One of the concerns of late is the weakness in commodities and what that portends in terms of global growth going forward. Many argue that the slide in commodity prices is discounting a collapse in global growth in the near future. While it is true that global growth has been very anemic recently, with RecessionAlert.com making the call that we are in the second global recession since the 2008 Great Recession (click for link), I believe recent commodity declines are actually setting the stage for a improved second half (2H) for 2013.

Europe has been particularly weak over the last six months which has weighed on US exports to the region and corporate earnings derived from Europe. That may soon be changing as the recent slide in commodities will give corporations and consumers alike a tailwind along with past monetary stimulus set to kick in during the second half of the year.

Shown below is the annual growth in European GDP (black line) along with several indicators that lead European GDP. Growth in M1 money supply (green line) shown advanced below argues that the delayed action of monetary policy should lead to a surge in European GDP growth rates through the remainder of 2013. Likewise, Bloomberg’s European Financial Conditions Index (red line below) is mimicking the message of M1 money supply growth rates and suggests a pickup in European GDP should be expected. Foreshadowing an improving European economy ahead is the trough seen in the OECD Euro Area Leading Economic Indicator (blue line), which has already bottomed and argues for an end to the European economic growth deceleration we’ve seen since late 2010.

Source: Bloomberg

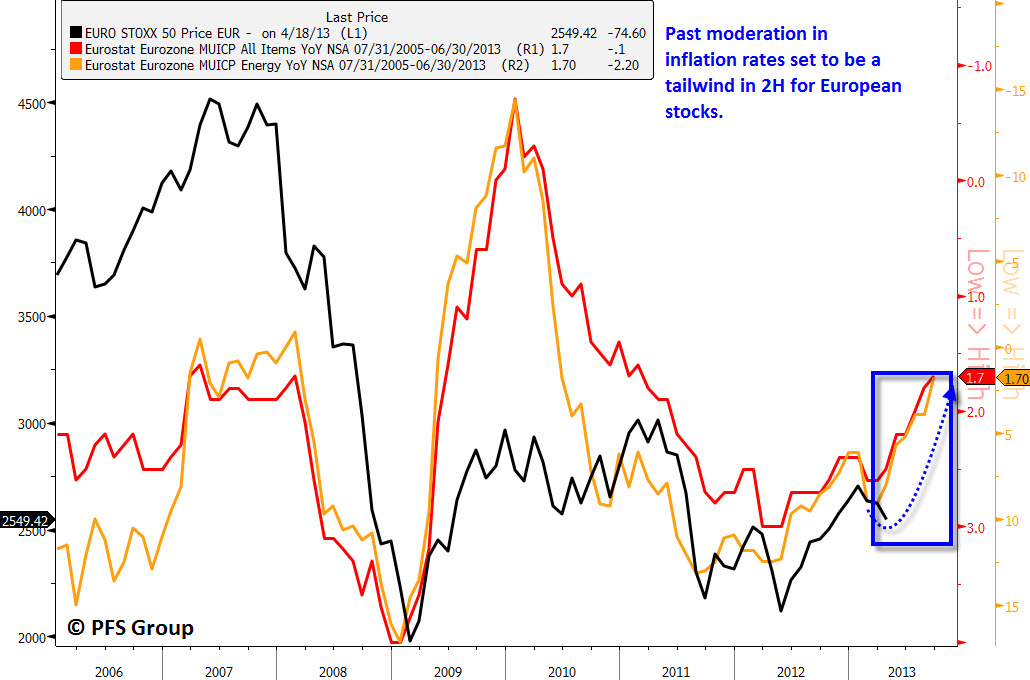

With interest rates already suppressed, Francois Trahan, Vice Chairman and Chief Strategist of Wolfe Trahan & Co., argues that inflation is the new swing factor on the business cycle, where rising inflation leads to tightening and slower future economic growth rates while declining inflation leads to easing and accelerating future economic growth. The inverse linkage between inflation rates and the stock market is shown below in which inflation rates are shown inverted for directional similarity. As seen below, the slide in European inflation rates from 2.5% to 1.7% over the last six months suggests European stocks should continue to rally strongly in 2H of 2013 after a brief pause.

