds will live past age 95.

The good news is most Americans are living longer and living healthier lifestyles. However, longevity and healthier lifestyles will lead to a greater drawdown of assets over a longer period of time. The average married couple can plan on living 25 years in retirement between both spouses. Longer lifespans mean portfolio assets will have to cover a much longer time period and longevity also raises the risk that one or both spouses could end up in a long-term care facility, which could deplete asset portfolios rapidly.

One of the greatest worries among retirees is the risk of outliving their savings or dying broke. According to analysis by the Employee Benefits Research Institute, roughly 1 in 5 individuals age 85 and older who died between the years 2010 and 2012 had no assets other than a home, 1 in 6 died broke, and 1 in 10 died with an average debt of ,000.

As much as longevity poses a risk, it also presents an opportunity. Longer and healthier lifestyles can lead to delayed retirement by working longer in a full-time or part-time capacity or even starting a new career in a different field. Choosing to delay retirement can mitigate some of the risk issues of outliving assets by allowing more years to accumulate savings and fewer years spent drawing down assets. Social Security benefits can also increase by delaying benefits to age 70.

Second Horseman: Medical Costs

Next to taxes, health care costs can be one of the biggest expenses in retirement, an expense few retirees have planned for adequately. Most retirees assume that Medicare will cover most expenses or that medical costs will be negligible, neither of which are true. The reality is Medicare covers a lot less than most individuals plan for in their retirement. Longevity adds to those costs posing the risk that healthy individuals are more likely to be saddled with higher medical expenses due to longer lifespans.

According to a Fidelity study, the average married couple will spend 0,000 for medical expenses throughout their retirement. These out-of-pocket expenses include Medicare premiums, Medigap insurance, co-payments, deductibles, drug and other medical expenses from dental to vision care. As an individual ages, out-of-pocket expenses accelerate.

This large sum of 0,000 averages out to an additional expense of ,000 a year and double that amount for higher income couples whose income ranges between 4,000-7,000 per year. As an individual's or couple's income increases above ,000, as shown below, Medicare Part B premiums can rise from 9/4 to 8.60—a 293% increase.

Source: Insured Retirement Institute

The major costs above do not include the cost of chronic illness or black swan events like dementia or Alzheimer’s disease, which can often require long-term private care and run as high as ,700 a month.

| Long Term Care Costs: Monthly National Median 2016 | |

| Homemaker Services | ,813 |

| Home Health Aide | ,861 |

| Adult Day health care | ,473 |

| Assisted Living Facility | ,628 |

| Semi-Private Room | ,844 |

| Private room | ,698 |

Source: Genworth

The cost of health care expenses in retirement can be formidable but they can be mitigated through careful planning. The good news is that these expenses don’t come in a lump sum but add up over time, which makes it easier to manage. They can be planned for by setting aside an amount each year to cover future health expenses through an HSA (Health Savings Account), which allows for tax-free withdrawals when used for medical expenses. Long-term health care expenses can be covered by taking out policies at an early age when the policies are affordable or by simply setting aside and including future health care expenses in the annual budget. The key is to build flexibility and plan for uncertainty.

Third Horseman: Financial Repression

If there is one remarkable event today that has caught those in or near retirement by surprise it's interest rates, which are the lowest they have been in recorded history. This is affecting those planning for retirement in different ways. For those who are years away from retirement, it means lower returns on their investments, requiring more in additional savings or more time to accumulate the necessary funds in order to retire. For those retired, the returns on safe investments have been much lower than planned for, producing less income to live off, requiring lifestyle adjustments, or forcing retirees to go further out on the risk curve.

The fact remains that interest rates remain well below historical norms and, I believe, are likely to remain that way for years to come despite the Federal Reserve’s plans to gradually raise interest rates over the next few years. With a burgeoning debt balance, it is in the government’s best interests to keep interest rates artificially suppressed through central bank policies as a means of managing a debt balance that is growing faster than economic growth.

One other factor retirees and future retirees have to contend with is stock market valuations. According to the Shiller PE Ratio, the S&P 500 is the third most expensive on record. History has shown that expensive markets are followed by bear markets and lower future returns. A recent example is a history of the S&P 500 following the tech bubble. Price earnings multiples for the S&P 500 in 2000 were the most expensive in the history of the index. The result was a secular bear market that lasted 13 years.

Even with dividends reinvested, the total returns during that 13-year period were barely above 2% annually, a far cry from investment models used in planning that often assume historical rates of return around 10% a year.

If history teaches us anything, it’s that markets display a strong propensity to mean revert; euphoric and expensive markets are followed by periods of lower returns. Over long periods of time—the last 30, 50, or 100 years—market returns have been stellar. However, unless you are 25 years old and just starting your working career, most individuals don’t have 30-50 years to average their returns and ride out a secular bear market or two.

