The latest issue of the NFIB Small Business Economic Trends is out today (see report). The April update for March came in at 89.5, which puts it deep in the cellar at the 9th percentile in this series, where a distinctly recessionary mood prevails.

Here is the opening summary of the report:

After three months of sustained growth, the March NFIB Index of Small Business Optimism ended its slow climb, declining 1.3 points and landing at 89.5. In the 44 months of economic expansion since the beginning of the recovery in July 2009, the Index has averaged 90.7, putting the March reading below the mean for this period. Of the ten Index components, two increased, two were unchanged and six declined. Among the greatest declines were labor market indicators, inventory investment plans and sales expectations.

"After another false start, small business confidence has sputtered and stalled again. For the sector that produces half the private GDP and employs half the private sector workforce — the fact that they are not growing, not hiring, not borrowing and not expanding like they should be, is evidence enough that uncertainty is slowing the economy. Virtually no owners think the current period is a good time to expand, because they simply don’t know what the future holds. So why invest? And with the lack of any sustainable fiscal policy or a federal budget, no one’s banking that Washington will be at forefront of any meaningful change. Overall, it appears that there will be little growth coming from the small business half of the economy; as the world economy slows, even big business may suffer." --NFIB chief economist Bill Dunkelberg

The first chart below highlights the 1986 baseline level of 100 and includes some labels to help us visualize that dramatic change in small-business sentiment that accompanied the Great Financial Crisis. Compare, for example the relative resilience of the index during the 2000-2003 collapse of the Tech Bubble with the far weaker readings of the past three years. The NBER declared June 2009 as the official end of the last recession.

The average monthly change in this indicator is 1.29 points. To smooth out the noise of volatility, here is a 3-month moving average of the Optimism Index along with the monthly values, shown as dots.

Inventories And Sales

The findings on small business sales and sales expectations continue to highlight a fundamental source of distress.

The net percent of all owners (seasonally adjusted) reporting higher nominal sales over the past three months was negative 7 percent, an improvement of 2 points and the best reading in eight months. However, firms are still reporting more declines than gains. Such a negative outlook will not stimulate a lot of hiring or spending or inventory investment. The net percent of owners expecting higher real sales volumes fell 5 points to a negative 4 percent of all owners (seasonally adjusted), 16 points below the 2012 cycle high of a net 12 percent reached in February 2012. Seventeen (17) percent of small employers cite weak sales as their top business problem, a one point improvement over February.

Credit Markets

Has the Fed's strategy of quantitative easing had a positive impact on Small Businesses?

Credit demands remained weak in March. Twenty-nine (29) percent reported all credit needs met, and 49 percent explicitly said they did not want a loan (64 percent including those who did not answer the question, presumably uninterested in borrowing as well). Seven percent of owners surveyed reported that all their credit needs were not met, unchanged from February and 3 points above the record low.

NFIB Commentary

This month's "Commentary" section offers a context for the March decline after three months of slow growth:

Small business produces half the private GDP and employs half the private sector workforce. But it is not growing, not hiring, not borrowing and not expanding enough. Small business owners have been depressed since 2007 and that has not changed. In the March survey of NFIB’s 350,000 member firms, 77% expect the economy to be no better or even worse 6 months from now that it is currently. Only 4% think the current period is a good time to expand substantially, compared to an average of 17% for the period 1973 to 2007. More owners plan to reduce employment in the coming months than plan to create new jobs. More owners plan to reduce their inventories than plan to order new stocks. The bulk of growth comes from the increase in our population of about 3 million people and the growing need to simply replace stuff that is wearing out, not enough to get the economy back to trend growth much less the strong growth needed to restore employment to 2007 levels.

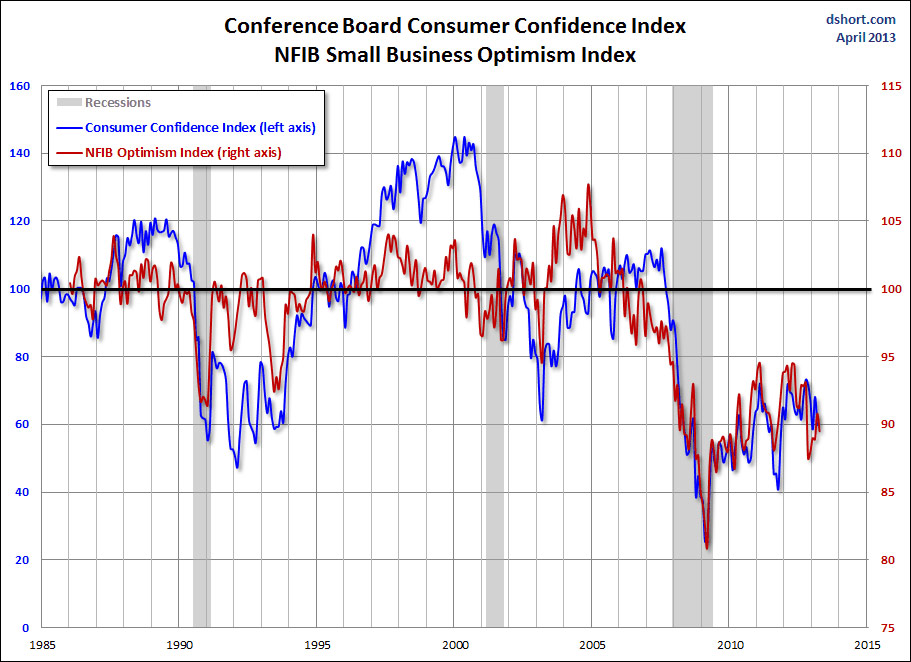

Business Optimism and Consumer Confidence

The next chart is an overlay of the Business Optimism Index and the Conference Board Consumer Confidence Index. The consumer measure is the more volatile of the two, so I've plotted it on a separate axis to give a better comparison of the volatility from the common baseline of 100.

With the latest NFIB data, we continue to see that the mood of small businesses is highly correlated with Consumer Confidence.

Source: Advisor Perspectives