Summary

- Net foreign purchases of US stocks turning up

- Corporate buybacks also acting as a support for the market

- Large potential short squeeze to serve as another bid

- Taken collectively, still too soon to turn bearish

It's always a good idea to periodically take a look at what the foreign community is doing in terms of net US equity purchases. The reason lies in the fact that they tend to buy at tops and sell at bottoms and can serve as a contrary indicator. We saw this not only in the 2000 and 2007 bull market peaks but also the 2003 and 2009 bear market bottoms.

So what do current levels of foreign purchases suggest for US stocks? They reflect more of a bottom than a top as net foreign purchases are coming off of multi-decade lows set earlier in the year and are close to moving into positive territory. Shown below is the S&P 500 on the top panel and the 1-year moving average of net foreign purchases on the bottom and you can clearly see that rising foreign purchases are associated with bullish moves in the stock market. Given the low level of current purchases we could continue to see an influx of foreign buying of US equities in the weeks and months ahead.

Source: Bloomberg

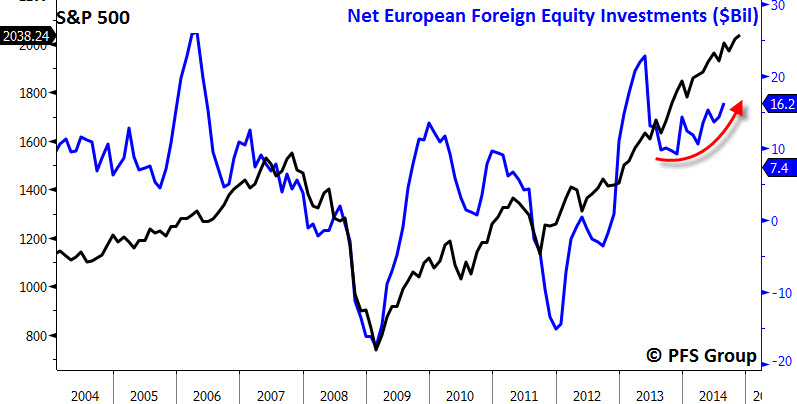

Part of the foreign inflows into US stocks is likely coming from Europe given the malaise of the region and the poor economic growth. Typically increases in net foreign stock purchases by the Eurozone translate into higher stock prices in the US with 2013 as a perfect example. Heading into 2013 net foreign equity purchases by the Eurozone were slowly declining but then surged strongly to nearly B a month by early summer before moderating back down to roughly B a month. Currently, European purchases of foreign stocks have picked and are likely serving a bid to our markets.

Source: Bloomberg

The market rally off the October bottoms has had a defensive feel to it as high quality stocks are outperforming low quality names. Foreigners typically buy large-cap strong balance sheet companies and so the outperformance of high quality stocks over low quality is likely an indicator of an increase of foreign inflows rather than a peak in the stock market often associated when lower quality names underperform.

Another widely known support for the markets currently as well is corporate buybacks, which, ironically, was also partially attributed for the October correction:

Is This the Beginning of a New Bear Market? Important Signs to Watch

Most corporations are precluded from buying back their shares during the five weeks before their earnings release and so the month before the onset of earnings releases typically show the lowest percentage of share buybacks seasonally. Peak earnings releases for the S&P 500 will be between October 13th and October 31st, which is significant as four to five weeks prior the S&P 500 peaked as a major buying source of the market dried up. Near the end of this month roughly 75% of the S&P 500 companies will have reported and will be able to restart their share buyback programs. According to Goldman Sachs data going back to 2007, roughly 25% of annual share repurchases occur in the last two months of the year with November being the largest month (14% of total annual share repurchases). This indicates corporations may be a significant marginal buyer of the stock market beginning in the next few weeks.

As mentioned in the excerpt above, according to Goldman Sachs roughly 25% of total annual share repurchases occur in the last two months of the year and suggests there is plenty of support for this market into year end. Tracking buybacks can be very helpful in identifying major market turning points since investors tend to sell stocks when the company is buying back their equities at rich valuations and then underperform the general stock market.

