We are starting to see weakening in breadth data that is suggestive of a possible short-term correction in the market. With the highly anticipated upcoming September 17-18 FOMC meeting, we could be in store for some volatility and market weakness.

While it is highly anticipated that the Fed will begin to taper its quantitative easing (QE) program next month, what the market is uncertain about is by how much and at what pace. This uncertainty will likely keep the market’s near-term upside potential limited and may open up a small correction or consolidation.

Related: Jeff Saut: The Market Is Overbought – Raise Some Cash

Once we have the uncertainty behind us the markets are likely to head to new highs given how robust the market currently is (excluding short-term divergences) as well as having an accelerating economy, as seen by the sharply rising service and manufacturing PMIs that were released last week.

One negative divergence I am seeing is the 200-day moving average (200d MA) for the daily NYSE advance-decline line, which is diverging with the S&P 500, as is the 20d SMA of the NYSE percent new highs minus new lows. While we are seeing some negative divergences in the two indicators below, they remain in positive territory and we would need to see dips into negative territory before even remotely considering the potential for a major market top.

Related: Martin Armstrong: Dow May Double by Late 2015

Source: Bloomberg

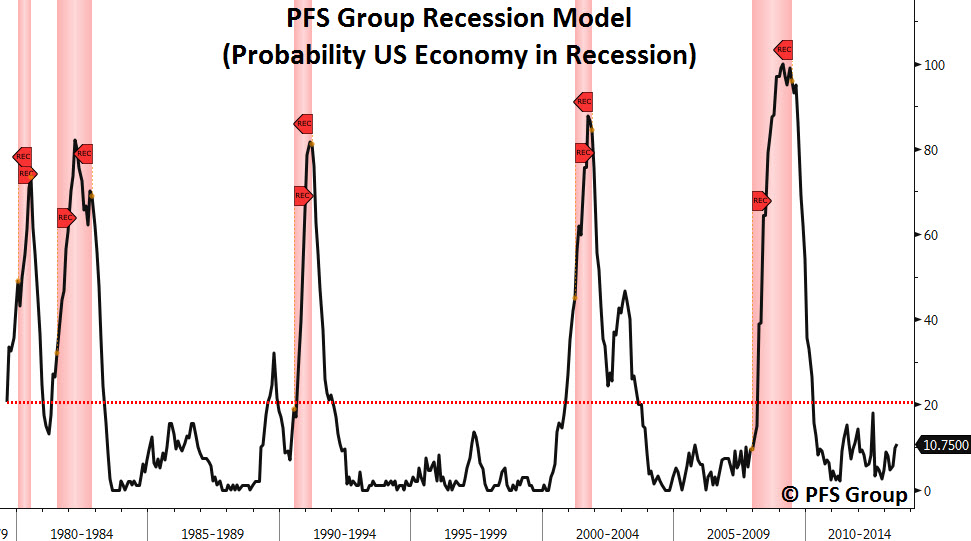

In addition to the technical data that argues against a major market top, various economic and financial indicators are not warning of any major market peak. The stock market has moved into a bear market with every single recession and, currently, the risk of a recession is minimal as seen by our recession model (recessions shown in red shaded lines):

Source: Bloomberg

We can have bear markets without a recession, however, and so checking the health of the credit markets can shed light on whether a non-economic financial crisis is brewing. To gauge these sorts of financial risks we can look at the Bloomberg Financial Conditions Index (red lines) for the US (top panel) and Europe (bottom panel), which are both resting near their highs of the last five years and signal that there is no mounting risk to our financial system at the moment.

Please note in the chart below that the Financial Conditions Indexes peaked well before the market did in 2007 (red circles) and also bottomed in 2008, more than 6-months before the market bottomed (green circles), showing that the credit markets caught the major turning points in the market/economy well before the stock market did. Thus, the fact that the US Financial Conditions Index rests at a 17-year high and the European Financial Conditions Index Rests near a 5-year high shows there is no brewing financial crisis in the U.S. or in Europe that the stock market is unaware of.

Source: Bloomberg

In summary, there are some negative divergences in short-term breadth and momentum that suggests a short-term top may be forming. My guess is that uncertainty around how much and how quickly the Fed will begin tapering its QE program will lead to market weakness this month. However, once this uncertainty is laid to rest after the September 17-18th FOMC meeting I believe we will see new highs moving forward given the market's strong long-term breadth and momentum. Most importantly, the cyclical sectors of the market are leading (financials, consumer discretionary, and industrials) as they are likely discounting an accelerating US economy.