'History is moving pretty quickly these days, and the heroes and villains keep on changing parts.'

– Ian Fleming, Casino Royale

'An effective zero percent interest rate, as a price for hiding in a foxhole, is prohibitive.'

– Bill Gross

'I used to think if there was reincarnation, I wanted to come back as the president or the pope or a .400 baseball hitter. But now I want to come back as the bond market. You can intimidate everybody.'

– James Carville

'Don't you miss interest rates?'

– Jim Grant

'And people with obsessions, reflected Bond, were blind to danger.'

– Ian Fleming, Moonraker

2012 marked the 50th anniversary of the release of the first James Bond movie, Dr. No, which had its worldwide premiere at the London Pavilion on October 5th, 1962.

The movie was based on the book of the same name, written by Ian Fleming, a former naval intelligence officer and grandson of Robert Fleming, the Scottish financier who founded Robert Fleming & Co. Ltd. 'Flemings', as it was known, was a UK-based merchant bank which, in 1985, for reasons best known to trusted officers of the company long since departed, was the first institution willing to give a wide-eyed young man named Grant Williams a job in the financial industry.

The movie was based on the book of the same name, written by Ian Fleming, a former naval intelligence officer and grandson of Robert Fleming, the Scottish financier who founded Robert Fleming & Co. Ltd. 'Flemings', as it was known, was a UK-based merchant bank which, in 1985, for reasons best known to trusted officers of the company long since departed, was the first institution willing to give a wide-eyed young man named Grant Williams a job in the financial industry.

My love for James Bond has nothing to do with the largesse of my erstwhile employer; in fact, it wasn't until I had been in the employ of the Fleming family for a couple of years that the connection became apparent (along with the realization that Alexander Fleming, the inventor of penicillin, was a scion of the same family). My love for James Bond stems from the place inside every 8-year-old boy where he wants desperately to be a secret agent, drive fast cars, and hunt down 'baddies'. (At that stage in my development, beautiful women were the only thing about James Bond films that I thought they could do without. Hey... I was 8.)

Recently, in conjunction with the release of Skyfall, the latest Bond movie, a study was commissioned by Sky TV in commemoration of the 50th anniversary of Dr. No's release, to determine the best moment in the history of the franchise. Surprisingly, the iconic line 'Bond. James Bond', first uttered by Sean Connery as he sat at a gaming table with a cigarette hanging loosely from his lips, landed in third place with just 5.7% of the vote. The winner of the poll, and incidentally the only other piece of dialogue amongst a litany of car chases, set pieces, and explosions, came from the third Bond film, Goldfinger, which came out in 1964. The quote in question was uttered by the villain of the piece, Auric Goldfinger, in response to Connery's Bond, who, as he lay watching a laser beam slowly cut through a solid gold table toward his groin, asked what, under the circumstances, was a perfectly reasonable question:

'Do you expect me to talk?'

Goldfinger laughed and replied simply, 'No, Mr. Bond, I expect you to die.'

Now, those of you who have read my work for a while will be rolling your eyes at the mention of Goldfinger and will be bracing yourselves for yet another trip into the murky world of conspiracy theories surrounding gold bullion. But, if you've made it this far, you are about to be pleasantly surprised, because that's not where I am taking you. No, that's not where we are headed at all.

Instead, we are going to try and get real about the big picture and understand just how impossible the situation is for the world's governments and central banks and, in turn, how impossible they have decided to make it for honest, hard-working savers. We are going to look at the possibility that, in keeping with Goldfinger's expectations, the bond market may be about to get hit right between the legs by a laser beam; and if it doesn't die, exactly, then it may be about to get rather badly singed.

As I was putting the slides together this week for my presentation to the Cambridge House California Resource Investment Conference in Indian Wells, CA, on Feb 23rd (shameless plug concludes), I found myself staring at a snapshot of a world that seems so far distant from today's that it's difficult to comprehend.

