In my experience, markets don’t deal well with several crises emerging at the one time. Give them just QE tapering and they may be able to adapt, but throw Syria and an Asian currency mess into the mix, and it can make for a wild ride. Underlying all of the recent volatility though is the first sign that investors are starting to doubt the omnipresent powers of central bankers. Ben Bernanke says there can be QE tapering without rising interest rates and bond markets revolt against that idea. Similarly, the new Bank of England chief Mark Carney says interest rates will remain low for the next three years and bond yields jump given better economic data and rising inflation.

This is important because the mother of all bubbles in the modern era hasn’t been in subprime, bonds or emerging markets. No, the biggest bubble has been in central banking. It’s been a bubble based on faith in central bankers to provide cheap money to smooth out business cycles and prevent serious economic downturns. That faith has been unwavering despite the 2008 crisis and the tepid recovery since. Until now.

[Read more: Be Prepared for Major Turbulence in 2014]

What does this mean for markets? Recent events may prove a prelude to the ultimate endgame: investors realizing that unwinding the extraordinary post-crisis policies will be messy, which gets priced into higher bond yields and exposes the vastly over-indebted developed world and some of the hot money reliant developing countries. I doubt this endgame is imminent though and oversold bond and emerging markets may be due for a bounce. The likes of India and Indonesia will be hoping that time is on their side so they can push through badly needed reforms which will them less exposed to a further crisis down the road.

Welcome Back Volatility

What is it with summer holidays (for much of the world) and market turmoil? It seems like someone’s bad joke to give investors a headache while they’re trying to get some down-time.

Anyhow, markets are digesting a lot of actual and probable events right now. They’re looking at possible QE tapering, volatile bond markets, the potential for US intervention in Syria, the coming announcement of a new U.S. Fed Chairman and crumbling Asian currencies. Receiving less attention are a big German election this month and another soon-to-announced bailout package for Greece. That’s not to mention that China and Japan have quietened down of late, though if they don’t announce serious economic reforms soon, they’ll be back in the spotlight. And you can throw in September traditionally being a terrible month for stock markets.

The simple and logical explanation for much of the volatility stems from Ben Bernanke’s statement in May signalling a potential pullback from QE. Of course, QE – aka money printing - has been used to buy bonds and thereby suppress yields. The purpose of this has been to keep interest rates below the GDP rate, thereby reducing America’s large debt to GDP ratio, now at 105%. Also, QE has aimed to get investors to part with their cash, by offering pitiful rates, and to put that cash into risk assets such as stocks. With rising stock markets, this would induce the so-called wealth effect where people feel wealthier and start to spend again, which boosts GDP. So goes the theory anyway.

Unsurprisingly, Bernanke’s announcement resulted in bond investors heading for the exit doors. After all, QE had helped keep bond yields low and any cutbacks would mean less demand and higher yields. Subsequently, U.S. 10-year Treasury yields went from close to 1.6% in May to the current 2.78%. For bond markets, that’s a bloodbath.

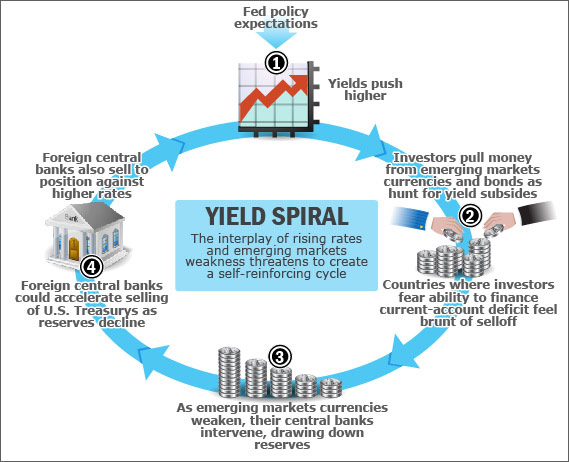

The spike in U.S. and developed market bond yields made emerging market currencies and bonds less attractive. Since 2009, emerging markets have benefited from a flood of money seeking higher yields in currencies and bonds compared with developed markets which were offering next-to-nothing yields.

The prospect of QE tapering turned this on its head. And the emerging market countries to suffer the most have been those such as India and Indonesia where investors have doubts about their ability to finance large current-account deficits. In effect, a current-account deficit means you’re investing more than you’re saving. And you rely on external money to finance the gap. Once that money starts to dry up, currencies get hit.

[Hear More: Martin Armstrong: The US Is the Beneficiary of Foreign Crises - Follow the Capital Flows]

In India and Indonesia, the currencies have been obliterated. That’s led to central bank intervention which has drawn down on foreign exchange (forex) reserves. In effect, this action tightens domestic money supply. Tightening is not what these countries need given both have softening economies.

There are also fears that the drawdown in forex reserves in emerging markets will produce a “negative feedback loop” for developed markets. That is, these reserves have primarily gone into large, liquid markets such as the U.S. bond market. A reduction in reserves means less demand for these bonds and possibly higher yields.

The graph below from MarketWatch illustrates this negative feedback loop.

