So, apparently, according to Jon Hilsenrath, "QE to Infinity" is actually "finite" after all. With Ben Bernanke set to "exit stage left" in 2014 the question of who replaces him at the helm of the massive USS "Federal Reserve" will be important as to the future of the current course of monetary policy. One of the top contenders for that job is Janet Yellen. However, according to the variety of erudite speakers at the recent Strategic Investment Conference, there are many hurdles ahead for her and she may be just too "dovish" to actually land the job.

However, according to Hilsenrath, the Federal Reserve has already mapped out a strategy for winding down the unprecedented $85 billion monthly bond buying program meant to spur the economy.

"Officials say they plan to reduce the amount of bonds they buy in careful and potentially halting steps, varying their purchases as their confidence about the job market and inflation evolves. The timing on when to start is still being debated.

The Fed's strategy for how and when to wind down the program is of intense interest in financial markets. While the strategy being debated leaves the Fed plenty of flexibility, it might not be the clear and steady path markets expect based on past experience.

Officials are focusing on clarifying the strategy so markets don't overreact about their next moves. For example, officials want to avoid creating expectations that their retreat will be a steady, uniform process like their approach from 2003 to 2006, when they raised short-term interest rates in a series of quarter-percentage-point increments over 17 straight policy meetings."

The stock market has rallied sharply in direct correlation to the expansion of the Fed's balance sheet yet economic growth has floundered much to the dismay of the Federal Reserve. As I discussed recently:

"The increases in excess reserves, which the banks can borrow for effectively zero, have been funneled directly into risky assets in order to create returns. This is why there is such a high correlation, roughly 85%, between the increase in the Fed's balance sheet and the return of the stock market."

The question for investors becomes "What will be the sign posts that QE has come to an end?"

Fortunately, while the magnitude of the current monetary experiment is unprecedented, what happens when to the financial markets, and economy, when one of the program cycles ends - is not. When the first round of Large Scale Asset Purchase programs (LSAP), or more commonly referred to as "Quantitative Easing (QE)", was launched it was scheduled to end in June of 2010. Similarly, when the second program was launched in fall of 2010 it was similarly scheduled to end in the summer of 2011. In both cases there were finite start and end dates to the programs around which the financial markets could plan.

This is the key difference between the two earlier programs and the current QE program which has no definitive scope in size or end date but was, for the first time, targeted to specific economic variables of inflation and unemployment rates. This key difference leaves much room for speculation by Wall Street as to where the limits of the program actually lay as well as how far the Federal Reserve will push those limits.

However, there are some key areas that we can watch, as investors, that should tell us that the Fed has indeed embarked upon a process to wind down the current QE program.

Sign Post 1: The US Dollar

One of the areas directly influenced by QE programs is the U.S. dollar. Other countries store their excess reserves in the U.S. dollar when they feel that the U.S. economy strong, or at least stronger, than other countries. The inflows into the dollar for "safety" causes the U.S. dollar to rise relative to other currencies. This is why you have often heard the term that the "U.S. dollar is the cleanest - dirty shirt." While the U.S. economy is not strong on any measure - it is stronger than most other economies in general.

The chart below shows the impact of past QE programs on the dollar.

As you can see when QE programs have been in full swing that dollar has declined against other currencies as the "short US Dollar - long dollar denominated assets" carry trade was engaged. However, when these programs came to an end the dollar rose as "risk" was unwound. However, during QE 3 the dollar has risen as the Japanese Yen has been the target of the "carry trade" with Japan's QE program dwarfing, on a relative basis, the size of that in the U.S.

We will want to watch for a decline in the dollar as QE3 begins to slow down and the support against a very weak economic state is removed. Increases in economic weakness will act as a headwind against the rise of the dollar.

However, one scenario that could drive the dollar substantially higher in the near term is a failure of Abe-nomics in Japan. If Kyle Bass turns out to be correct, and their current monetary experiment fails, the flight of capital out of Japan into the U.S. for safety could lead to a sharp rise in the dollar. However, such an event will be bad economically for the U.S. as exports will become to expensive too quickly and will likely push the U.S. into a recession.

Sign Post 2: Gold & Commodities

Gold is not behaving under the current QE program as it has during the previous two. Gold spiked sharply during the two previous programs as the fears of hyperinflation and economic ruin fueled speculative gold buying. However, gold has plunged sharply during QE 3 as concerns of "deflation" have continued to show prevalence in recent economic reports.

However, it is likely that we could see gold rise in the months ahead if economic weakness continues to perforate the data. The chart below shows commodities during the same QE programs. Like gold, commodities rose as economies recovered. However, commodities are clearly signaling that deflation, and economic weakness, is ripping through the world economies and, without the monetary support from the Federal Reserve, the U.S. economy would likely be exhibiting far more weakness than it is currently.

Investors should be watching for a continued decline in commodities as economic erosion gains traction. However, as the underlying economic weakness surfaces the reversion of money flows out of the "risk-on equity trade" into "safety" will push gold higher.

Sign Post 3: Same For Bonds

The same goes for bonds. During QE programs interest rates have risen as the "risk" trade pushed money flows into stocks. However, the opposite occurred at the end of programs as money fled from stocks and into the perceived "safety" of bonds.

Despite calls for the end of the "bond bubble" the reality is that with the demographic shift in the country leading to a need for "yield" coupled with the Fed suppressing interest rates to historically low levels - the money flows will continue to push into bonds for the foreseeable future. This will particularly be the case when QE 3 ends and the inevitable reversion in stock prices occurs.

