Overview:

- The long predicted top in the USD is finally in

- Catalyst is a bottoming in global growth which is likely to have widespread investment implications

- Foreign currencies, commodities likely beneficiaries while the bond market will be greatest casualty

The two biggest topics I wrote about in the first quarter of the year was to expect a correction in the USD and a trough in global economic growth this spring, both of which are occurring right now. The three main points for why I argued a significant bottom in the global economy was due this spring in my prior article (click for link) are summarized below:

- Falling oil prices should lead to positive economic surprises in coming months

- Reflationary global central bank response is building to help global growth in 2nd half of 2015

- Relative performance of early to late cyclicals already discounting global economic trough

My case for expecting a USD correction highlighted in an earlier article (click for link) are outlined below:

- Extreme bullish sentiment towards the USD

- Mean reversion – USD move is stretched by several metrics

- A global economic recovery would turn optimism away from USD and towards foreign markets/currencies

- USD at long-term technical resistance

Updating some of my charts I looked at in the early articles shows that we should look past the weak Q1 GDP report that showed U.S. growth slowed to 0.25% during the quarter led by sharp declines in net exports (-1.25% hit to growth) and fixed nonresidential investment (-0.44% hit to growth led be declining in mining equipment from falling oil prices) and expect better growth prospects ahead. The relative performance of early to late-stage cyclicals argues that manufacturing activity in the U.S. as measured by the ISM Purchasing Manager’s Index (PMI) should bottom right here and begin to advance into the fall.

Source: Bloomberg

We are seeing the same development in europe in which the relative performance of early to late-stage cyclicals are calling for continued acceleration in european growth heading into the fall. The Markit eurozone PMI has already bottomed and recouped half of the decline seen during 2014.

Source: Bloomberg

Given two of the world’s largest economic regions are expected to show growth heading into the back half of the year it’s not surprising that global early- to late-stage cyclicals are also signaling global growth should accelerate ahead when looking at the OECD leading economic indicator where the OECD accounts for 63% of world GDP and 75% of world trade.

Source: Bloomberg

The Bloomberg consensus estimate shows estimates for 2015 economic growth bottomed in February and began to improve meaningfully in March close to 3%. Alongside the improved outlook for 2015 world GPD growth has been a bottom in commodities like oil prices (red line below) and copper prices (blue line below).

Source: Bloomberg

Concurrent with an improved global outlook, the USD appears to have also changed trend. It is not coincidence that the peak in the trade weighted USD Index coincided with the bottom in global growth as shown below (note that the USD is inverted for directional similarity).

Source: Bloomberg

Looking at global GDP estimates for 2015 suggests the bottom is in and as shown above global early- to late-stage cyclicals suggests global growth should improve heading into the latter half of 2015. Given USD strength is inversely correlated to global growth we should see the pace of appreciation in the USD slow for the balance of 2015. This is shown below in which the year-over-year (YOY) rate of change in the trade weighted USD is shown inverted relative to global early to late cyclical relative performance. What could affect the relationship below is the elephant in the room, which is a US Fed bent on raising rates. However, if it does so in the face of a growing global economy, the strength in the USD should be muted.

Source: Bloomberg

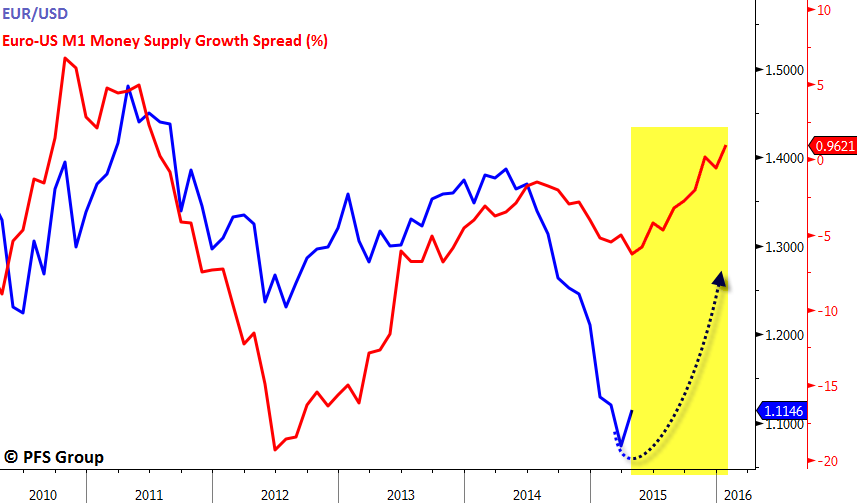

What is also likely to cap the appreciation of the USD this year is an economic recovery in the eurozone. Several relationships I track suggest that european growth should outperform US growth, which in turn should lead to the euro recouping some of its lost ground to the USD. One relationship is the spread between monetary growth rates in both regions and when money supply is growing faster in europe than in the US we tend to see the euro advance relative to the USD.

Source: Bloomberg

The strength in the euro over the USD is due to the leading tendency for money supply growth rates to lead economic growth rates. Thus, if the spread between euro and US money supply growth increases, then we are likely to see the spread between European and US GDP increase as well which is why the euro should strengthen or at least stabilize to the USD in the months ahead. Given we are in unprecedented times in which the ECB will be printing over a trillion euros heading into 2016, while the relationships above and below argue the euro should advance relative to the USD we may simply see the euro stop depreciating.

Source: Bloomberg

Another trend we are likely to see in the coming weeks and months is that a bottom in global growth will arrest the deflationary trend of falling inflation rates and falling interest rates that we’ve seen over the last several years. The pickup in global growth predicted by the relative performance of early- to late-stage cyclicals argues that long-term interest rates should move higher as shown below where both US and German long-term yields should be heading higher for much of the rest of the year. As long as the rise in interest rates is orderly we could see global capital move out of the bond market and help lift equity markets higher.

Source: Bloomberg

Summary:

The big story of the first quarter was one of falling global economic growth and strength in the USD. Those trends are now likely to reverse. While the USD may not experience a significant correction we should expect a consolidation at least and several trends will be developing that could cap the USD’s advance in the months ahead.

We’ve seen that the dollar tends to move inversely to global growth and a pickup in global growth should lead to a softening of its appreciation while foreign currencies recover from their declines over the last six months. Another added beneficiary from a weaker dollar will be commodities and commodity-producing sectors like energy and basic materials. We are also likely to see inflation expectations rise and with it a pickup in global bond yields.

In short, we are currently at a major inflection point in the year in which the trends that have been in place for the last year are likely to reverse.