In 2009, China spent $89-billion for imports of crude oil, $50-billion on iron ore, and $30-billion on copper. However, even before the final tally for 2010’s import bill is calculated, Beijing understands that the era of cheap commodities is over, and that if continues to target economic growth of 9% or more, it’ll have to pay a heavy price. Beijing has been backed into a corner, by the US Treasury, and its powerful allies at Japan’s ministry of finance, and must soon decide how to navigate its economy in the year ahead. The threat of hyper-inflation looms on the horizon.

As the final days of 2010 are drawn to a close, the landscape of the commodity and financial markets has been turned upside down from just two-years ago. The price of copper has soared to record heights at $9,400 /ton in London, more than 3-½ times higher than its lowest point hit two years ago. Crude oil has rebounded to $92 /barrel, up from a crash bottom low of $33 /barrel, and cotton has skyrocketed 95% this year to $1.44 /pound in New York, up from 60-cents two-years ago. Overall, the Continuous Commodity Index (CCI) has recouped all of its losses from the post Lehman Brothers’ meltdown, and is climbing to new all-time highs.

Fueling the advance of the resurgent “Commodity Super Cycle,” is booming demand from emerging countries. China and India in particular, are now engaged in the construction of new airports, railways and new cities, activities that demand a lot of steel, and its key ingredients - coking coal, iron-ore, and nickel. China is set to continue to tap international markets for farm commodities in 2011, to replenish reserves that got dangerously run down this year. China’s stocks of corn, sugar and cotton are thought to be below one month's supply.

On a per capita basis, mainland China and India’s consumption of oil and metals is still only a fraction of those of the more developed countries like the US, Japan and South Korea, suggesting that the potential growth of this emerging commodity demand would be enormous in the years ahead. And if an economic recovery in the G-7 nations takes hold in 2011, it’s possible that severe shortages of key raw materials could materialize, sending commodity indexes higher yet.

During the past year, the emotions of equity traders swung between the exhilarating impact of the Federal Reserve’s electronic printing press, and the fear of a possible “double-dip” recession, emanating from the Greek debt crisis, or a sharp slowdown in China’s economy, due to a tighter money policy. But while the Greek debt crisis triggered the May 6th, “Flash” Crash on Wall Street, sparking a 1,000-point intra-day plunge in the Dow Jones Industrials, investors in commodities stayed bullish, and handily beat stocks and bonds by a huge margin in 2010.

While global stocks are still about -trillion short of the record .6-trillion of market capitalization reached in October 2007, silver has soared 75% higher from a year ago, to its highest level in 30-years. Coffee is up 73%, corn up 48%, wheat up 45%, orange juice up 31%, and soybeans up 30-percent. The cost of unleaded gasoline in New York is up 55-cents a gallon since late August. Yet the upward explosion in commodity prices this year isn’t even on the Fed’s radar screen, since it routinely excludes food and energy from its definition of inflation.

Even as the commodity markets continue climb to new record heights, the Fed aims to pour more fuel into the tank of the “Commodity Super Cycle,” by injecting an extra 0-billion of high octane liquidity into the US-money markets in the first half of 2011. Traders are already betting on QE-3, with a median estimate of 0-billion of additional liquidity. The Bank of Japan, is also injecting an extra -billion into the Tokyo money markets, under the guise of its QE-3 scheme, including the purchases of ETF’s linked the Nikkei-225 index, and REIT’s for a new twist, that’ll whet the appetite of Japanese speculators in the world markets.

Since July, European banks have been expanding their commodities trading desks in Asia as the region’s rapid growth prospects and regulatory changes in Europe and the US pull investors east. While establishing footholds in emerging giants such as China and India, banks are also focused on stuffing their portfolios with grains, precious metals, iron ore, coal, rubber, and crude oil. The Agricultural Bank of China built round-the-clock commodity trading teams in New York and London this year, to further Beijing’s ambition to be a major force on commodity markets.

Soaring commodity prices are celebrated by the Fed, since it removes the threat of a deflationary spiral plaguing the US-economy. However, in China and India, home to one third of the world’s population, the specter of soaring commodity prices is viewed with grief stricken horror. In rural areas where huge throngs of citizens live on wages of less than /day, more than half the household budget is spent on staple commodities, such as corn, rice, palm oil, soybeans, and petrol. Beijing admits that the consumer price index in China is +5.1% higher than a year ago, it’s highest in 28-months, and worries that a 10% inflation rate lies ahead.