Interest rates have already been declining as economic data has weakened. However, the reversion of the "risk trade" into the "safety trade" will likely drive interest rates to our long term target of 1% or potentially lower.

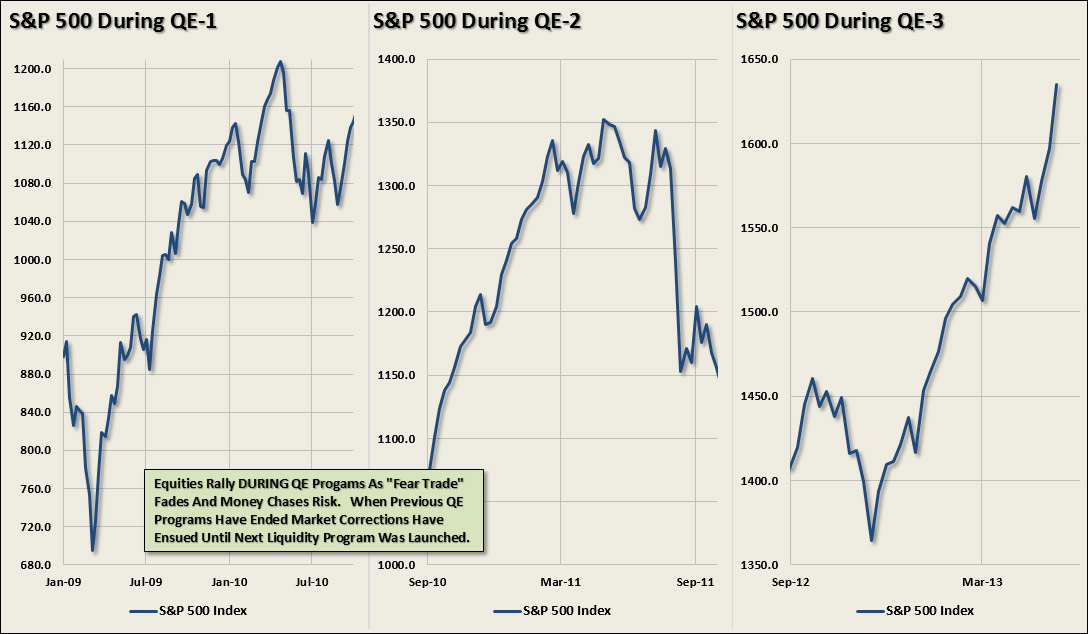

Sign Post 4: The Stock Market Reversion

When something is perceived that it cannot end, it will, and likely sooner than you think.

That is the way that it is with the stock market currently. The belief is that the current trajectory of stocks will continue indefinitely, however, that is subject to how much further that the Federal Reserve is willing to inflation their balance sheet. The reality is, as shown in the chart below, is that when the Federal Reserve begins to stabilize, and or reduce, their balance sheet it will be reflected in the stock market.

During each program there was a belief that the current trend would not be broken. Yet in each case the result was the same as the corrections in the markets, following the end of QE programs, have progressively become more severe.

The reason that each correction has gained more severity is due to the extension of prices relative to the underlying fundamentals. During the first two programs economic and market fundamentals were improving. That is no longer the case and the unwinding of QE 3 is likely to leave a rather large vacuum below current asset prices. Investors need to watch corrections in market prices for signals that the current bullish trend is being violated.

Sign Post 5: The VIX Will Lead The Way

The volatility index (VIX) has been muted ever since the Fed started hinting at QE 3 last summer. With the Fed "in play" market participants have "no fear" of taking on additional risk. It becomes an even bigger issue when the "lack of fear" is coupled with "leverage" as witnessed by the levels of margin debt now reaching levels seen at the peak of the markets in 2008.

What the chart above shows is that "WHEN" the eventual reversion in the stock market occurs the volatility index will begin to spike sharply higher. investors should watch the VIX closely as it will begin to push higher as the correction begins. When price supports are broken, and ultimately the bullish upward trend, the VIX will begin to spike sharply higher as stock prices fall. This will be your signal that it is time to leave the casino.

The Race For The Door

There is no doubt that the Federal Reserve will do everything in its power to try and "talk" the markets down and "signal" policy changes well in advance of actual action. However, that is unlikely to matter.

The problem with the financial markets today is the speed at which things occur. High frequency trading, algorithmic programs, program trading combined with market participant's "herd mentality" is not influenced by actions but rather by perception.

As stated above, with margin debt at historically high levels when the "herd" begins to turn it will not be a slow and methodical process but rather a stampede with little regard to valuation or fundamental measures. As prices decline it will trigger margin calls which will induce more indiscriminate selling. The vicious cycle will repeat until margin levels are cleared and selling is exhausted.

The reality is that the stock market is extremely vulnerable to a sharp correction. Currently, complacency is near record levels and no one sees a severe market retracement as a possibility. The common belief is that there is "no bubble" in assets and the Federal Reserve has everything under control.

Of course, that is what we heard at the peak of the markets in 2000 and 2008 just before the "race for the door" led to fingers being pointed, blame laid and calls for more regulation occurred. The outrage that follows market reversions is symbolic only of the willful blindness by investors caused by greed. Someday we will learn the simple truth that, despite our best efforts, market and economic cycles can only be momentarily manipulated and not repealed and the end result will always be the same. This time will be no different.

Source: Street Talk Live