The Shadow WLI is a research project stemming from the initial work of Franz Lischka, subsequently enhanced by the Dwaine van Vuuren, Georg Vrba, Franz Lischka, Doug Short global collaborative team. It is derived from five leading weekly U.S economic indicators, three of which are available on Mondays and the final two available by Thursdays. It is published twice weekly, on Mondays (1st estimate) and Thursdays (final estimate) by 13H00 EST (best effort so do not hold us to this). Obviously the final estimate will be more accurate than the 1st estimate as it will include all 5 components.

The weights attached to each of the five components have been optimized with multiple regression analysis to maximize the correlation between the Shadow WLI and the ECRI WLI. For the periods commencing Jan-1-1990 and Jan-1-2010 the correlations are very high, the coefficients being 0.946 and 0.938, respectively. The Shadow WLI gives you two estimates of the ECRI WLI before it is published on Fridays at 10am to the public. The Thursday final estimate of the Shadow WLI is also used as input into the Thursday Weekly Superindex flash-estimate delivered to RecessionALERT.com subscribers.

The Shadow WLI does not replace the ECRI WLI, its sole purpose in life is to give investors 4 days advance (1st estimate) and 1-day advance (final estimate) readings of the figure eventually published by ECRI on Fridays. Thus all figures shown in below charts are actual ECRI WLI figures except the final week which is the forecast Shadow WLI reading. This research page (found here) will act as central point for all Shadow WLI updates, so you can bookmark it if you want. For now, the updates are free to the public.

11 Jun 2012 : The Shadow WLI (1st estimate) is 121.2 with its growth metric WLIg of -3.03. We are at alert level DEFCON-3 (last week DEFCON-4) as the WLIg has fallen below its optimal recession trigger. The DEFCON change has escalated the recession probability from 0.17 to 0.31.

To properly understand & appreciate the above charts please read “Using the ECRI WLI to flag recessions“ and also the follow-on titled “Further improving the use of the ECRI WLI.” As these research notes point out, you should never let a single indicator (such as the WLIg or its variants shown above) form the basis of your investment decisions. It is far better to adopt a staged multi-pronged approach such as our RFE Model.

How Do the Shadow WLI Defcon Levels Work?

We have adopted a 5-stage recession alerting mechanism modeled on the Defense Readiness Condition alert posture used by the US armed forces, which prescribes five graduated levels of readiness (or states of alert) and increase in severity from DEFCON 5 (least severe) to DEFCON 1 (most severe) to match varying military situations. We use the 4 WLI growth variants discussed in the two papers mentioned above to derive the DEFCON level. Each time one of the following conditions occur, the DEFCON is raised a level in severity (i.e. decreased by 1):

- WLIg (the growth metric published by ECRI) falls below its “golden trigger” of -2.63 (a condition that resulted in 12 false positives in the past)

- WLIg+ falls below zero (a condition that has resulted in 4 false positives in the past)

- WLIG+2 falls below zero (a condition that has resulted in 2 false positives in the past)

- WLIG+1 falls below zero (a condition that has resulted in 1 false positives in the past)

Each time one of the above conditions changes from true to false, the DEFCON is lowered a level in severity (i.e. increased by 1).

How Do the Shadow WLI Recession Probabilities Work?

The recession probability is calculated from a 5-factor Probit statistical model that looks at WLIg, WLIg+, WLIg+1,WLIg+2 and the DEFCON level to determine probability of being in a recession now. This multi-factor probability model is far superior to any of the single-factor models for each of the individual components and is therefore more representative of recession risk. Using recession probability to make recession calls requires using a trigger of 0.53 (53% chance of recession) for optimal long-term accuracy.

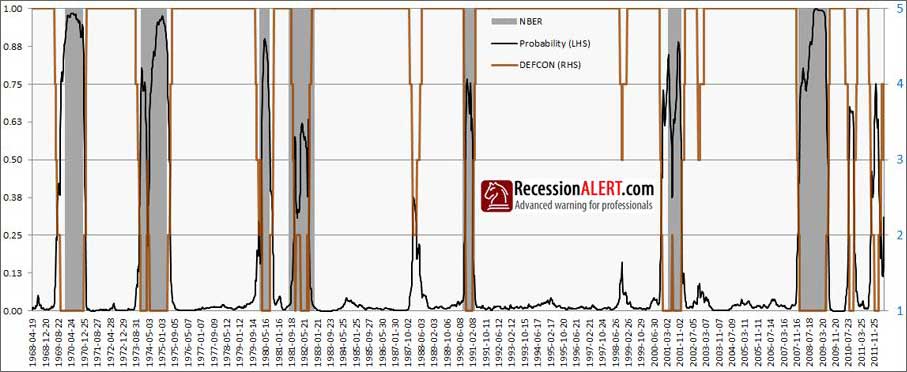

Defcon Severity & Probability of Recession History

Historical plots for DEFCON ratings and probabilities of recession are shown below. As you can see the method, despite its sophistication, is still subject to recent false positives. Therefore you are discouraged from relying on these charts alone for investment descisions. Rather use a more sophisticated multi-model approach such as our Recession Forecasting Ensemble (RFE) that has not suffered from false positives yet.

Source: Recession Alert