That world offered investors and savers the opportunity to park their money in two-year treasuries for a return of 4.8% or, perish the thought, a one-year CD for 5.4%. At the time, CPI inflation was reported to be 2.1%. In short, if you had a nest egg and didn't want to risk it, you could simply be prudent and watch that egg grow in real terms to the tune of 2.5-3.0% per year.

Crazy, huh?

That world still existed in 2007.

In the 65-odd months that have transpired since then, the world has become an altogether different place for those fortunate enough to have any capital. The option of 'safe' investing has been willfully removed by the Federal Reserve, the ECB, the BoE, BoJ, PBoC, and SNB (to name but a few) as they have attempted to force investors to take on risk and put their capital to work instead of hoarding it out of fear of an imminent collapse. Now, the whole idea of an 'imminent collapse' can be a useful thing — just ask Hank Paulson:

(Daily Bail) ... several Congressional members have alluded to a private meeting with Paulson and Bernanke in which vague economic Armageddon was threatened if Congress did not immediately hand Hank 0 billion, with no oversight. As the political debate raged over the next 15 days, several members expressed a sense of shock over the severity of the secret warnings, while refusing to divulge the details to a concerned public. Representative Sherman of California later accidentally revealed that members were warned that Martial Law would follow if the 0 bailout plan were not approved quickly. Days later it was confirmed that the warning was delivered by Treasury Secretary Paulson. [Representative Paul] Kanjorski relates the fear about an electronic run on the banks that was apparently part of the Congressional scare tactics employed by Paulson and staff. You will notice that he says members were told that within 24 hours, the entire political structure of the United States would collapse....

In the video of Kanjorski's interview (which makes for great watching) he hits the nail on the head when he says:

'You know, we're not any geniuses in economics or finances on the Hill. We're representatives of the people.'

Uh huh...

But we're getting ahead of ourselves here. Let's stay with the bond market and that 'imminent collapse'.

However, since 2008, after Paulson's warnings about collapse scared the economically and financially challenged inhabitants of the Hill sufficiently that they handed him a 7 billion cheque made out to 'Cash', the world's central banks and governments have been on a mission to convince investors that the idea of an imminent collapse is, in fact, preposterous — the theory being that, once fear has dissipated, growth can magically begin again, organically, propelled by the sudden investment of dormant capital.

Not so fast.

The massive distortions that the various QE programs have caused in markets have broken just about every mechanism for understanding the true price of risk and, by extension, the true cost of capital; and that, ladies and gentlemen, is a problem. A BIG problem.

What am I talking about? Well let's take a look at a few bellwethers of the world's bond market and try to develop some perspective on what should be the true risk-free rate, shall we?

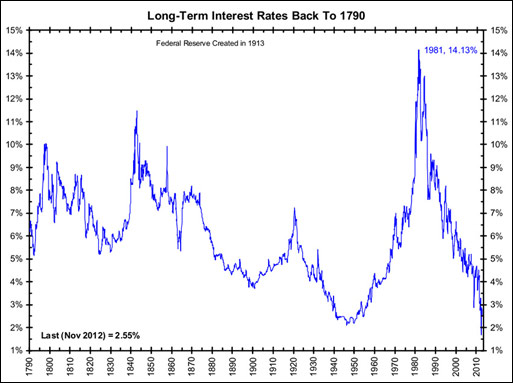

We'll begin with Exhibit A: US 30-year rates going back to before the Civil War.

As can be seen from the chart below, the USA has never — NEVER — been able to borrow long-term capital more cheaply than it can right now. In an ordinarily functioning bond market, that fact would be a fair signal that the creditworthiness of the country had never — NEVER — been better <cough>.

The second chart below shows the debt level of the United States. The US took roughly 200 years to amass a trillion dollars in IOUs and then proceeded to triple that number in a decade, double it again 12 years later, double it again in another 8 years and, overall, multiply it 16 times in a 30-year period.

