Short and quick answer, no, or at least, not yet. With the tensions escalating in the Middle East, Japan’s nuclear reactor troubles, and various countries in Europe having their debt downgraded by the ratings agencies, you would think this is 2008 all over again. However, before jumping out the window, it is important to look at the credit markets as a gauge for true risk. Currently, as you'll see below, they simply aren't yelling “FIRE”.

Credit Default Swaps Across the Globe

The cost of insuring against default can be measured by credit default swaps (CDS) which can also be viewed as the market’s perception of risk. Looking across various asset classes and regions across the globe—while there are a few hot spots—there are no widespread spikes in risk.

Below is the five year CDS for various Middle East countries. As can be seen, risk initially picked up in Egypt in January and hit a high later in the month near 450 basis points (bps), but just as the CDS for Egypt were cooling off at the end of January the risk was rising in nearby countries. Spikes in the CDS for Bahrain, Saudi Arabia, and Israel spiked up. Currently Bahrain is the greatest hot spot in the region as its CDS are spiking sharply and on the verge of rising above those of Egypt. While still relatively low, the CDS for Saudi Arabian debt is not that far off its highs and appears to be turning higher. So, there does appear to be spreading contagion risk within the Middle East, and Bahrain in particular needs to be monitored closely.

Source: Bloomberg

The Euro crisis has been in the news ongoing now for more than a year. Risk really picked up as seen by spikes in CDS on European debt last spring and remains elevated to this day. However, since November of 2010 CDS on European debt has either failed to make new highs or are actually falling, so risk in the European region is not materially elevated than where it was last spring and does not seem to be affected by the Middle East or Japanese crisis.

Source: Bloomberg

While credit risk in Europe is not escalating, it is by no means back to normal and the markets are more nervous in regards to the European situation than the Middle East crisis. This can be seen in the image below that shows a snapshot of 5-year CDS on European and Middle East Countries. Bahrain is third from the bottom at 359 and is still well below the market risk being priced in for Portugal, Ireland, or Greece.

Source: Bloomberg

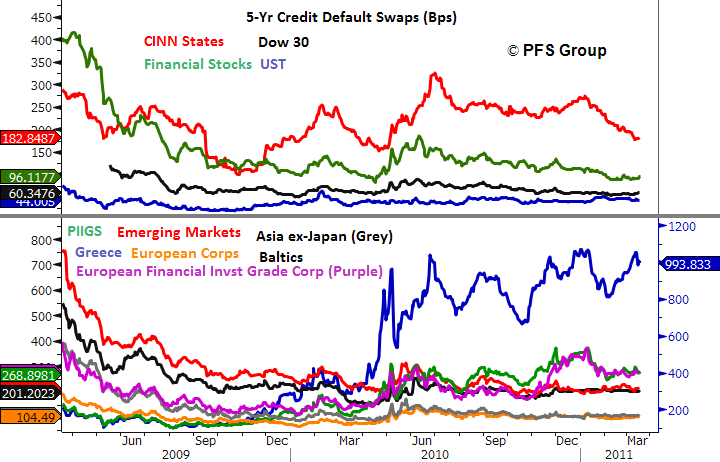

Taking a step even further back by looking at the CDS on other assets classes across the globe, credit risk in the US (top panel) remains tame and even the municipality default scare appears to be subsiding a bit as the CDS for my CINN State Composite (CA, IL, NY,NJ) peaked last June and continues to hit new lows. The CDS on US financial stocks remains low as are the average CDS on the 30 Dow Jones Industrial Average stocks. The bottom panel shows international stress that remains tame as well and is showing there appears to be no global contagion in financial risk at the present time. Credit default swaps on Asian sovereign debt, European corporate debt, emerging market sovereign debt, and Baltic’s sovereign debt all remain calm and well below their 2009 levels or even last summer’s levels.

