Last fall we put together a presentation called Zero-Bound. It was our belief at the time that in the next recession the Fed would bring interest rates back down to zero. We were not in a recession, the economy was recovering globally, yet the Fed was slashing interest rates and expanding its balance sheet. We did not anticipate a global pandemic which led to a severe downturn in the economy as we are facing today. Despite trillions of dollars in monetary and fiscal stimulus, the unemployment rate is expected to remain above 10% this year with the economy contracting between 10-20%.

Many of the states are shutting down again, including my own state of California. Many states are also considering shutting down schools, which will make it difficult for two-parent working families. This is an election year and, as we've seen, many of the steps taken to contain the virus have been based more on political science instead of medical science. The only agreement in Washington is to spend more money. We expect and are predicting another massive stimulus bill to emerge by the end of July that will range between $1 trillion to as high as $3 trillion. This is an election year and politicians want to keep their jobs, including the President.

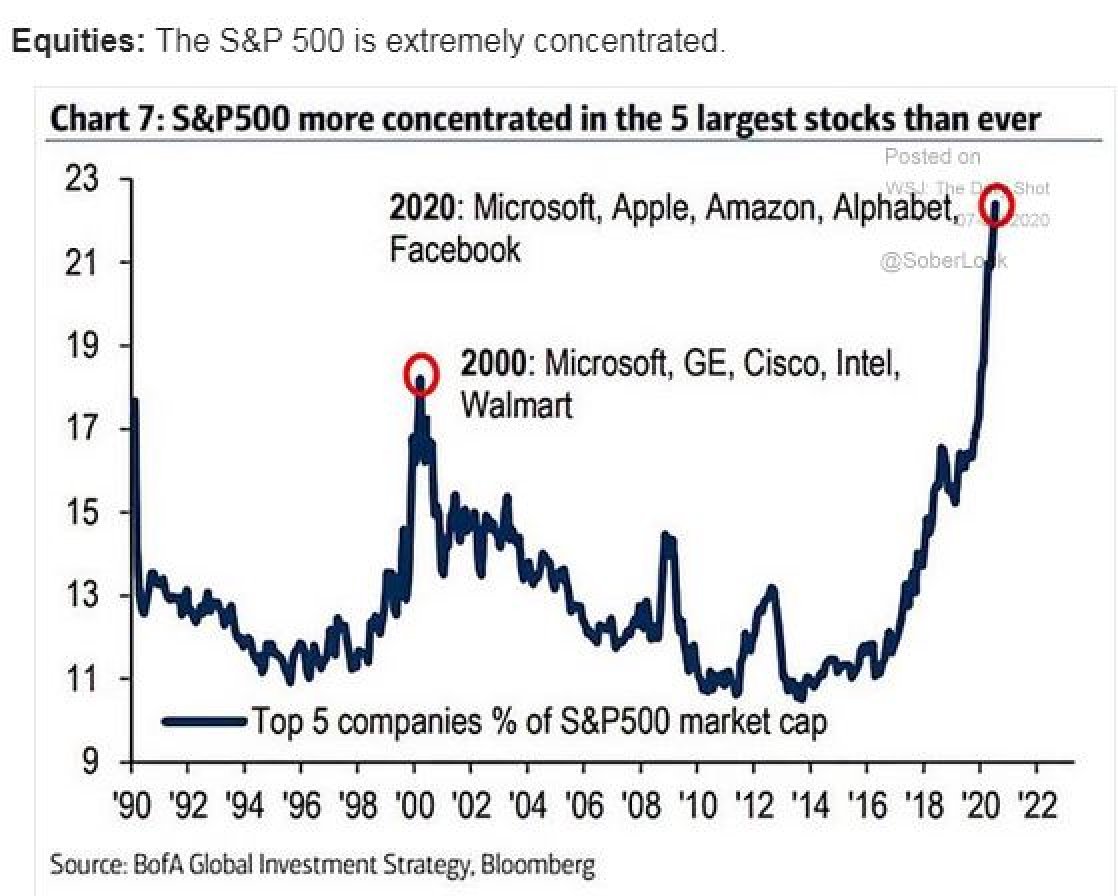

The financial markets seem to like the fiscal and monetary stimulus and have responded with a meteoric rise since the March lows. However, this rise is somewhat deceptive in the fact most of the market’s gains have been in the tech and healthcare sectors. The majority of stocks remain underwater, while the major indices like the Nasdaq and the S&P 500 are being driven by an increasingly smaller number of high-flying tech stocks.

