The script of the last two years continues to play out as we move further into the fourth quarter. The highly volatile script over the last two years is strength in the beginning of the year followed by a harsh middle third and then a recovery into the latter third of the year. The economy and markets bottomed this summer and continue to show improvement despite the recession call by the Economic Cycle Research Institute (ECRI). As is shown below, the economy continues to improve from this summer’s drubbing which is being confirmed by the credit markets as financial stress continues to subside.

Economy Improving

There are simply way too many bears out there, both of the economic and stock market variety. One way to visualize this is to look at economist estimates for various data series and then compare with the real numbers. For example, today we received the University of Michigan’s Consumer Confidence report for October with the average estimate from 71 different economists coming in at 77.9 while the actual reading was off the charts, coming in at 83.1. Out of those 71 economists, not a single one of them even came close to the actual number as the most optimistic estimate called for a reading of 81. Clearly economists are behind the economic curve as the economy continues to improve.

Source: Bloomberg

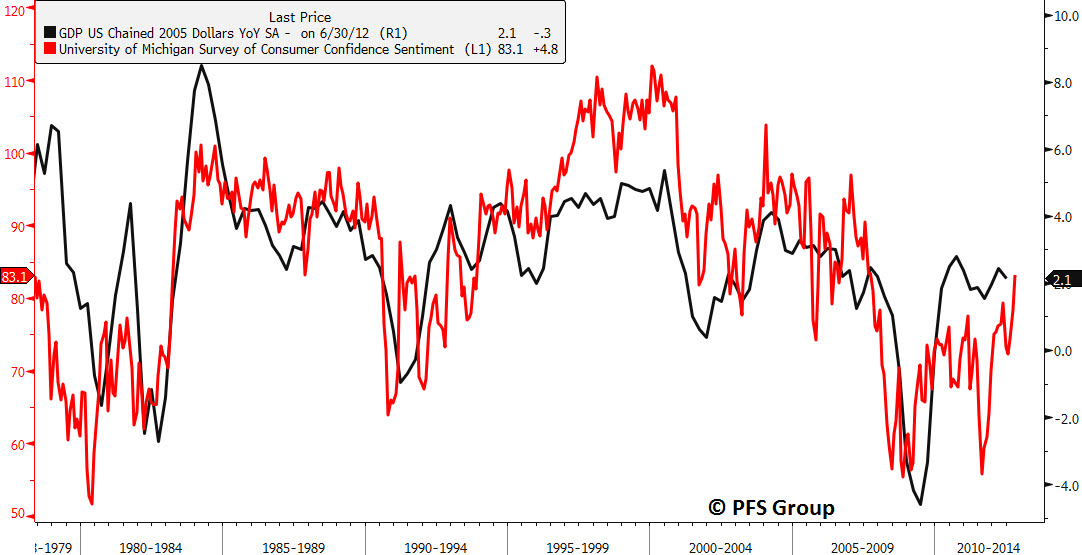

Consumer confidence is a key driver of the U.S. economy as consumers spend more as their confidence improves, and more spending leads to higher growth rates. The linkage is shown below between the Michigan Consumer Sentiment Survey and real GDP. The recent jump in confidence suggests that real GDP may accelerate heading into the end of the year.

Source: Bloomberg

Recession Warnings Remain Absent

With an economy on the mend recessionary risk diminishes, which is going against the ECRI’s recession call. What is interesting to me is the ECRI’s insistence of sticking with their recession call in the face of improving data. Even their own economic leading indicators (WLI) are improving and have moved from contraction to expansion territory. One argument of the ECRI is that economic growth rates continue to fall each year as the recovery since the recession ended in 2009 begins to weaken and fade. However, the U.S. economy appears to be doing the complete opposite as the ECRI’s WLI growth rate jumped this week to a reading of +5.7%, which exceeded the peak set earlier in the year before the summer swoon. Moreover, while the WLI fell this summer it bottomed at a higher level than either the 2010 or 2011 summer decline. Any good technician knows that a higher low and a higher high is the definition of a bullish trend and that is exactly what we have in the ECRI WLI, a similar setup that occurred in the middle of 2009 as the economy’s growth rate accelerated and stopped the economic slide that began in 2007. How the ECRI can stand behind their recession call currently is beyond me as even their own data refutes their position.

Source: Bloomberg

Aside from the ECRI WLI, other economic data is void of recessionary warnings. The five month moving average of the Conference Board’s Coincident Diffusion Index rests at 95% as of the end of August and given leading economic indicators are turning up it’s highly unlikely that we will fall below the critical 60% mark shown below that often heralds a recession.

Source: Bloomberg

Jobless claims data just hit a post-recession low this week as they came in at 339,000 which is the lowest reading since February 2008. To begin to worry about a coming recession we need to see the annual rate of jobless claims rise more than 15% from its year-ago levels and the fact that jobless claims are FALLING makes it highly unlikely we will see a 15% annual growth rate any time soon.

Source: Bloomberg

Credit Markets in Agreement with Economy & Stock Market

We are also seeing an improvement in the credit markets as financial stress moderates. Shown below is the Bloomberg Financial Conditions Index for the U.S. (top) and Europe (bottom) along with their respective stock markets. Looking at both economic regions shows financial stress has improved to its highest levels in two years as fears of a European contagion slowly fade.

Source: Bloomberg

Money market spreads are near the lowest levels since the recovery began and indicate the stress from the 2011-2012 European scare have been fully alleviated.

Source: Bloomberg

Euro and USD swap spreads are at their lowest levels since the recovery began while others like the Ted Spread and LIBOR-OIS spread continue to improve from lofty levels seen earlier in the year.

Source: Bloomberg

Summary

We have an improving economy and stock market that nobody wants to believe in. Economists are too pessimistic and investors and portfolio managers are largely on the sidelines. From a contrarian point-of-view, this provides a bullish setup in the market in stark contrast to the 2000 and 2007 tops when the skies were the limit and sentiment was overly optimistic. While 2013 will certainly have its challenges and the fiscal cliff looms large, keeping emotions in check and sticking with the facts on the ground will be crucial to help investors remain objective.