Source: Bianco Research (via Big Picture)

Source: Bloomberg

It is really hard to make a case for such low rates when the USA is facing such a mountain of debt, its economy is stalling, it is essentially politically paralyzed, and ... oh, what was the other thing? ... Oh yes. The Fed will be buying about 90% of the country's new issuance in treasuries and mortgage bonds in 2013.

You have to hand it to them. US Treasuries have long been the absolute representation of the risk-free rate; and by allowing only 10% of issuance to free float, you create tremendous demand for the asset class, drive up prices, and drive down yields. Brilliant!

So brilliant in fact that it has led people who supposedly are economic and financial geniuses to say out loud some things that perhaps they ought to be keeping to themselves. Take for example the proposal this past week of Commerce Bancshares Chairman & CEO David Kemper, who, in an article entitled 'QE Cubed: A Modest Proposal for More Fed Buying. A Lot More', had this to say about the Fed's performance:

(Businessweek) The ongoing depressing news about the American fiscal situation has obscured the startling and very impressive earnings performance recently announced by the Federal Reserve. The Fed, in its usual understated way, just revealed it will be turning over billion in 2012 profits to the U.S. Treasury, a much-needed contribution that will put a sizable dent in our nation’s current trillion federal deficit.

The Fed’s earnings performance over the last several years has been exceptional. It earned more than twice Apple’s after-tax earnings last year, the result of a simple but powerful strategy: borrow money at very low rates, then buy long-term bonds.

Now, some people might question the Fed’s exceptional results and point out that it has an unfair advantage in that it has a monopoly on manufacturing the U.S. dollar. Yes, the Fed does have extraordinary profit margins, since its cost of goods sold is close to zero (basically paper, some bond traders, and access to the Internet), and yes, so far the demand for new dollars seems unlimited. Meanwhile, we as a society seem to have no stomach for trying to reduce our soaring deficit and our accelerating entitlement programs. No one in our federal government seems to be willing to work out a long-term fiscal solution. Why not go with a business model that has proven to be such a winner?

So far, so good (kinda) and, in a normal world, a very valid question: why not pick such a model? Then, Kemper gets his crazy on:

That is why I propose the Federal Open Market Committee’s next move be to take our central bank to a whole new level — a 2013 campaign that I call QE Cubed. Why not expand the Fed balance sheet exponentially, from its current trillion to trillion? Earning an extra 3 percent on another trillion in bonds would allow the Fed to return an additional 0 billion to the Treasury — thus wiping out most of our federal deficit while avoiding actually having to do anything about current government spending.

After reading this, and whilst mopping up my tea, I couldn't help but call to mind Wile E. Coyote, Super Genius.

Accidentally ejected tea cleaned up, I returned to the article, to find ... well ... this:

I’m sure some skeptics will scoff that this might be a little irresponsible.

Errr... yeah...

They may invoke memories of Weimar Germany.

Now, at this point, Kemper's article is most definitely making me think about Jonathan Swift's 18th-century satirical essay, whose title began with the same three words, "A Modest Proposal", and in which he proposed that poor Irish parents might ease their circumstances by selling their offspring as food for the rich. I read on, hoping for dear life that what I was reading was, indeed, satire:

And, oh, by the way, where is the Fed going to find trillion in acceptable bonds? I am the first to admit that the Fed will have to buy all trillion or so of our current U.S. debt, as well as most of our agency and some corporate debt, in order to reach an additional trillion. But we can make this happen!

At this point, Kemper outlines what he calls 'The Plan' — a proposal which is to modesty as Lady Gaga is to demureness. I won't recap it for you, in case my name accidentally gets attached to it in a freak cut-and-paste accident, but if you're interested in getting to the bottom of this, you can read it for yourself HERE. To the sound of approaching sirens, Kemper wraps things up in words that I can only assume were intended to amuse, but that may land in some brains somewhere between the synapses for 'frightening' and 'Barrossian':

Would trillion in extra buying power be inflationary when our entire current GDP is only about trillion? Maybe, maybe not — but we need a game-changer here. First let’s celebrate the Fed’s record profits and its contribution to reducing our deficit. Then let’s seize the moment to do something truly grand: eliminate that stubborn deficit. We have the tools, and I, for one, say let’s give it a try.