Retirees will have to be much more active and informed and learn to navigate future markets that will prove to be more uncertain, more volatile, and less predictable. The days of passive investing are over, in my opinion, as investors will need to learn to adapt to rapid and changing markets. The days of set-and-forget are over and could be dangerous to one’s financial health.

Fourth Horseman: Inflation

Inflation has been called the silent killer. It creeps up slowly and unannounced and catches us by surprise. Outside of health issues, inflation is the one aspect of retirement that can devastate plans, alter one’s lifestyle, and, in a worst-case scenario, leave one broke at death.

President Ronald Reagan once commented on inflation by saying “Inflation is as violent as a mugger, as frightening as an armed robber, and as deadly as a hit man.”

| Cost (US average) | 1960 | 2016 | % increase |

| New home | ,500 | 8,000 | 1,645 |

| New car | ,500 | ,300 | 11,420 |

| Gallon of regular gas | __spamspan_img_placeholder__.31 | .95 | 529 |

| First-class stamp | __spamspan_img_placeholder__.04 | __spamspan_img_placeholder__.47 | 1,075 |

| Dozen eggs | __spamspan_img_placeholder__.57 | .08 | 265 |

| Gallon of milk | __spamspan_img_placeholder__.49 | .19 | 551 |

Data sources: BLS.gov, inflationdata.com

The long run inflation rate has averaged 3.77% since WWII. The good news is that it has been coming down over the last few decades averaging 3.4% in the 1990s, 2.76% in the last decade, and 2.1% in the last year.

The bad news is that it still remains a major cost factor in retirement. That is because retirees are subject to much higher health care inflation rates than working Americans. According to Fidelity’s health care cost estimator, 2016 costs rose by 6%, the highest since the survey began in 2002.

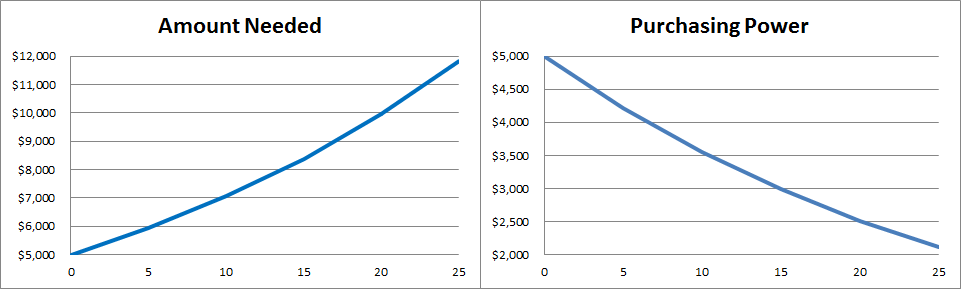

Inflation impacts retirement in several ways. The amount needed to retire will be greater and lifestyles will be reduced unless planned for. Two examples illustrate this point. Assume a retired couple lives on an income of ,000 a month. The graph on the left illustrates the amount needed to maintain the same lifestyle with a 3.5% inflation rate, the average over the last 70 years, over a 25-year period. The graph on the right shows the purchasing power of 00 over time, which at 3.5% inflation equates to a 58% reduction over 25 years. Put another way, it would take ,816 to buy the same goods and services that ,000 does today.

Most retirement plans focus on a single number—a targeted magical figure that makes one's retirement goals achievable. However, many of these plans use investment returns that no longer hold up. The historical returns used in most models assume rates of return based on the last 100 years where stocks returned 10%, government bonds 5.5%, and US Treasury bills 3.5%. The reality of investment returns has been much different since the beginning of this new millennium. Since the year 2000, stocks and bonds have yielded an annual return of around 5% with Treasury bills around 1.8%. On the day this was written, the yield on a 10-year Treasury note was 2.47% and on a 3-month T-bill 0.548%. The returns over the last 16 years are a far cry from the returns used in most retirement planning investment models.

More modest investment returns are called for which greatly changes retirement outcomes and retirement dates. This reality is altering the outcome of retirement planning. The key to meeting retirement goals rests on two simple premises:

- Begin saving and investing early.

- Invest regularly.

Outside these two realities, the more probable outcomes for most retirees are one of four outcomes:

- Delaying retirement to a later date.

- Working part time in the early retirement years.

- Reducing standards of living and lifestyles.

- Moving to a less expensive locale or state.

Unpleasant outcomes can be avoided with proper planning and using realistic savings and investment returns. Most desired retirement goals can be achieved my making the appropriate adjustments listed above. Part of any good plan also requires monitoring and making portfolio adjustments to adapt to changing personal circumstances and different economic and investment environments. There is no substitute for proper planning, no panacea for not setting aside savings, and no windfalls for losing principal.

If you plan to avoid the four horsemen, have a plan, plan early, and start today. It is the first day of the rest of your life. Begin now!