As America debates its debt, its debt ceiling, and the indebtedness of future generations, let’s make sure we all understand what we are talking about. Also, let’s look at an example of how the debt permeates through our society.

Why does the US have debt?

Because the stewards of the country’s Treasury, Congress, spends more than it takes in in tax receipts.

What is the debt?

The US issues bonds, notes, and bills that promise to pay principal and interest at maturity of the issue. The principal is meaningless. A printing machine produces principal to infinity. The interest, on the other hand, is a problem. Almost all of the current debt will have to be rolled over (re-financed) before 2020 at interest rates that prevail at the time of re-issue.

How much is the debt?

Let’s refer to the following website: https://www.treasurydirect.gov/govt/reports/pd/mspd/2011/opds062011.pdf. As of June, 2011, the official amount of Treasury debt issued is $14,343,088,000,000. In case we have trouble with all those commas, that figure represents ‘trillions’ of dollars in debt.

How much interest expense does the country pay each year on the debt?

In 2011, the US will pay $385.8 billion in interest coupons. That’s down from $413.9 billion paid in 2010 because interest rates have been falling while debt has been rising. In the end, it is not the debt that crushes a nation but rather the interest coupon required to facilitate a growing debt. We now live in a completely artificial environment whereby the Federal Reserve works to orchestrate a contracting interest coupon so the debt can be perpetuated. Banks make money by lending. The Fed made $90 billion in 2010. That’s more than Exxon and Walmart combined! We can all see who really benefits from massive debt. One can read my article ‘Why US Treasuries Will Eventually Yield Nothing’ to learn more as to why interest coupons will continue to fall.

Who owns the debt?

Here’s where it gets interesting. From the same website as previously referenced, the public owns $9,742,223,000,000 and roughly two-thirds of that is in the form of notes or intermediate term maturities. Another $4,600,864,000,000 in Treasury debt is listed as ‘Intragovernmental Holdings’. Nearly all of that $4.6 trillion is Treasury debt known as ‘Government Account Series’ (GAS) issue.

What’ the difference?

$4,580,584,000,000 of the $4,600,864,000,000 GAS debt is non-marketable. That means there is no market in which to sell this debt. In other words, if Treasuries should begin a bearish trend and sell off, investors that hold marketable Treasuries could sell their holdings to limit their losses. Holders of non-marketable Treasuries cannot.

Who holds non-marketable Treasury debt?

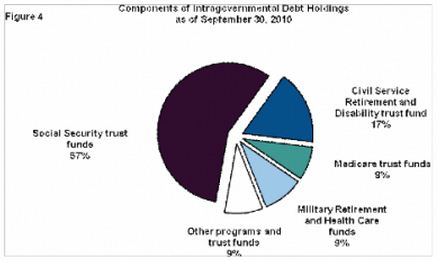

Interestingly enough, US citizens do. The Social Security Trust Fund holds 57% of the non-marketable Treasuries. Federal government employees are tied to the non-marketable debt through their retirement plan with a 17% ownership. Take a look at the following chart.

Source: https://www.treasurydirect.gov/govt/reports/pd/feddebt/feddebt_ann2010.pdf, pg. 15

Explain how federal employees are affected?

Civilian federal employees hired before 1984 were covered by the Civil Service Retirement System (CSRS) and those hired after 1984 were covered by the Federal Employees Retirement System (FERS). Both plans had investible assets directed to the Civil Service Retirement and Disability Fund (CSRDF). This is a defined benefits retirement fund for retired Federal employees. This retirement benefit extended by the taxpayer is structured as an annuity. Like everything for our government employees, a defined benefit plan is the ‘Cadillac’ of retirement plans. According to the Office of Personnel Management (OPM), they estimate the cost of the FERS annuity to be 12.5% of employee pay. The federal employee pays .8% and you and I pay the other 11.7% of that contribution. The federal government makes supplemental payments into the CSRDF on behalf of employees covered by the CSRS because employee and agency contributions and interest earnings do not meet the full cost of the benefits earned by employees covered by that system. But, it is an annuity and it is totally controlled by the government. The government controls the payout. The government controls the allocation of the invested funds. And, the government controls the ownership of the funds. That means the employees have no rights to the money listed in the plan under their name.

What is in the CSRDF?

As the retirement fund of civilian Federal employees, the funds are 100% invested in special-issue Treasury securities that count against the national debt. Contributions to the fund can be, and are suspended when a debt ceiling prohibits further expansion of the national debt. Current investments in the fund are redeemed by the Treasury while contributions are suspended. If and when further governmental borrowing is allowed, by law, the fund is then made whole again.

How much money is in the CSRDF?