On Sept 16th, US Treasury chief Timothy Geithner advised Beijing to allow a “significant and sustained rise in the yuan’s value” against the US-dollar, as an expedient tool to dampen the inflation pressures from soaring commodity prices. “The pace of the yuan’s appreciation has been too slow and the extent of appreciation too limited. We are examining the important question of what mix of tools, those available to the United States and multilateral approaches, might help encourage the Chinese authorities to move more quickly,” Geithner warned.

Three months earlier, on June 19th, the People’s Bank of China (PBoC) said it would allow a more flexible exchange rate for its currency, after it was frozen for two-years against the dollar at 6.82-yuan. Yet the pace of the yuan’s appreciation was very slow, gaining only 1% over three-months. New York Senator Charles Schumer commented “Until there is more specific information about how quickly China will let its currency appreciate and by how much, we can have no good feeling that the Chinese will start playing by the rules,” he warned. Michigan’s Senator Sander Levin added, “We’ll see if China’s action in this immediate period really reflects a very significant change in policy. We follow the yuan every day,” Levin warned.

Yet China’s decision to bow to American pressure to un-hinge the dollar /yuan peg, was one of the key sparks, that ignited the latest upward thrust of the “Commodity Super Cycle,” and is now boomeranging on Beijing. But the big blow was dealt by Fed chief Ben “Bubbles” Bernanke, acting at the directive of the US Treasury, on August 28th, when he told the world’s top central bankers, gathered at Jackson Hole, Wyoming, that a second tsunami of QE, would soon be unleashed upon the globe.

In its simplest form, “quantitative easing,” (QE) is nothing more than massive money printing, designed to dilute the value of US-dollars floating in circulation. And since most globally traded commodities are priced in dollars, when the value of the dollar goes down, the prices of commodities and precious metals usually climb higher. China’s trade minister Chen Deming lamented, “Uncontrolled printing of dollars and rising international prices for commodities are causing an imported inflationary shock for China and are a key factor behind increasing uncertainty.”

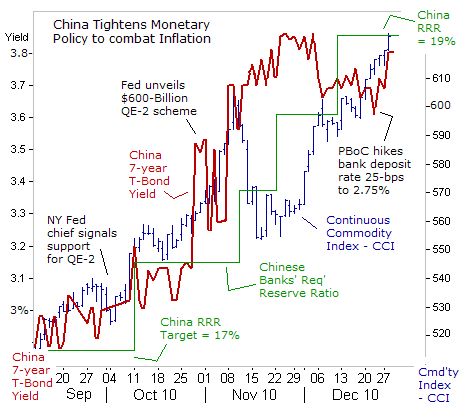

The US money supply, as measured by MZM, has mushroomed by nearly $500-billion since late April, and is fueling the explosive surge of the “Commodity Super Cycle,” to record heights. Beijing has responded to the surge in commodity prices, by hiking bank reserve requirements to a record 19%, - draining out 2-trillion yuan of liquidity from the Shanghai money markets since October. The PBoC has also guided the Chinese 7-year Treasury-bond yield 1% higher to 3.80% today, to discourage speculation in commodities. But with inflation running ahead at +5.1% or higher, Chinese bond yields are still mired deep in negative territory.

With the Indian central bank reluctant to push its 6.25% repo rate much higher, Beijing has few allies in its battle against soaring commodity markets. Central banks in Brazil and Chile, which could hike their lending rates a half-point higher next year. However, in order for Beijing to get the upper hand over bullish commodity traders, it must allow Chinese Treasury bond yields to climb above the inflation rate, and into positive territory. That’s something Beijing isn’t ready to gamble on.

Therefore, the only viable option left for Beijing that could hold down the cost of key raw materials, is to succumb to pressure from the Fed and US-Treasury, and allow the yuan to climb further against the US-dollar. Right now, Hong Kong based currency dealers expect the yuan to gain roughly 6% next year, hitting 6.25 /dollar in late 2011. Yet allowing the yuan to climb higher also carries huge risks, and the strategy could backfire, if traders view it as a reason to jack-up commodity prices, given China’s increased purchasing power. Beijing would also suffer a huge loss on its massive $805-billion portfolio of US T-bonds. With no good choices for the PBoC to use to thwart the “Commodity Super Cycle,” China’s citizens will have to get used to the new normal, - rapidly escalating inflation.