While gold and silver bullion have fallen considerably since the highs reached in 2011, and mining stocks have fallen even more, I believe the weakness behind much of this move is due to the transition from the bull market in precious metals to its next phase. It is my contention that the move in precious metals since late 2008 through 2011 was largely a result of the expansion in central bank balance sheets and the perceived threat of runaway inflation. Since 2011 we’ve seen economic growth improve and inflation rates across the globe subside. As a result, investment banks and market strategists are arguing against owning gold, and making the case that, with a lack of inflation and an improved economy, the need for owning gold as an insurance hedge against inflation and currency debasement is no longer present. I strongly disagree.

Potential vs. Kinetic Energy

Before getting into the nitty-gritty data, let's quickly brush up on our physics by understanding the difference between potential and kinetic energy. An object at the top of a hill has stored energy as it rests. However, as the stored energy is released when gravity acts upon the object, the stored energy becomes kinetic (active) energy. The energy in a drawn bow before an arrow is released is another example of potential energy (stored); releasing the arrow transforms the arrow's potential energy into its kinetic energy (active energy, or the arrow's flight).

I believe there is a financial equivalent of this foundational principal of classic physics, which is: The assets on the Fed’s balance sheet (from several rounds of quantitative easing, or QE), constitute a substantial source of potential inflationary energy that has yet to translate into meaningful kinetic energy through increased monetary velocity and inflation in the economy.

It is likely that precious metals rallied strongly from late 2008 into their 2011 high, based on the increase in potential energy (size of the Fed's balance sheet) that was expected to translate into kinetic economic energy and rising inflation rates. However, high rates of inflation have yet to materialize; thus, many are giving up on the inflation thesis for owning precious metals. With an improving economy and record stock market prices the question becomes: “Why own precious metals at all?”

The Current Reasons Cited for Not Owning Gold Are Actually Reasons to Own Gold

When it comes to the reasons for owning gold or not for owning gold, we have quite a perverse situation: We believe the reasons cited for not owning gold are actually the catalysts that will propel gold into its next phase of the bull market that began late in 2008. Some strategists are arguing against owning precious metals because we have an improving economy, which they believe means that the Fed is not likely to launch further rounds of QE. Rather than being a reason why the gold bull market may be over, we believe the improving economy is a catalyst for gold’s transition into its next bull-market phase. One of the primary reasons why we have yet to see all of the Fed’s money printing translate into high rates of inflation is that money velocity (a measure of how quickly money turns over in the economy) remains low: banks have been reluctant to lend after suffering devastating loan losses after the 2008 financial crisis. Prior loan losses coupled with high rates of unemployment and slow job growth are not the environment that spurs banks to lend, which keeps money velocity low.