No, David, we'd better not.

Now, giving the benefit of the doubt to Kemper would have been far easier in different times; but in today's QE-addled world, sometimes crazy-sounding is just plain crazy. I have a feeling that, one way or another, we shall discover in coming days whether Kemper was being satirical or is just disconnected from reality. Personally, I can't foresee him admitting to the latter. Either way, the fact that there could be any doubt whatsoever about the thinking behind this article tells me how far down the rabbit hole we have ventured.

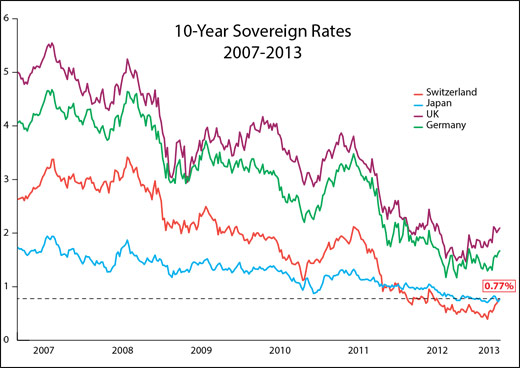

Source: Bloomberg

The chart above further highlights the problem the bond market faces. It shows the yields for 10-year debt in the UK, Germany, Japan, and Switzerland. To clarify things a little more, let's take a look at the returns an investor with million equivalent in local currency could expect to receive today and compare them to returns in the golden days of 2007.

Suddenly, not only does million not seem like an awful lot of money (especially to those who were expecting to retire on it and live the millionaire's life), but the theft of income that results from the coordinated ZIRP being conducted by the central banks becomes far more obvious.

A look at another phenomenon offers further proof of the confiscation of income from the prudent. The chart below shows personal interest income (red line) and personal dividend income (blue line). As can clearly be seen, the Fed has essentially appropriated 0 billion in interest income from the most conservative investors and effectively handed it to those more willing to take risk in the form of dividend income.

Your government at work, folks.

Source: BEA

Until now, investors heavily weighted towards bonds have seen their investments reap significant capital gains as the asset class has soared, thanks in large part to government bids via the various forms of QE, the fear generated by Europe's on-again-off-again meltdown, and recycling of euros bought in massive quantities by the SNB to defend its pegging of the Swiss franc. But on January 7th, 2013, something happened that will have enormous ramifications for bond markets. Fittingly, it came in the form of a European politician opening his mouth.

This time, it was the turn of José Manuel Barosso, the man whom Nigel Farage described in 2012 as 'a deluded, communist idiot', to throw things for a loop when, against a backdrop of protests on the streets of Madrid, he proclaimed victory (when will they ever learn?):

(UK Guardian) The euro has been saved and the euro crisis is a thing of the past, European commission president José Manuel Barroso has declared.

'I think we can say that the existential threat against the euro has essentially been overcome,' Barroso said in Lisbon. 'In 2013 the question won't be if the euro will, or will not, implode,' he said.

So let's indulge Mr. Barroso, shall we, and assume that the euro crisis is over and there is no more need to be fearful?

So let's indulge Mr. Barroso, shall we, and assume that the euro crisis is over and there is no more need to be fearful?

Let's ignore for a moment the 11.8% unemployment across the euro region, the faltering growth in its supposedly strongest economy, and the bribery scandal in Spain that has reached to the prime minister himself.

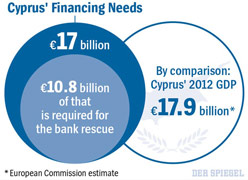

Let's also forget about the existence of a further scandal in Italy that threatens to engulf both the Super Mario Brothers, Draghi and Monti; the tug of war over a potential bailout for Russian oligarchs through Cyprus — a country with a 2011 GDP of €17.9 billion, which somehow now needs bailing out to the tune of €17 billion (see graphic above); and the UK's possible referendum on whether to stay in the EU. Greece? Sooo 2012.