Source: Bloomberg

Part of the inflationary relief set to hit Europe is the slide in Brent crude oil. Brent (red) is shown inverted relative to European equities (black line) and its recent peak coincides with a bottom in equities by June followed by a sharp rally into the fall.

Source: Bloomberg

Europe isn’t the only region set to benefit from the recent slide in energy prices however. The linkage between inflation (with energy being one of the most volatile components) and future economic growth is seen throughout the globe and suggests an improving global economic outlook ahead. Trends in economic surprises (black line) and the growth rate for the S&P 500 (blue line) are shown below along with crude oil (red line) shown inverted and advanced.

The boom/bust 12-month cycle we’ve seen over the last few years is largely a result of significant swings in inflation (energy prices) in an environment devoid of interest rate cycles (central banks adjusting balance sheets, not interest rates) over the last few years. We are currently going through another mini bust due to the prior spike in energy prices which has dented global growth while the U.S. has held up remarkably well. That said, the recent slide in oil prices suggests global growth should pick up in the 2H of 2013 with a trough in economic surprises due this summer.

Source: Bloomberg

A close-up of the chart above is shown below and suggests the current Spring swoon turns into a summer boom by June.

Source: Bloomberg

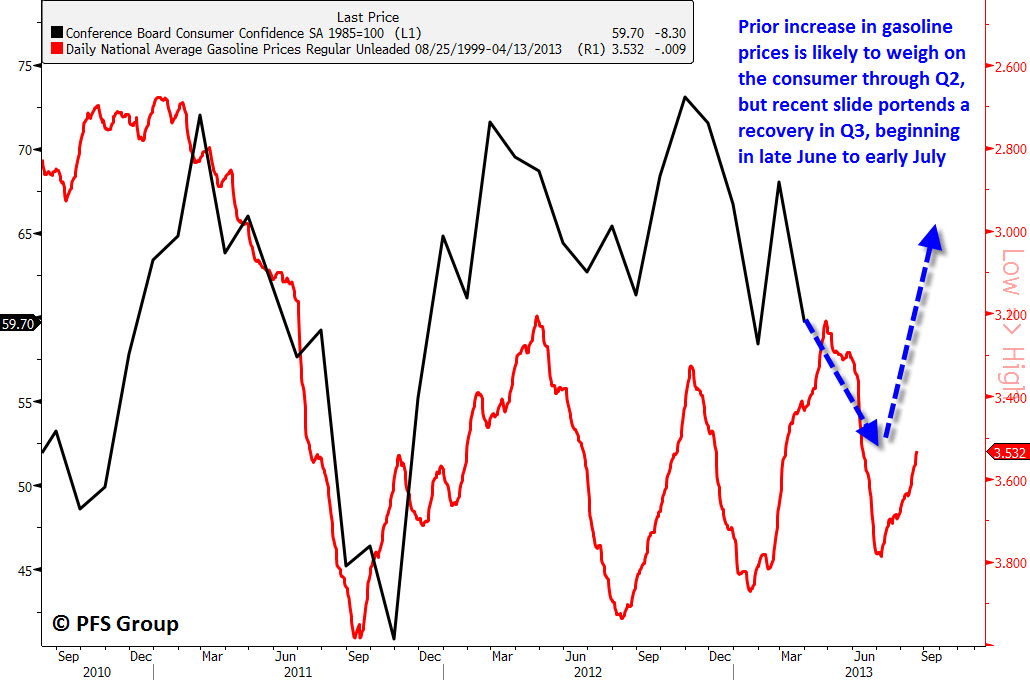

In addition to an improving outlook for economic surprises and the stock market, consumer spirits are also likely to pick up with the recent slide in gasoline prices. As consumer confidence improves, retail sales typically follow in concert so we could be setting up for a decent 2H rebound.

Source: Bloomberg

As argued previously (article link), we are likely in the middle of a Spring swoon based on a prior rise in energy prices (inflation), though the good news is the recent dramatic slide in commodities is not arguing for poor future growth as some would portend, rather the slide will provide a tailwind to economies across the globe in the second half of the year. We are likely already seeing early signs of this as RecessionAlert.com’s World Leading Economic Indicator has improved dramatically in recent months and suggests the global recession that began late last year may already be over (article link). As such, any correction we get this Spring should serve as a buying opportunity for investors, with the cyclical sectors that have underperformed this year due to their global exposure seeing the greatest improvement.