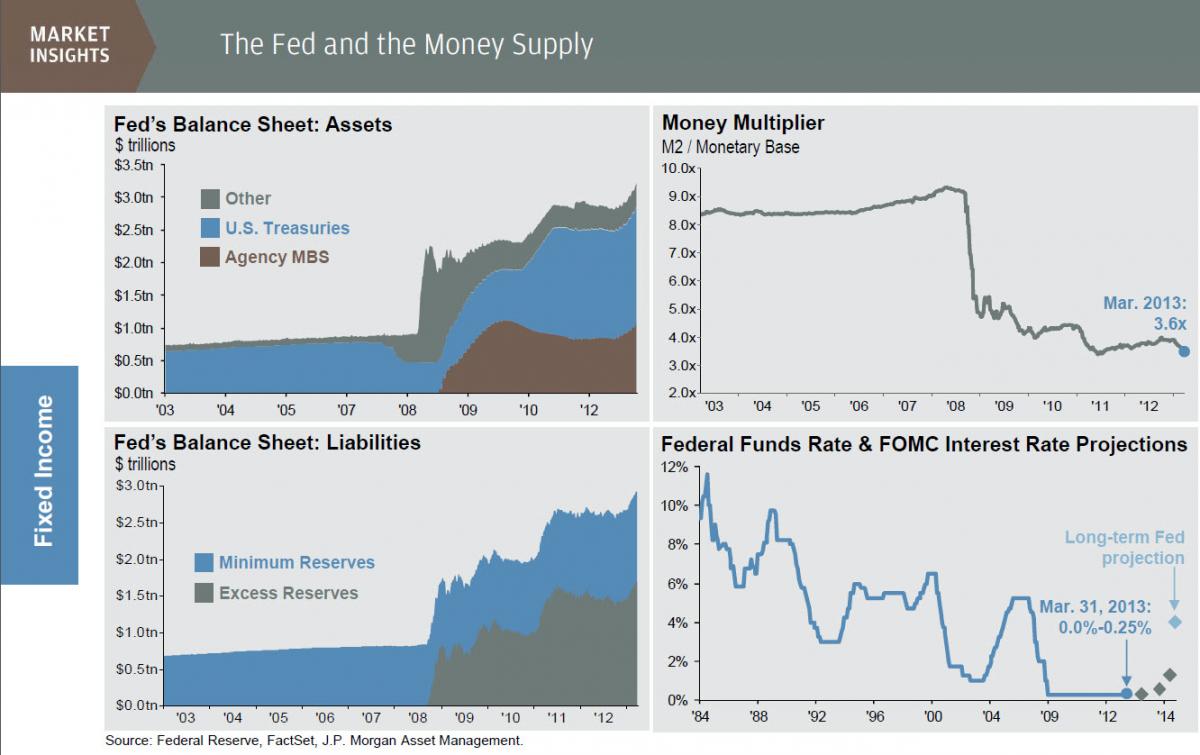

Much of the money created by the Fed just sits on its balance sheet in the form of “excess reserves.” Note the chart in the bottom left below in which, prior to 2008, excess reserves were negligible relative to minimum reserves. However, since then, the spike in the Fed’s liabilities has largely been associated with banks keeping excess reserves at the Fed, and consequently money velocity, as seen in the top right corner below, has collapsed.

Source: JPM Market Insights, Q2 2013

This is important to understand, as there is a strong link between money velocity and inflation. Generally, the faster money turns over in the economy, the higher inflation rates climb. The correlation between the two is shown below during the inflationary 1970s, which characterized the last secular bull market in precious metals. You can see clearly how money velocity and inflation rates moved together. Thus, with money velocity collapsing in recent years, it shouldn’t be surprising that we do not have runaway inflation. That said, recent changes in bank lending suggests this is about to change.

Source: Bloomberg

The Resurgence of Inflation

The argument that, since the economy is improving (i.e. there is no need for further QE), there is no reason to own gold, actually is the very reason why banks are likely to accelerate lending. Shown below is the growth in commercial bank credit, along with the unemployment rate (inverted for directional similarity). As seen below, when the unemployment rate falls (rises in chart), bank lending generally picks up. The unemployment rate peaked late in 2009 with loan growth subsequently bottoming in early 2010. As the unemployment rate continues to fall, we are likely to see loan growth continue to accelerate ahead.

