Gone are the days where investors and savers alike can expect 5-6% real returns on US equities without taking excessive amounts of risk. In fact, many investors might agree that finding value in domestic equity markets has become increasingly difficult.

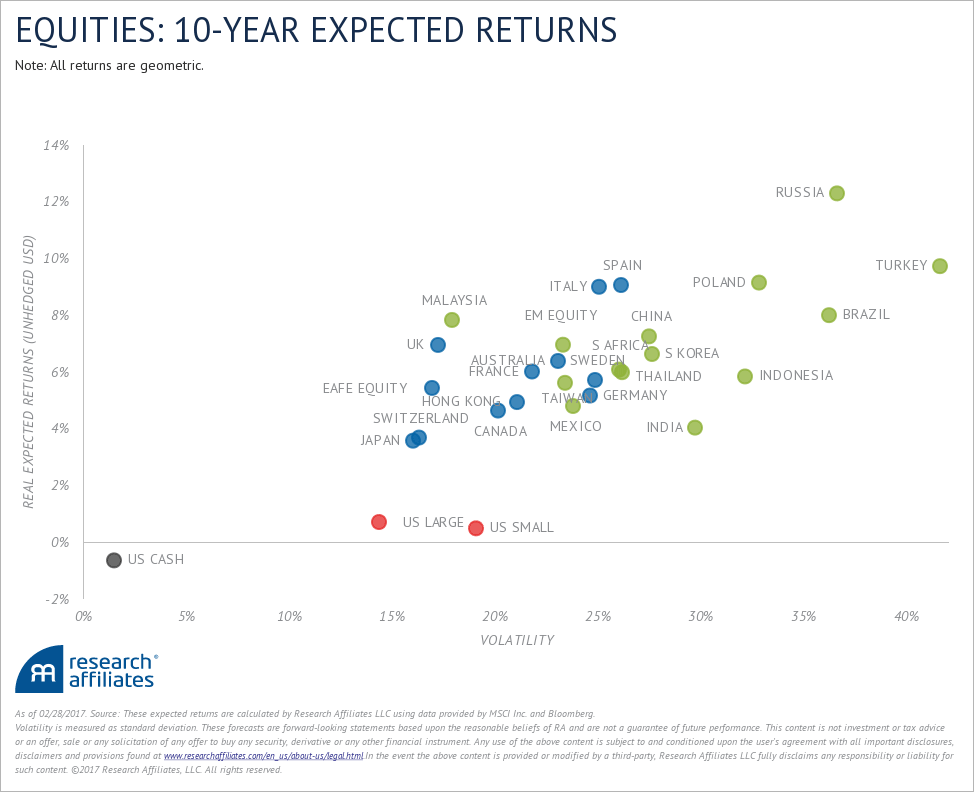

At current valuations, many institutions are lowering their expectations based on the current macroeconomic outlook and it doesn’t look that great for US stocks overall. Below is a chart compiled by Research Affiliates that graphs the next 10-year expected returns on global equities including US equities (in red), emerging markets (in green), and European and far eastern markets (in blue) based on real returns and forward-looking volatility.

This chart speaks volumes as to why investors need to rethink their expectations for higher returns over the next 7-10 years and why it may be important to consider searching for value elsewhere going forward.

In terms of why experts downgrading their outlook on US asset classes, here are the three main reasons...

Extreme Valuations

Future expected returns on US stocks will naturally continue to decrease as US equity markets climb higher, especially given the extreme levels they are at currently. Think of Sir Isaac Newton’s third law of motion that states that, “for every action, there is an equal and opposite reaction.” Noted market watcher Doug Short has a great chart that really provides a big picture view of where valuations are currently. In the case of extended asset prices, the probabilities of a significant reversion are growing higher as valuations push above their long-term mean.

Political Uncertainly

A lot could happen in 4 years with President Trump in the oval office. President Trump has a HUUGE agenda of overhauling the current tax system, building a border wall, and rebuilding America’s infrastructure (fiscal stimulus). The Administration’s failure to deliver on a campaign promise of repealing and replacing the Affordable Care Act is the reason why political uncertainty still remains an underlying component of low expected returns going forward. Very little is known about what role Trump will play in global trade or whether he will look for a more protectionist course of action.

The Fed Factor

A steady rising interest rate environment could be a catalyst for higher credit default rates and lower amounts of bank lending, especially if it results in a flattening or inverted yield curve. Nearing the end of an easy credit cycle means we could see more pressure on consumers and institutions with high debt burdens. This too could cap equity yields and contribute to low potential growth going forward.

In summary, stretched equity prices, political uncertainty, and a rising interest rate environment all remain catalysts for lower future returns over the next decade. As a result, putting your savings in a low-risk, high yield investment probably won’t come as easy as it did 10 or 20 years ago. That is why setting the bar at a reasonable level becomes all the more relevant now.