The primary US stock market yardstick, the SP 500 Index rallied 17% into March 1st from the spike low on election day. In almost 5 months of stellar gains, the market has yet to experience more than a 2% correction on a closing basis and 3% intraday. Until March our advice has been to avoid waiting for corrections and keep investing as too many sat on their hands assuming a better entry ~5% lower was due. While 5% is not scary, the growing pent-up demand prevented such an ideal pullback.

Now that we have entered a new political phase where market expectations require being fed a dose of “real” legislative success, we are in stall mode. The reality is setting in that the arduous hurdle of replacing Healthcare and Tax Reform will be delayed until late 2017 – at the earliest. No longer are we anxious to pay expected 2018 earnings today and Buy at any price. Throughout March we have been talking of consolidation. The chart below is essentially unchanged from previous iterations we have shown. This consolidation could last longer and correct further, but supportive economic data, deregulation orders and normalized household income growth provide support while Trump searches for legislative success to break out of the current incertitude.

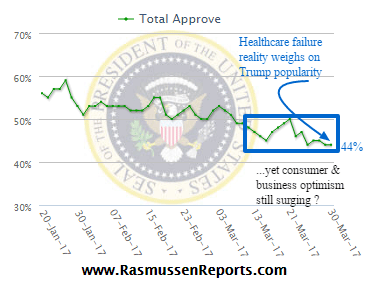

The failure (delay) in passing Trumpcare is not a surprise, but certainly, highlights the challenge of Trump’s wildly ambitious agenda. Our polarizing populist President is taking a further hit in the polls that have based most of their optimism upon the Making America Great mantra. Rasmussen was one of the accurate pollsters during the election and they show a clear downdraft the past couple of weeks as healthcare doubts rose. Trump would be prudent to pivot towards domestic infrastructure and overseas income repatriation legislation.

If Trump’s personal popularity were critical to investors and the economy then we would expect to see consumer and business surveys tanking along with stock prices. Just the opposite is occurring on all fronts. Businesses are extremely optimistic, consumers are about as excited as any period in history and our rocketing stock market has yet to allow more than a 3% correction since Trump was elected.

Is too much of a good thing bad? The concern is there may be an expiration date upon Making America Great Again. The soft data reflected in consumer and business expectations is exceptionally high, especially relative to the tepid sub 2% growth rate of our economy. At some point, legislative roadblocks by Democrats and alienated factions within the Republicans may cause a sharp reduction in the financial premiums that are being priced into earnings and the stock market. For now, we are in pause mode for March and likely April. While there are few political signs of optimism currently, the executive orders reducing regulations combined with natural conversion of optimism to new orders and new hires can still propel prices higher this summer. The “soft data” surge seen here is more indicative of an early stage expansion instead of one that is writing dirges for a maturing economy.

Image cannot be displayed

While Trump ignited a fire in US stocks, there is also a fire in stock markets throughout Europe and Britain which have mirrored our gains. Manufacturing data is robust in the US and even more so in Europe. There is more here than a simple wave of hope swirling around a boastful President. Any serious stock market correction of 10% or more would drive a nail through this current Bull move and squash optimism and economic acceleration for many months to come. That is not a scenario we expect. Barring exogenous events, we still expect soft data optimism to convert to hard data above trend growth later in 2017 and 2018.

Become a subscriber and gain full access to our premium weekday interviews with leading guest experts by clicking here.