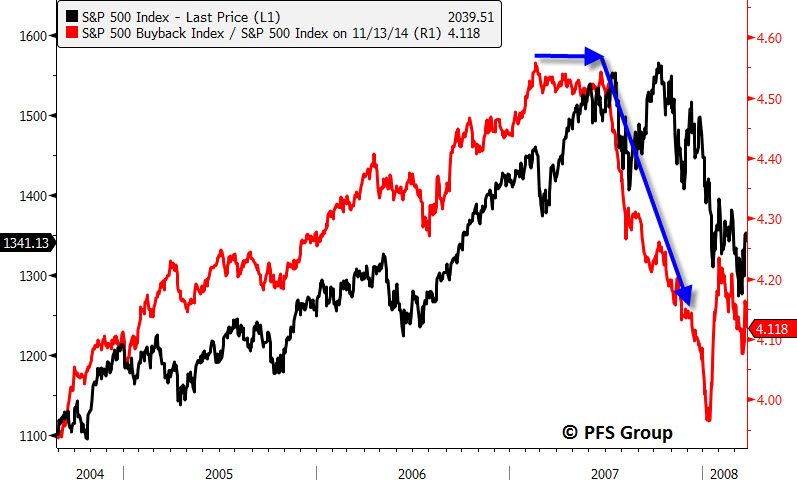

Because of this, tracking the relative performance of the S&P 500 Buyback Index to the S&P 500 can provide an early clue of an impending major market top. This was the case leading up to the 2000 bull market top in which companies with large buyback programs began to be penalized by investors beginning in 1997 as the S&P 500 Buyback Index underperformed the S&P 500 by a large degree in the last few years of the 1990s.

Source: Bloomberg

A similar situation was seen in 2007 when the market shot higher heading into the summer but the S&P 500 Buyback Index stopped outperforming the S&P 500 and then virtually collapsed in the last six months of the year as investors took companies to task for wasting shareholder money by buying back overly priced stocks.

Source: Bloomberg

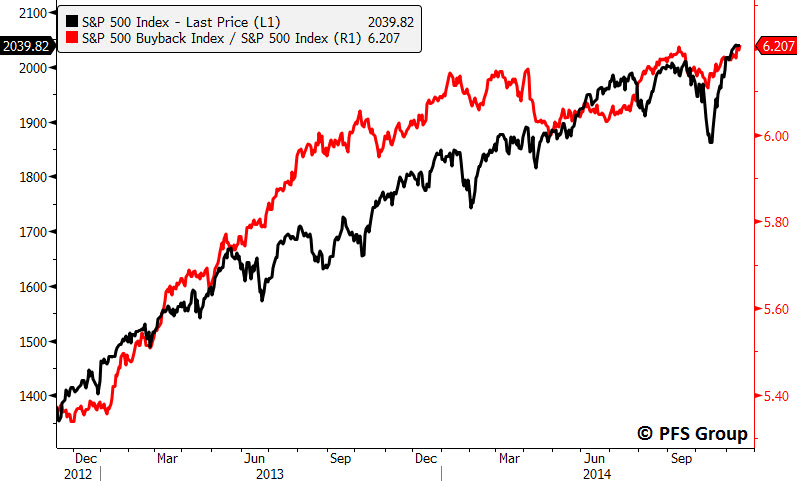

When you look at the market today you do not see any of the glaring divergences above that were associated with the 2000 or 2007 tops and suggests we haven’t reached the peak of this bull market.

Source: Bloomberg

Another development to keep in mind is that short interest on the New York Stock Exchange is at levels that nearly match the March 2009 bottom and have eclipsed the levels that marked the 2010, 2011, and 2012 bottoms. As I’ve said before, the time to be bearish is when everyone is bullish – short interest levels do not convey this message at all.

Source: Bloomberg

There are some sentiment surveys that show elevated bullishness but I tend to put more value on data that follows what people are doing rather than what they are saying; actions speak louder than words and short interest levels are providing a bullish contrary signal.

Summary

The trends in net foreign purchases and the outperformance of the S&P 500 Buyback index suggests a major market top is not in the offing as neither are signaling a market peak as they did at the 2000 and 2007 tops. Additionally, the large net short interest levels on the New York Stock Exchange suggests a significant chance of a short covering rally that could lift the markets higher. Collectively, the data above cautions against turning overly bearish on the markets despite the strong run off the October lows. There still remains plenty of support underneath this market to carry it higher in the weeks and months ahead.