With the market’s decline over the past week our longer term survey (200 day moving average evaluation) worsened with the long term trend of the market close to being downgraded another notch from neutral-bullish to neutral-bearish. Our more sensitive MATA survey fell meaningful from the prior week which downgraded the intermediate market outlook from neutral-bearish to outright bearish. Unless the market stabilizes soon we are likely to see the long term trend (200d survey) downgraded another level to neutral-bearish.

* Note: For further explanation of the market surveys and background on analysis, please click here.

200 Day Moving Average Evaluation

As shown in the table below, the net percentage of stocks that are in long term uptrends decreased from the prior week from 59% to 52% while the percentage of stocks in downtrends increased from 41% to 48%. The decline to 52% puts the market’s long term trend in jeopardy of being downgraded another level if it falls below 50%. In terms of sectors, the utilitiy sector takes the top spot as the percentage of its members in uptrends increase held steady at 72% while the consumer staples sector takes the second spot with its 66% reading. The absolute worst sector is energy with 84% of its members in long term bearish trends. Given energy represents 11.3% of the S&P 500, its weakness is weighing on the S&P 500 and offsetting some of the improvement in health care and consumer staples.

Classifying the four categories for the survey in terms of seasons helps to gauge the market’s maturity. This bull market remains to be dominated by the early bull market (AF, Spring) and late bull market (AR, Summer) categories, indicating the age of this bull market remains young as late bull markets have the AR categories dominating with more stocks also residing in the early bear market (BR, Fall) category.

The biggest shift we have seen in the categories over the last month is that many of the stocks in the S&P 500 that were marginally above their falling 200 day moving averages (200d MA) fell below them with the selloff over the last week to move from the AF (Above Falling) to the BF (Below Falling) category as the AF category nearly dropped in half from 11.2% to 1.0% over the last week. We have also seen stocks mature in their trends as a percentage of stocks in the AF category moved into the AR category (mainly non-cyclicals like health care, consumer staples, and utilities) while stocks that were in defined uptrends (AR) topped out and moved into early downtrends (BR). The early downtrend category (BR) saw the biggest increase over the prior week as many stocks have topped out with the market’s recent weakness.

While the bull market’s long term trend has been cut from bullish to neutral-bullish and in jeopardy of being downgraded even further, when looking at sector performance year-to-date, there is still some support for the bulls that the market is simply having a nasty intermediate term pullback rather than having put in a bull market top, particularly if the S&P 500 can stabilize above its 200 day moving average.

The sectors most leveraged to the economy that outperform when the economy is expanding are leading the market this year. The consumer discretionary, technology, and financial sectors are all up nearly twice the performance of the S&P 500. Conversely, the non-cyclical sectors that do best in a weak to decelerating economy are underperforming the S&P 500 (except for health care). If we are witnessing a market putting in a top we should see the non-cyclical sectors significantly outperform the cyclical sectors leading into a top and not after one which was never the case heading into the April 2012 peak.

Source: Bloomberg

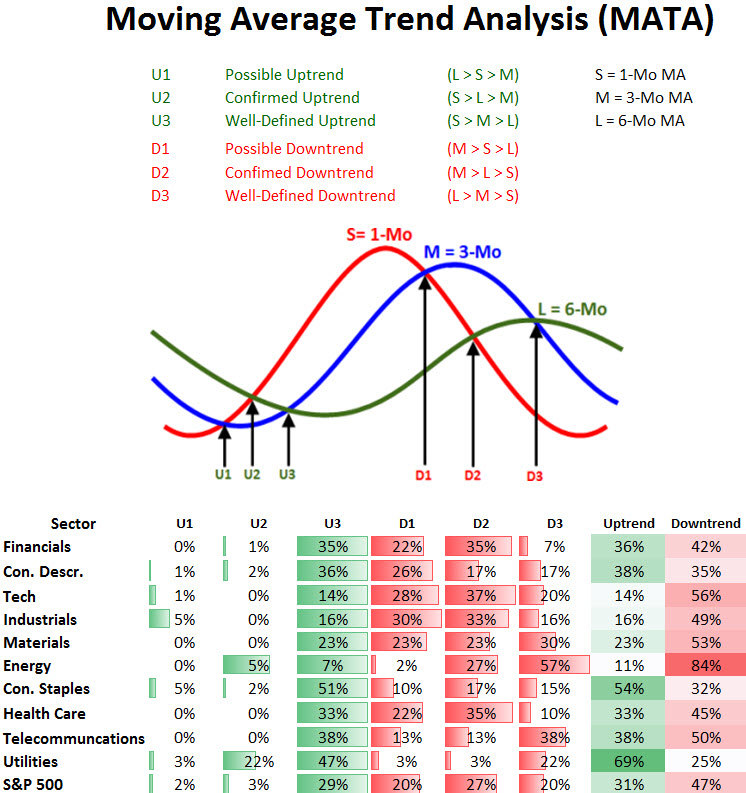

Moving Average Trend Analysis (MATA)

We saw a further worsening in the MATA survey for the S&P 500 in which the percentage of stocks in uptrends decreased from 42% to 31%. We saw an increase in the percentage of stocks in intermediate downtrends from 37% to 47% from last week’s reading as many stocks that were trying to rally and who were trendless saw their declines resume as they moved to bearish categories.

At a reading of 31% the intermediate trend for the market was downgraded one level from neural-bearish to outright bearish as less than a third of the market is in a well-defined intermediate uptrend.

52-Week Highs and Lows Data

The data for the S&P 500 for 52-week highs and lows shows a confused market. Over the past month 24% of the S&P 500 hit a 52-week high while only 5% hit new 52-week lows. What makes the backdrop in this survey a bit confusing is that one of the more cyclical sectors, consumer discretionary, has the strongest breadth with 38% of its members making a 52-week high over the last month. At the same time, of the 4 sectors with more new 52-week highs than the S&P 500, three are defensive non-cyclicals which gives a bearish tone to the market’s breadth.

That said, most of the sectors within the S&P 500 show new 52-week highs above new 52-week lows except for the energy sector which remains a technical mess. The technology sector has been weakening considerably over the last few weeks and it has seen its percent of new 52-week lows over the preceding month rise from 3% to 6% in the last week.

Source: Bloomberg

Summary

Given the above, the message provided in the surveys is an intermediate-term correction that has gone on now for 36 days and has significantly weakened the longer-term trend which is at risk of being downgraded to neutral-bearish the 200d MA survey weakened from 59% to 52%. On the bullish side of the ledger, this intermediate correction is running out of time as most intermediate-term moves end between 20-30 days and we can expect some type of oversold rally to occur to alleviate the market’s oversold condition. So far the S&P 500 is holding above its 200 day moving average which is bullish, though a definitive close below it would really begin to set off the bear market alarm bells.