Originally posted at Briefing.com

The start to 2017 has been almost as good as the start to 2016 was bad. It's an important distinction if only for the fact that "the turn" in the S&P 500 from its ugly start in 2016 started in mid-February when there were palpable concerns about how bad things looked for the stock market and the economy.

What a difference a year makes. Today there is an almost giddy sense of how good things look for the stock market and how good they could look for the economy.

You may also like Gary Shilling: US Holds Upper Hand in Trade Environment

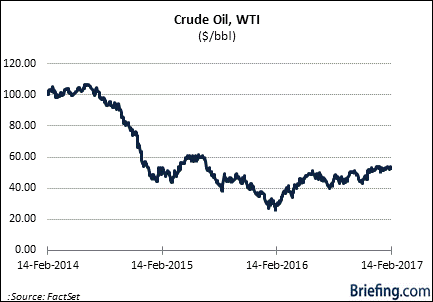

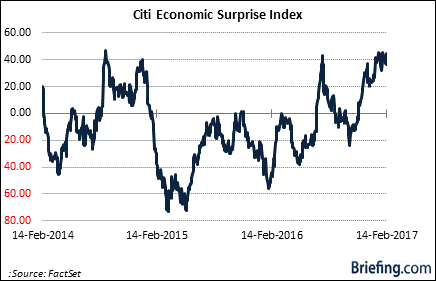

The major indices have all established new record highs, the cyclical sectors are leading the stock market higher, the financial sector occupies a leadership post, earnings are growing again, oil prices are up 80% from a year ago, and economic data is continually surprising on the upside.

The thinking among many market participants today is that the US economy is poised to achieve escape velocity, which is a far cry from the view a year ago when it was thought among many market participants that the US economy might slip into a recession and that falling oil and commodity prices might lead to a pernicious period of deflation.

At this juncture last year, many were wondering what could turn things around. Ironically, the same question is being contemplated today and it is one we'll explore here.

A Dimon in the Rough

Jamie Dimon, CEO of JPMorgan Chase (JPM), received a lot of credit for changing investor sentiment when it was disclosed on February 11, 2016, that he had bought $26 million of JPM stock. It just so happens that February 11 marked the low for the year for the S&P 500; hence, it is referred to as the "Dimon bottom."

Reassuring as that stock purchase was, it's a stretch to say that purchase alone made all of the difference. It didn't. There were multiple drivers, which started to gel at roughly the same time Mr. Dimon made his prescient (and very profitable) stock purchase.

- The Chinese stock market, which had been imploding, bottomed in late January

- Oil prices, which had been in a freefall, coincidentally hit their low for the year on February 11 (.21) and reversed dramatically from there on word of a potential output freeze agreement between OPEC and non-OPEC members

- Economic data started surprising on the upside against some depressed expectations, tempering the festering recession concerns

- The S&P 500 re-tested and held its April 2014 low; AND

- Central banks got more vocal about providing more policy accommodation if necessary

In reviewing the recovery effort in this column last March, we observed that "...recession fears faded away with the data and the market's deflation fears were dissolved by the spike in crude prices. The financial sector turned around and so did the cyclical sectors. Many growth/momentum stocks battled back and there was a massive wave of short-covering activity. The fear of being in the market was replaced by the fear of being out of the market."

The stock market would eventually suffer another notable setback in the latter half of 2016. It wasn't as pronounced as the one early in the year, yet the recovery effort from the latter setback was every bit as enthralling as the first one and it got going after Donald Trump was elected president and the GOP gained a majority in both houses of Congress.

A Force to Be Reckoned With

Some have taken to calling it the "Trump bottom," but once again, we'll aver that the stock market's rally to record highs in the wake of the election isn't only because of the pro-growth policies being discussed by the Trump Administration.

That has had a very large part to do with it in our estimation, yet it would be remiss not to mention that earnings had already started to grow again, oil prices were climbing to new heights, and the global economy was showing improvement ahead of the election.

Don't miss Michael Pettis: Most People, Including Trump, Don’t Understand How Global Trade Works

What the talk of tax reform, deregulation, and fiscal stimulus did, however, was energize a market that was already finding some reason to discount a better environment ahead, only it hadn't really dared to imagine before the election that could all come to pass, because very few people expected the election results to turn out as they did.

With a seeming mandate to cut tax rates, regulations, and introduce fiscal stimulus, market participants soon started sniffing out some strong growth possibilities for the economy and earnings, and the rush to get a piece of the stock market was on.

Animal spirits kicked in, pulling cash off the sidelines and pulling funds in from the Treasury market. Underinvested money managers were forced to play catch up, short sellers were forced to cover, and, if you'll pardon the expression, the force was with the stock market.

That's a very brief synopsis of why the map dot indicates we are here at record highs.

Spoilsports

What could turn this all around then? That answer, like the rally effort, is not one dimensional.

Multiple factors could spoil things and they are wrapped up in many of the same drivers that have pushed the major indices to record highs.

- A lack of corporate tax reform

- President Trump has indicated a "phenomenal" tax reform plan will be unveiled soon. The market has certainly liked the idea that such a plan is still at the forefront of the administration's policy initiatives, but will that reform plan measure up to the market's bullish expectations?

- What if it includes a border adjustment tax that drives up prices?

- What if it isn't revenue neutral and drives up the budget deficit, forcing more debt issuance that leads to higher interest rates?

