The world is awash in worries about deflation, but here in the US, it appears that inflation is making a comeback. If this new trend continues, it may catch a lot of investors off guard.

Inflation, or the lack thereof, drives financial markets with an unforeseen force. It has strong implications regarding everything from long-term interest rates to capital spending plans to Federal Reserve monetary policy.

Roughly four years, the Fed was able to hit its 2% inflation target. Since then, we’ve been over a prolonged period of disinflation, which the Federal Open Market Committee (FOMC) has been trying to overcome.

Read: OECD's William White: In Terms of Debt, the Situation Is Way Worse than 2007

When they raised rates last December, they did so on the premise that low levels of inflation were “transitory” and would dissipate as the declines in energy and import prices worked their way through the system.

So far it would appear the Fed’s thesis is playing out.

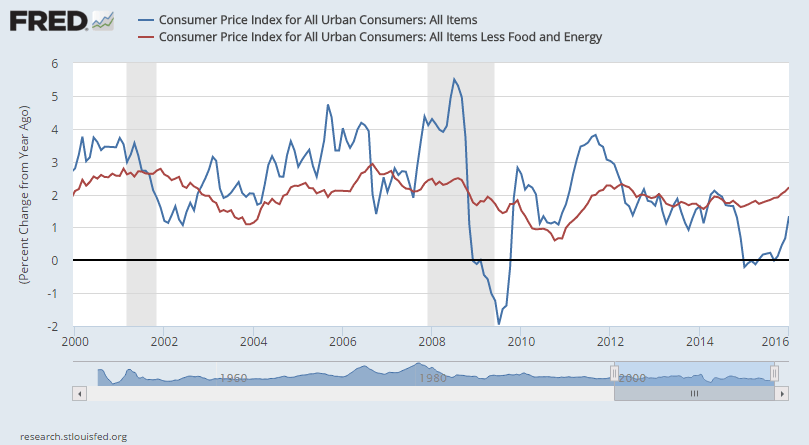

To begin, take a look at the chart below which shows overall headline inflation in blue, and core inflation (excluding food and energy) in red.

Notice that in mid-2014, corresponding to the dollar’s blast-off and the beginning of oil’s demise, overall inflation took a nose dive lower, nearly crossing the sharp 0% line (which would mark the transition into deflation). We can see that that the collapse in headline inflation pulled core inflation down with it, but to a much lesser extent.

Now, over the last few months, inflation has begun to rebound (black arrows). Many people find this phenomenon strange when they consider that oil is still trading close to its recent lows, near /barrel. “Doesn’t oil need to rise for inflation to pick up?” they ask.

The answer is no; it doesn’t. It just needs to stop going down.

The reason oil took such a toll on overall inflation is because oil itself was experiencing massive deflation. The price of oil, when compared to its price a year earlier, kept on falling and falling. But now, oil has been sharply suppressed for over a year, and this effect is diminishing.

Consider that at the beginning of 2015, WTIC was trading near /barrel. With current prices near /barrel, that decline is much more benign than the massive drops we saw earlier.

Listen to: Jim Puplava’s Big Picture: Oil – The Bottom, The Recovery, The Shock

The Fed knew that oil couldn’t keep falling forever, and once it stabilized, its deflationary effect would subside.

Before we get into the implications of rising inflation, I want to show you a few more charts to highlight the shift that we’re seeing.

Below is a chart of the Consumer Price Index. The headline rate (all items) is in blue, and the core CPI (excluding food and energy) is in red.

Notice the same pattern in which both headline and core inflation are trending higher. Also, note that core CPI has crossed the 2% threshold.

Next, let’s take a look at some of the inputs for inflation to get an idea of what’s in the pricing pipeline.

The chart below shows the Producer Price Index, (again both headline and core) and you can see the same rebound in prices on the right side of the chart.

Finally, here is a look at import prices, which are starting to stabilize as well. Import prices are still lower than a year ago, but the negative growth rate is abating. As falling import prices begin to level off, it will remove some of the downward pressure on overall price levels.

Now let’s talk about what this all means.

If inflation is on its way back, then we’re going to see movements in financial assets across the board.

First, keep in mind that the primary factor keeping the Fed from raising rates further has been the lack of inflation. As the one component of their dual mandate that is not currently being met, a return of inflation would give the Fed the ammo it needs to maintain an upward trajectory for the Federal Funds rate. Translation: rising inflation implies more rate hikes ahead.

Read: Will the US Go Negative in 2017?

Rising inflation will also cause fixed income investors to demand more yield on longer-term bonds. This means longer-term Treasury yields will rise, and prices will fall.

And if interest rates across the board rise, there is a good chance it will attract more capital to the US, bolstering the dollar’s current strength.

In closing, I’d like to show you one last chart. This next chart shows the market’s inflation expectations over the next 5 years. As you can see, the downtrend in inflation expectations remains intact. This suggests one of two possible scenarios.

Either the market has not caught on to the uptick in inflation, or they don’t believe it will persist.

There’s certainly an argument to be made that deflationary forces across the rest of globe will continue to exert pressure on the US However, the counterargument lies in the strength and resilience of the American consumer, who makes up the bulk of our economy.

Where prices will go from here is anyone’s guess, but at the moment, inflation appears to be knocking on the door.

The preceding content was an excerpt from Dow Theory Letters. To receive their daily updates and research, click here to subscribe.