Yes, let's put all that aside and take Mr. Barroso at his word and ask the simplest of questions:

Now that everything is fixed and the crisis is behind us, who would own a 10-year German bond that pays less than 2%? Or a Japanese equivalent that pays less than 1% when the new Japanese government is guaranteeing 2% inflation? Would you lend to the US government for 5 years for an 88-basis-point return?

The answer? You would own this stuff only if you were another government engaged in a currency war or in propping up your own debt. If you are a fiduciary of private money or an investor in your own right, then bonds are, for the most part, a nonsensical place to be.

I have for some time now been banging the drum about the perils of confidence returning.

Last week Bank of America took up the baton in a report warning of something called a 'bond crash':

(UK Daily Telegraph) The return of confidence and healthy growth in the US risks setting off a 'bond crash' comparable to 1994 and triggering a string of upsets across the world, Bank of America has warned.

The US lender said investors face a treacherous moment as central banks start fretting about inflation and shift gears, threatening a surge in bond yields.

This happened in 1994 under Federal Reserve chief Alan Greenspan when yields on US 30-year Treasuries jumped 240 basis points over a nine-month span, setting off a 'savage reversal of fortune in leveraged areas of fixed income markets'.

A similar shock this year is 'likely' if the US economy continues to gather strength. 'The moment we hear the first rhetorical talk of exit strategies by central banks, this could turn,' said chief investment strategist, Michael Hartnett. There was already a whiff of this in the most recent Fed minutes.

Forget the central bank exit strategies, folks. This is not something that will wait for them to dictate terms. Why does everybody think we will never again be subject to 'market forces'? Confident markets do not lend money to insolvent governments at these rates of interest. Period. Throw in the enormous capital gains that bond portfolios have made — and therefore will look to protect — and you have a recipe for disaster.

It has already started. Quietly.

Talk of a 'great rotation' out of bonds and into equities is growing louder, as stock indices have come flying out of the gate in 2013. Simultaneously, since Mr. Barroso's 'victory speech', a rather interesting move has taken place in the bond markets, as the chart below demonstrates.

Source: Bloomberg

Now, we are not talking big numbers here, but the quantum of the moves is interesting. German 5-year yields have more than doubled since the beginning of December, French yields have done likewise, and US rates are up by a third. January is going to be the first month in quite some time when portfolio valuations are going to saddle investors with a capital loss. It isn't going to help that those same investors will be reading about the 'great rotation' into stocks and how impressively equities are performing thus far in 2013. Some of those stocks even pay dividends! Go figure.

Source: Bloomberg

Bank of America again:

Bank of America said the 'Great Rotation' under way from bonds into equities closely tracks the pattern of 1994, with bank stocks leading the way.

Over the past seven years US investors have pulled 0bn from US equity funds and poured 0bn instead into bond funds. This process is going into reverse. Equity funds have drawn bn over the last 13 trading days alone, creating the risk of an unstable 'melt-up' in stocks over coming months.

The Bank for International Settlements has issued an alert on the high-yield 'junk’ bonds and mortgage debt, currently trading at record lows. The Swiss-based watchdog said parts of the credit market credit are 'highly valued in a historical context relative to indicators of their riskiness.'

It will come as no surprise to regular readers that I am very much in Bill Fleckenstein's camp: the 'deflation scare' (if that is what it ever really was) is done. Over. And that means trouble.

True deflationary scares are few and far between. The US has had four significant periods of deflation in the last 200 years, three of which occurred between 1818 and 1896. In each case, they were followed by significant periods of inflation as the remedy applied (inflationary measures) took hold. The last such period was the Great Depression (fear of a repeat of which has dictated policy response for the last four and a half years and counting) and, as the chart below shows, from that day onwards it's been inflation all the way, baby!