Source: Bloomberg

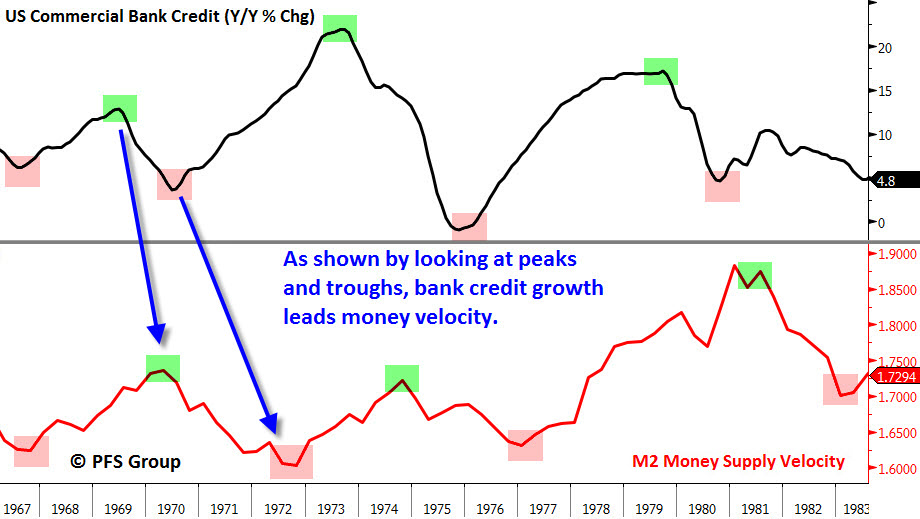

Trends in bank lending play a pivotal role in money velocity; this is a key piece of data for believing that the next phase of the precious metals bull market lies ahead. The more banks lend, the more money enters the economy and changes hands, leading to higher rates of economic activity and thus higher rates of inflation. The tendency is for growth rates in commercial bank credit to lead trends in money velocity. An example of how commercial bank credit growth trends played a key role in the inflationary 1970s is shown below.

Source: Bloomberg

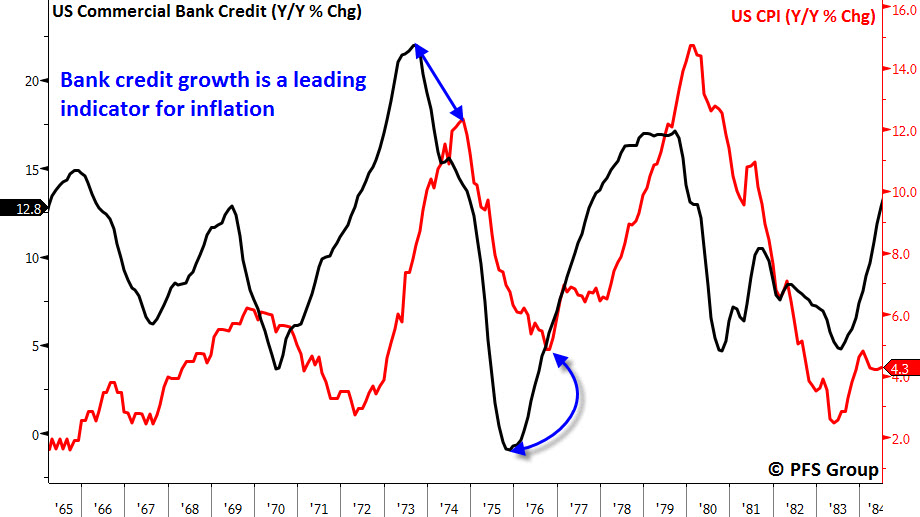

Due to the linkage between money velocity and inflation rates, it is not surprising that bank credit growth also leads trends in inflation, as shown below.