Source: Bloomberg

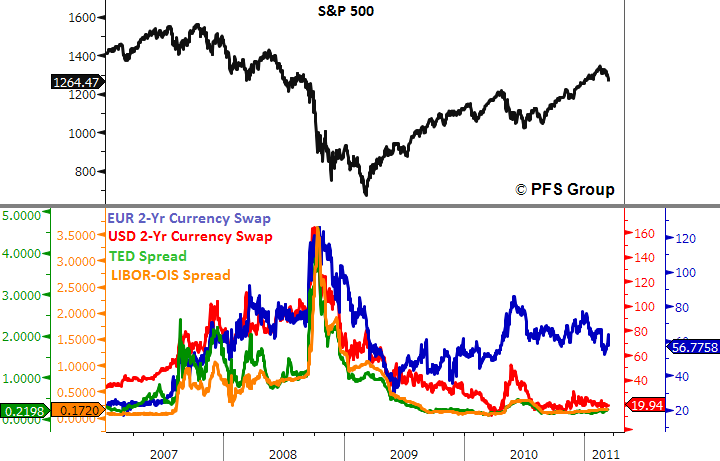

Outside of credit default swap data, various other credit spreads do not show increased financial risk as issues in the Middle East, Europe, and Japan are, at least up to the present time, contained. The Ted Spread and LIBOR-OIS spread are well bellow their 2007-2009 levels and below the 2010 summer levels. USD currency swap rates remain low though Euro currency swap spreads remain elevated and mirrors the elevated risk seen in European sovereign CDS.

Source: Bloomberg

In quick summation, while the crisis in the Middle East, Japan, and ongoing European saga show elevated risk, there appears to be no widespread global contagion in financial risk as was seen in 2007-2009, with most levels even below the heightened risk period from last summer. That said, things can change quickly and global credit risk should be monitored closely, but if we get some stability in the markets the present sell off will likely represent just an intermediate correction.

Beware of Divergences

As highlighted above, while we are not presently seeing widespread financial credit risk, I believe 2011 will be the year for risk management and the preservation of capital. “The trend is your friend” is a popular investing phrase for good reason. It is more profitable to stay with the trend then bet against it. However, at tipping points there are always signs of change and astute investors can get an early warning of a coming change in trend by studying the markets closely and one of the hallmarks of tipping points are divergences.

The biggest divergence I see presently that gives me pause and leads me to believe that 2011 will be the year the bull market comes to an end is the negative divergence between the S&P 500 and the Economic Cycle Research Institute’s (ECRI) Weekly Leading Index (WLI). The trend remains up as long as both keeping making higher highs and higher lows, but when one does not confirm the other a tipping point may have been reached.

The three biggest divergences seen in the last decade are shown below in the shaded boxes. Negative divergences were seen at the last two bull market tops in 2000 and 2007 in which the ECRI WLI provided an early warning of a change in trend by not confirming the new high in the S&P 500. We had one bullish divergence setup in 2002 in which the ECRI WLI failed to make a new low and hinted that the bear market that began in 2000 was coming to a close. Looking at the current bull market, since early 2009 the ECRI WLI made higher highs and higher lows alongside the S&P 500, but while the S&P 500 surpassed its April 2010 high the ECRI WLI is well below it and is showing the third bearish divergence in a decade.

Source: Bloomberg

My gut tells me we remain in an intermediate correction and then rally in April. I will be very interested to see the strength behind any future rally as weak breadth and momentum will be hinting the present bull market is running out of gas. If the S&P 500 rallies and fails to breach its February highs then we could be in the process of forming a market top. Market tops typically are more of a lengthy process than market bottoms, so watching for widespread deterioration in the markets underlining health should be readily identifiable if we are indeed forming one. If the signs are there that the market's trend is reversing from bull to bear then investors need to watch their portfolios closely to protect against the downside.

I believe it is always best to take a wait and see approach before declaring the market top is in. Fighting the Fed has over the last two years been a futile exercise, whereas taking one's cues from the market and staying flexible has been the way to go. As of right now the market’s trend remains bullish as seen by higher highs and higher lows, though divergence with the ECRI’s WLI suggests this trend may be in the process of reversing. I’ll be watching for more signs of divergences and weakening economic and stock market internals, but as of now the bulls still remain in charge.