However, as we discussed last fall, the recession has caused interest rates to drop to zero and we expect them to remain there for years to come in order to lower borrowing costs on an exploding national debt. The Fed is being forced to monetize most of the government’s debt as it expands its balance sheet to the tune of $1 trillion a month. Before this plays out, we actually expect interest rates to turn negative as they briefly did on T-bills in the early weeks of March.

The Fed’s massive bond-buying program is keeping interest rates capped and will prevent rates from rising as rising rates further exasperates the government’s budget deficit. The Fed is also intervening in the corporate bond market buying both investment grade (mainly BBB debt) and junk bonds driving down both of their yields. This is counter to most business cycles where, as the economy heads into recession, interest rates on corporate bonds rise to reflect increased credit risks or the risk of a debt downgrade. That was exactly what was happening in the months of February and March until the Fed announced it was going to be adding corporate bonds to its bond-buying program. The result is the bond market no longer offers attractive income opportunities as the yields on Treasuries and corporates no longer offer yields to compensate investors for the added risk of owning long-dated bonds, especially as we expect the return of inflation directly ahead of us. The CPI rose 0.6% in June as the return of consumers drove prices higher from food to gasoline. Listed below is a table of interest rates on Treasuries, foreign government bonds, and popular corporate bond ETFs.

As shown above, there isn’t much to find in the bond market that would justify locking up money for decades at a rate lower than the inflation rate, which we expect to start rising.

This is why we set up our income fund late last fall. The original idea behind the portfolio would be to invest 60% of the portfolio in dividend aristocrats (large cap, blue-chip stocks) with a history of raising dividends over a longer period of time. We would own 20 stocks with a 3% position in each company as well as hold stocks in different sectors for diversification. The rest of the portfolio would be 30% invested in bonds, and 10% in alternative asset classes such as gold.

Since its inception, we have had to change part of our allocation from bonds and replace them with preferred stocks paying dividends that range from 5.00-5.50%. The T-bills we held in the portfolio matured and it didn’t make financial sense to invest in Treasuries at yields of only 0.10%-0.60%. They were replaced with preferred stocks with yields ranging from 5-6%, and are taxed at a lower dividend tax rate of 10-15% for most of our clients. Corporate bonds make up the rest of the portfolio with a 10% allocation.

The results are that the program is working just as I expected. Of our 20 companies, 13 so far have increased their dividends this year despite an economic recession, with our gold stock increasing its dividend by 80%. We only had two stocks reduce their dividends—one has already been replaced and the other will be sold shortly and replaced with other dividend achievers. As a comparison, over 30% of the S&P 500 companies have decreased their dividends this year compared to only 10% of our Income Portfolio. One replacement has already increased its dividend this year by 6%. The two companies cutting their dividends were financials, casualties of the Fed’s low interest rate policy. Some of our healthcare holdings are working on a COVID vaccine, with one company that hopes to be producing 1 billion vaccines by the first quarter of next year if September trials go well.

I will also be reducing our bullion allocation to 5% and will be adding another dividend-paying gold producer. Gold companies are in a sweet spot as the price of gold is heading higher, costs are down on fuel and labor denominated in depreciating currencies.

The concept of this account was to provide a stream of increasing income at a time of zero interest rates and rising inflation. The objective was to achieve a yield that was twice the yield of the S&P 500 and 4-6 times higher than Treasuries. The current yield on the portfolio is close to 4%, and I see that yield rising with dividend increases as well as a few adjustments already mentioned.

At this point in time, the portfolio is doing what it was intended to do which is to provide an increasing source of income that is twice that of the market and much higher than the bond market in a tax-efficient manner with low turnover. Stock dividends are taxed at a rate of 0%-20%.

I anticipate this will become increasingly important in the years ahead as the Fed pursues a policy of financial repression in order to keep interest rates at zero coupled with the combination of massive fiscal deficits and monetary printing leading us down the path to higher inflation—a reason we own stocks, natural resources, and gold.

To find out more about Financial Sense® Wealth Management or for a complimentary risk assessment of your portfolio, click here to contact us.

Advisory services offered through Financial Sense® Advisors, Inc., a registered investment adviser. Securities offered through Financial Sense® Securities, Inc., Member FINRA/SIPC. DBA Financial Sense® Wealth Management.

Copyright © 2020 Jim Puplava