According to an article authored by Katelin Isaacs at https://www2.pennyhill.com/?p=14318, the CSRDF reported a balance of $734 billion at the beginning of 2009. Here’a the part that I like. As with everything in our world today, the CSRDF is unfunded to the tune of $674 billion. It turns out that the CSRS was never funded while the newer and less generous FERS was and is funded. What we have is a dollar figure based on ‘imaginary value’ derived from Treasury note par value.

How is the CSRDF funded?

According to the OMB, the fund will have an income of $98 billion (estimate) in 2010. A full $3 billion will come from employee contributions. The other $95 billion will come from interest ($40 billion) and well, essentially tax payers. Expenses, or payouts, are expected to be around $70 billion for the same year. Again, all investments are required to be in US Treasuries. Still, the fund has a lot of ground to make up.

What if the US Treasury debt is capped or sells off?

We can see that civilian Federal employees and retirees could be hurt severely. If the debt can’t be expanded. the CSRDF will not get funding and retirement obligations will not be met. Should the Treasury notes and bills experience a loss in value due to selling pressure, the CSRDF will likely lose value and find itself more unfunded than originally thought. Even at best, the current Treasury Secretary has borrowed from the existing holdings of the fund to apply to the national debt to make it seem less threatening. Outright default on held Treasuries would surely diminish the value of the fund.

How does the US government get away with this type of accounting?

I really like this part. What you are about to read explains our world and our fiscal predicament perfectly. Please read this next sentence very carefully. Quoting from the source listed below, ‘According to the U.S. Office of Management and Budget (OMB), balances in the trust fund are... available for future benefit payments and other trust fund expenditures, but only in a bookkeeping sense.’ That statement ought to engender confidence in the government.

(Source: https://www.narfepad6.org/media//DIR_11701/c425b8c8d4041659ffff8b7effffe...)

But what about the part that is unfunded?

From the same source listed above, the fund is in no danger of insolvency because the unfunded gap will eventually close. Want to know how? This article that I am quoting from is from the Congressional Research Service written by Patrick Purcell in June of 2009. It says, ‘The decline in the ratio of CSRDF outlays to salary expense after 2020 will occur mainly because future retirees will receive smaller pension benefits under FERS than they would have received under CSRS.’ Does that sound like austerity? I suppose too, that actuaries could estimate rising taxes, rising interest rates, rising numbers of contributors (more government hires), and declining benefit recipients due to death. Or maybe, they are just dreaming!

What about Social Security?

Yep, the Social Security Trust Fund is required to own US Treasuries and as previously pointed out, the fund owns 57% of the non-marketable Treasury inventory. As with the CSRDF, if US Treasuries fail (default), so too will the Social Security Trust Fund. Also, as with civilian Federal employees and their retirement funds held by the CSRDF, a 1960 Supreme Court ruling established that contributors to Social Security do not have a right or an entitlement to receive benefits from the Social Security Trust Fund. The government can cut either off whenever it wants. The debt debate should be bringing the phony pension accounting to light in both Social Security and the CSRDF. Sadly, both now depend on ever expanding debt.

Conclusion

Hopefully this little article will help with the understanding of the US debt and some of the ramifications of current, and probably ongoing debt debate. As we can see, our modern world is tentacled with pervasive debt. Putting a limit on that debt is not as easy as it might sound. Letting the debt continuously expand is clearly an exercise of surrender at the vault of the elite banks. Yes, Treasuries held in trust funds and pensions are valued at par. But if the Treasury is not allowed to borrow more money to pay the interest on currently issued Treasuries, default will occur rendering the paper worthless. On the other hand, if the Treasury is allowed to expand the debt unimpeded, the increased supply will erode the value of currently issued debt either through inflation or supply/demand dynamics. The government is now exposed as an irresponsible fiduciary as it requires certain retirement programs to hold only one security - the one that it issues. The US Treasury note might turn out to be one of the most risky securities on the market. To make matters even worse, the reported balances in some retirement programs like the CSRDF are only balances in a ‘bookkeeping sense’. Maybe we are playing musical chairs only all the chairs are make believe. Maybe what we should really take from the debt debate is the illusion of fiscal soundness. In other words, we are in an ocean of debt that threatens to drown us but fortunately we have a boat. However, the boat only exists in our minds through the power of imagination. The boat is not real. We just can’t afford to open our eyes and see that the boat is not real because the ocean will consume us.

Disclaimer: The views discussed in this article are solely the opinion of the writer and have been presented for educational purposes. They are not meant to serve as individual investment advice and should not be taken as such. This is not a solicitation to buy or sell anything. Readers should consult their registered financial representative to determine the suitability of any investment strategies undertaken or implemented. BMF Investments, Inc. assumes no liability nor credit for any actions taken based on this article. Advisory services offered through BMF Investments, Inc.