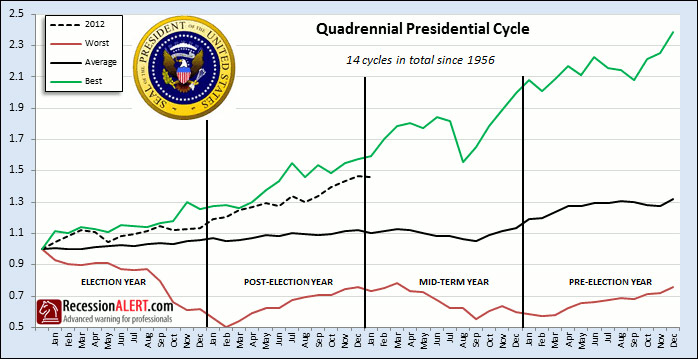

We have entered the Mid-Term cycle in the Quadrennial Presidential Cycle, in which the months April through to September typically represent the worst SP-500 seasonal period for the entire 4 year cycle. The current cycle which commenced in 2012 has performed way above average so far, as shown below with the black dotted line:

However it is plain to see from the chart above that the average gains through the 4-year cycle are composed of cycles that vary quite a bit around the mean. We also note that despite the hugely above-average performance so far in this cycle, we are by no means out of boundaries set in prior cycles.

Due to wide dispersion around the mean since 1956, we find it more illuminating to rather compare the current cycle with all prior cycles that are showing at least a 90% correlation with the current 2-year progress:

Again it is clear we are still running above average (no doubt due to the FED’s stimulus — see “FED in the driving Seat“), but are still very much in tune with the directional cues imparted by the average as shown by the r-squared correlation of 0.97. Regardless if one looks to this chart or the chart depicting all past cycles, the message is clear that we are entering a seasonally weak period through to September 2014.

If we examine all prior stretches running from April through to September in the mid-term election cycle, we get the following distribution of returns:

Whilst it is not impossible for out-sized gains to occur during this period, the odds are clearly stacked against you with the historical record providing a lowly 35% chance of success and losing points outweighing winning points by 2.56 times to one. There are obviously many factors to take into account when deciding what do do during this period of weakness, most importantly the status of the economy, stock market health metrics, your investment horizon and so forth but if you are purely making decisions on statistical odds of past performance then this is the time to be sitting out the market since risks are more than double any likely rewards.

As we showed with our SuperCycle Seasonal Methodology, bear markets and recessions have a surprisingly large seasonal factor surrounding them. If ever this market is going to correct 10-15% off current heady highs it is very likely to occur between now and September. We certainly hope it does follow the playbook, since the 4-6 months pain is more than rewarded with the mother of all rallies that usually commences in the latter part of the mid-term election cycle.