Source: Bloomberg

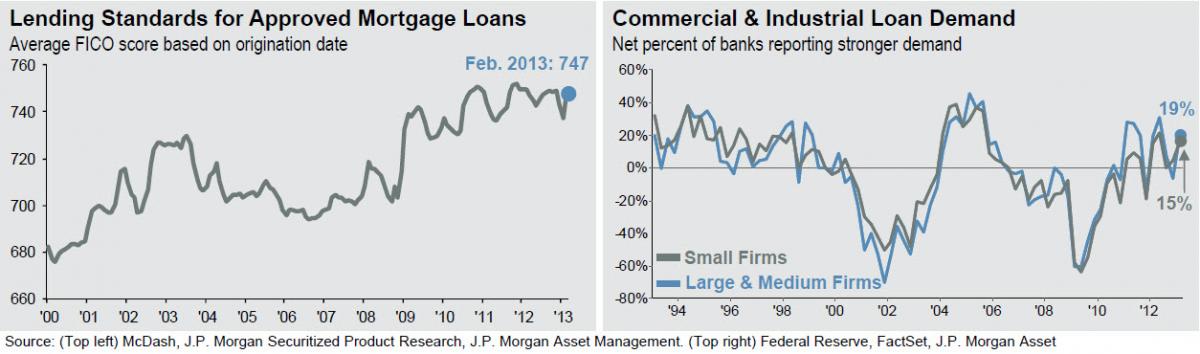

Not only is the unemployment rate currently falling, but the average FICO score for consumers being approved for mortgage loans is near the highest levels seen in over a decade. An improving economy and improving consumer creditworthiness are leading to a pick-up in bank loans to consumers and corporations, as highlighted below.

Source: JPM Market Insights, Q2 2013

Just like the bottoming of bank credit growth in 2002 eventually led to a pick-up in money velocity in the 2003–2007 economic recovery, the recent surge in bank credit growth is likely to cause money velocity to rise as banks become more willing to lend.

Source: Bloomberg

I believe metals sold off as investor fears over runaway inflation subsided, as well as from the perception that an improving economy would lessen the need for the Fed to launch more QE programs.

If inflation were more directly correlated to the Fed's balance sheet and its QE programs, then it would make sense to move away from metals if and when the Fed slows down QE. However, the size of the Fed's balance sheet alone (potential energy) is not the driver of inflation: it is the banking industry's willingness to put that money to work—to lend (kinetic energy)—that spurs money velocity, which drives inflation.

I believe that as focus moves away from the Fed's balance sheet as an inflation indicator—and a reason to own, or to not own, gold—and shifts to a focus on rising bank credit growth as an inflation indicator, money velocity will cause precious metals to shine once again.

Intermediate Outlook Bullish

While the macro picture thesis was outlined above, I wanted to touch on the current outlook for precious metals. We are likely witnessing a washout point in which precious metals have been sold off to such an extent that they are likely to snap back sharply, like a stretched rubber band. Currently, investors are far too bearish on the sector, and far too bullish on the USD, similar to what occurred at the 2008 bear market lows.

The Commitment of Traders (COT) report is a useful tool for gauging sentiment. The report breaks down the open interest for various markets and shows the positioning of commercials and non-commercials (AKA: speculators) in the futures markets. It is assumed that commercials are the “smart money” and the speculators are the “dumb money.” Typically, when speculators are overwhelmingly bullish (net long), a top is usually near, and when they are overly bearish (net short), a bottom is typically near.

The speculators' (non-commercials') investment in USD futures, and their bullish sentiment, is at levels that have marked meaningful tops in the USD over the last five years (red shaded box below). As such, we are likely witnessing a top in the USD, which should act to lead precious metals higher.