Source: Wikipedia

We are not out of the woods yet, not by a long way. Europe faces so many crosswinds, headwinds, and downdrafts that it's really is just a matter of time; and that will send investors panicking into sovereign bonds again and cause equities to hit air pockets, which in turn will cause the odd short, sharp fall; but with each renewed outbreak of panic, the circle of bonds that will be deemed 'safe' is going to contract.

Currently, there are only 12 countries ranked AAA by all three major ratings agencies; and of those, four are currently on negative watch by two of the three — which leaves only eight supposedly pristine sovereign credits in the world, none of which is big enough to absorb major inflows (table, below).

With each new panic, another country drops off the list of 'safe' havens. (Finally, it seems, France's dire economic situation is being taken seriously, and it is edging ever closer to the periphery of Europe where it belongs, regardless of its size.) This shrinking pool of 'good' collateral is going to become a major issue.

Last week, a hilarious exchange highlighted just how desperate things are in La Belle France:

(UK Daily Telegraph) France's labour minister sent the country into a state of shock on Monday after he described the nation as 'totally bankrupt'.

Michel Sapin made the gaffe in a radio interview, which left French President Francois Hollande battling to undo the potential reputational damage.

'There is a state but it is a totally bankrupt state,' Mr Sapin said. 'That is why we had to put a deficit reduction plan in place, and nothing should make us turn away from that objective.'

This was amusing enough, but the real kicker came with the frantic response from an altogether expected source:

Pierre Moscovici, the finance minister, said the comments by Mr Sapin were 'inappropriate'.

He added: 'France is a really solvent country. France is a really credible country, France is a country that is starting to recover.'

Until I read this, I was unaware that there were degrees of solvency. I had always assumed that either (a) you could pay your bills or (b) you couldn't, in which case you weren't solvent.

It's good to know that France is, in fact, really solvent — as well as really credible.

With such small things do we begin to see the truth emerge.

Anyway, it's about time for me to wrap this up for another week, so let's get back to where our hero, James Bond, 007, lies strapped to the solid gold table with the laser beam slowly advancing towards his classified documents.

Anyway, it's about time for me to wrap this up for another week, so let's get back to where our hero, James Bond, 007, lies strapped to the solid gold table with the laser beam slowly advancing towards his classified documents.

Goldfinger is about to leave the room (and Bond to his fate), when a slightly desperate looking 007 makes one last attempt to avoid a nasty end by resorting to the final option available to any self-respecting secret agent: he starts lying:

Bond: 'You're forgetting one thing. If I fail to report, 008 replaces me.'

Goldfinger: 'I trust he will be more successful.'

Bond: 'Well, he knows what I know.'

Goldfinger: 'You know nothing, Mr. Bond.'

Bond: 'Operation Grand Slam, for instance...'

Goldfinger: 'Two words you may have overheard which cannot possibly have any significance to you or anyone in your organization.'

Bond: 'Can you afford to take that chance?'

Goldfinger decided he couldn't afford to take that chance, and the laser beam was turned off. Sadly for the arch-villain, he should have killed 007 when he had the opportunity. Goldfinger's failure to take drastic action when he had Bond at his mercy meant that he lost everything when Bond ultimately sent the complacent bad guy plummeting to his doom....

But that was all just a movie. It's not as though life ever imitates art, now, does it?

*******

Before I disappear, there are a couple of quick pieces of housekeeping:

Firstly, a quick reminder that I will be speaking at the Cambridge House California Resource Investment Conference in Indian Wells, CA, on February 23/24th. The line-up this year is fantastic: Rick Rule, Greg Weldon, Frank Holmes, and Peter Schiff will all be in attendance, along with my great friends Al Korelin and John Mauldin. So if you are in the vicinity and would like to drop by and hear from any of these fine speakers, you can find all the details at the conference's website, HERE.

I hope to meet some of you there.

Secondly, I will not darken your inboxes next week, but I hope to return in a fortnight.