- What if—and this is the big IF—it doesn't pass before the end of the year, dashing the economic and earnings growth expectations for 2017 that are tied up in premium valuations?

- President Trump has indicated a "phenomenal" tax reform plan will be unveiled soon. The market has certainly liked the idea that such a plan is still at the forefront of the administration's policy initiatives, but will that reform plan measure up to the market's bullish expectations?

- Protectionist trade chatter manifesting itself in actual trade protectionism

- What if the US imposes tariffs on Chinese goods?

- What if other countries balk at the Trump Administration's negotiating tactics and seek to establish new trade relationships with other partners (like China for instance)?

- What if the US dollar continues to strengthen and stiffens the resolve of President Trump to ensure other countries don't unduly benefit from their weaker currencies?

- Earnings growth disappoints

- Calendar 2017 earnings growth is expected to be 10.3%, according to FactSet, yet the market is tolerating rich valuations on the belief the earnings growth rate will be even higher thanks to a cut in the corporate tax rate.

- That will have to be rethought if the tax cut doesn't come in time or if it becomes apparent the earnings boost from the tax cut isn't as great as expected because the effective tax rate for many S&P 500 companies is already comfortably below the corporate tax rate.

- That will have to be rethought if the tax cut doesn't come in time or if it becomes apparent the earnings boost from the tax cut isn't as great as expected because the effective tax rate for many S&P 500 companies is already comfortably below the corporate tax rate.

- Calendar 2017 earnings growth is expected to be 10.3%, according to FactSet, yet the market is tolerating rich valuations on the belief the earnings growth rate will be even higher thanks to a cut in the corporate tax rate.

- Geopolitics gets messy

- There are always pockets of geopolitical discontent, but only an armed conflict—or the heightened threat of an armed conflict—ever really upsets the market for a spell. That threat is still under the market's radar, but it would have added capacity to upset the market if it came to pass since it would be viewed as a negative in its own right on one level and as a deterrent to implementing corporate tax reform sooner rather than later on another level

- North Korea, Iran, and the South China Sea stand out as geopolitical hot spots to watch, but the wild card is ever present

- North Korea, Iran, and the South China Sea stand out as geopolitical hot spots to watch, but the wild card is ever present

- There are always pockets of geopolitical discontent, but only an armed conflict—or the heightened threat of an armed conflict—ever really upsets the market for a spell. That threat is still under the market's radar, but it would have added capacity to upset the market if it came to pass since it would be viewed as a negative in its own right on one level and as a deterrent to implementing corporate tax reform sooner rather than later on another level

- The Federal Reserve takes away the punch bowl

- The FOMC has raised the target range for the fed funds rate only two times in the last 10 years (once in December 2015 and once in December 2016)

- The median projection among Fed members calls for three rate hikes in 2017, without accounting for any fiscal stimulus. If inflation picks up more than expected, with or without the benefit of fiscal stimulus, the FOMC could be forced to raise the target range for the fed funds rate faster than expected and more than expected

- Market rates should move higher in response, which would invite added valuation concerns and reduce the relative appeal of the equity asset class

- Market rates should move higher in response, which would invite added valuation concerns and reduce the relative appeal of the equity asset class

- Elections in the eurozone

- The Netherlands, France, and Germany all hold elections this year, but it is France's election that is being held out as the most pivotal one since it reportedly has the potential to upend the European Union (EU)

- Marine Le Pen is the leader of the far-right National Front Party and has said she would push for a referendum on the withdrawal of France from the EU if elected.

- France is the third largest economy in the EU behind Germany and the UK, and considering the UK has already voted to leave the EU, France's exit would be another major blow to the EU's integration efforts.

- Ms. Le Pen reportedly isn't favored to win, yet populism sells in politics these days, which means her potential to get elected, and the market upheaval it could invite, should not be underestimated.

- The Netherlands, France, and Germany all hold elections this year, but it is France's election that is being held out as the most pivotal one since it reportedly has the potential to upend the European Union (EU)

- Jamie Dimon sells stock

- This factor isn't a fundamental factor, yet we include it here because it could be an important factor for market sentiment. The major indices have hit record highs, but if the individual considered to have called the bottom with a major stock purchase at last year's low discloses that he is now selling stock with the indices at record highs, it could invite concerns about a potential top having been reached.

- Since more than a year has passed since Mr. Dimon's purchase, any stock sale now would be subject to the lower long-term capital gains tax rate, so there's a greater tax advantage for him in selling from this point forward than there would have been only a few weeks ago

What It All Means

Clearly, there are a lot of potential risk factors in the mix and a lot of "what if" scenarios. No one knows for certain what the future will bring.

There are spoilers in the mix. None have bubbled to the surface to any great extent, yet it seems naive to think that this bull run the market has been on since the election will persist without any challenges.

There are external challenges looming on the geopolitical front and there are internal challenges looming on the policy front.

With the market so focused on the domestic potential, though, it will be incumbent on the Trump Administration and the GOP to keep moving the line of scrimmage forward on tax reform and deregulation without getting caught offside on foreign policy matters.

One can tell by looking at the performance of the stock market that it has a pretty good sense of what could go right this year, although questions remain if it has any real appreciation for what could go wrong.

The answer is plenty, which means it is prudent to be hedged in the face of a roaring bull market—and probably because of it since everything seems so right.