Source: Bloomberg

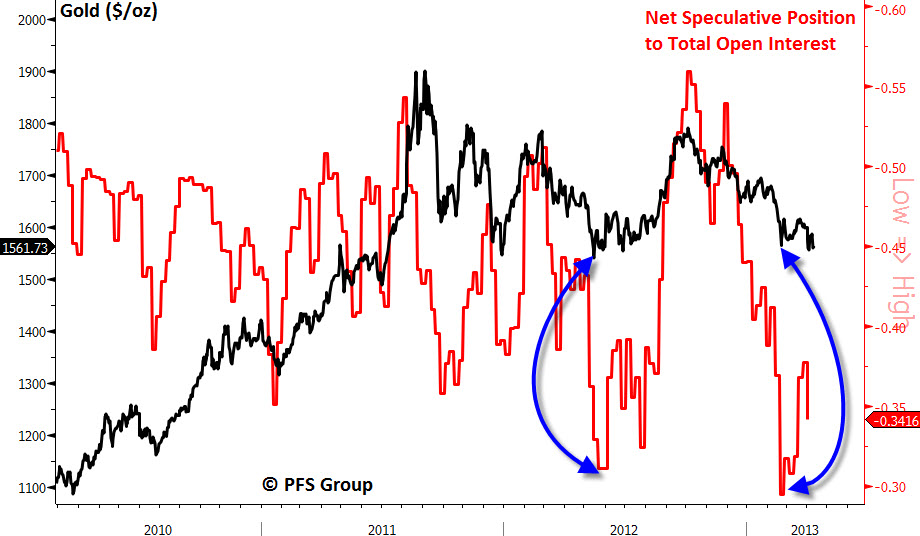

While speculative sentiment on the USD is overly bullish, sentiment towards gold is coming off the most bearish reading in three years, and likely signifies a bottom. The last time speculative sentiment got this bearish on gold was at the 2012 lows before gold rallied nearly 0/oz. over the following months.

Source: Bloomberg

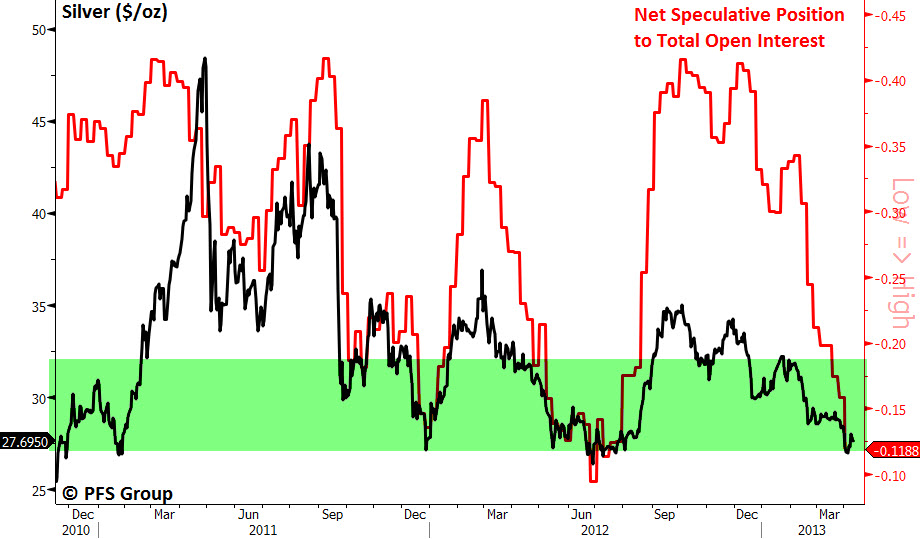

Sentiment on silver is also hitting a bearish extreme, suggesting that we likely are near a low in silver as well.

Source: Bloomberg

The situation in the metals market right now is very similar to what occurred late in 2008, when sentiment was overly bearish on the precious metals sector, and valuations had been greatly compressed. Looking at the price multiples on the HUI Gold Bugs Index to shed light on current valuations shows that mining stocks are at a price-to-cash flow (P/CF) and a price-to-sales ratio (P/S) that is currently as cheap as it was at the October 2008 lows, and at or near the valuations seen when the bull market in precious metals began in 2000.

Source: Bloomberg

In addition to bearish sentiment and valuations hitting an extreme, our technical indicator for the HUI Gold Bugs Index is hitting levels only seen four times in the last 13 years, suggesting we have reached a washout point in the sector, which should lead to a significant bottom.

Source: Bloomberg

With sentiment, valuations, and technical levels all at extreme bearish levels, a significant bottom in the sector is likely upon us. With gold breaking marginally below its 2011 and 2012 lows near 40, we may have one more downward move, but the more we decline the more violent the recovery rally is likely to be. My thesis of a resurgence in inflation to help propel precious metals higher is likely to play out beginning in the second half of the year and into 2014. Until we see signs of inflation beginning to accelerate the sector may remain weak. That said, with valuations resting at bear market lows the downside risk is certainly diminishing the further we decline.

For a free subscription to the weekly Best of Financial Sense Newsletter, CLICK HERE to subscribe.