Central Bankers Tamed

What’s fascinating about recent events though, and has been little mentioned, is that investor confidence in the words of central bankers appears to be waning.

In May, Bernanke indicated the QE tapering was on the cards. When bond yields jumped soon after, leaks to the press tried to downplay the impact of tapering on interest rates. In other words, the Fed was at pains to emphasize that QE tapering did not automatically mean higher interest rates. Investors didn’t get the memo and yields spiked further.

Similarly, Britain’s new central bank chief Mark Carney pledged to keep policy loose and rates low, but investors all but ignored him. Earlier this month, Carney said he’d keep benchmark interest rates at a record low of 0.5% until unemployment in the U.K. falls to 7% – a threshold not expected to be reached until 2016. But with the economy and inflation picking up, investors have already factored in a rise in rates in 2015, a year prior. The worry is, of course, that these market expectations will feed through to higher mortgage rates before then.

These events could prove a significant turning point. Up until now, investors have treated the words of central bankers as gospel. Since 2009, these bankers have pledged massive stimulus and low rates. Investors have taken their word and parted with cash to pile into stock and bond markets. What the central bankers wanted, they got. This explains why the correlation between stimulus and the S&P 500 is more than 90%, for instance.

Now it seems that investors are getting more skeptical of central bank pledges. It’s not before time!

But it’s important to understand the ramifications of this. The developed world desperately need bond yields to remain low. As I’ve argued in a previous post, higher interest rates would cripple many over-indebted developed countries.

For example, if interest rates in the U.S. normalize and increase by 100 basis points annually over the next five years, the interest expense on government debt would rise from US0 billion last year to US.51 trillion. To put this in context, U.S. government cutbacks earlier this year, which some worried would tip the economy into recession, totaled just US billion. The upshot is that normalizing interest rates would result in massive cutbacks in U.S. government programs.

[Listen: Barry Bannister: The Biggest Risk to the Economy Is Government Policy, Not Fundamentals]

Elsewhere, higher interest rates would be even more brutal. The Bank of International Settlements estimates that if bond yields were to rise just 300 basis points across the yield spectrum, the losses for holders of debt in France, Japan, Italy and the U.K. would range from 15% to 35% of GDP.

I repeat: the developed world can’t afford higher interest rates. The problem is that though central banks control short-term rates, the market controls long-term rates. Once investors start to lose faith in the ability of central bankers to manage an exit from the extraordinary policies of recent years, much higher interest rates will be on the cards. It’s only then that the ugly implications of these policies, which has led to even greater debt in developed countries than prior to the crisis, will come to light.

And recent events also show, a number of developing countries, particularly in Asia, would also suffer from higher interest rates. Inevitably, like now, those countries with large current account deficits would be hit hardest.

A Wake-up Call for Asia

Which brings us to the plights of India and Indonesia. While recent currency turmoil hasn’t entirely surprised, the speed and ferocity of it has. There’s little doubt that they’ve both been large beneficiaries of lavish QE and now victims thereof. But equally, they’ve been targeted for good reason.

According to the IMF, India’s current-account deficit is likely to be 5% this year, compared with 2.8% from 2008-2011. Similarly, Indonesia’s current-account deficit will reach 3% this year after an average surplus of 0.7% from 2008-2011.

As alluded to earlier, current-account deficits essentially mean you’re investing more than you’re saving. The only way to keep this up is to borrow surplus savings from abroad. Or put another way, you’re borrowing money to finance growth.

QE tapering is leading to expectations of higher interest rates in the developed world. Money which had been flowing into Asia in search of yield is now heading back to the West. And that makes the ability to finance current-account deficits more difficult.

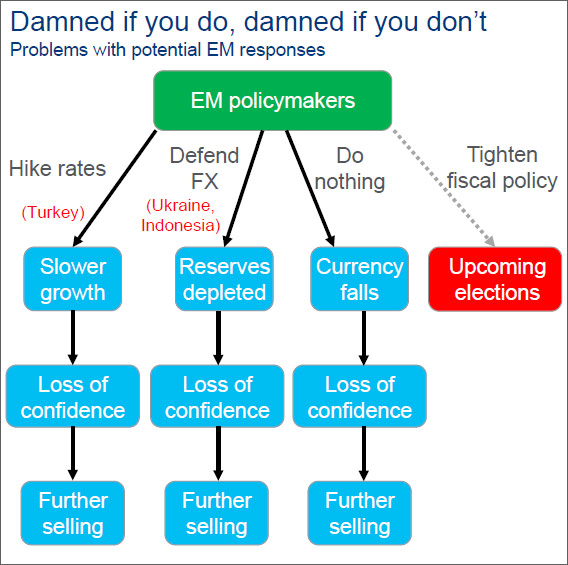

India and Indonesia are certainly in a bind. If they hike interest rates, that will slow their economies, leading to another drop in international confidence and further money outflows. If they defend their currencies against further falls, forex reserves will decline, eroding confidence and resulting in accelerating outflows. Do nothing and their currencies are likely to fall further.

The elephant in the room is that both countries have elections next year. This makes raising interest rates a politically undesirable option. Though as Indonesia has shown with its recent rate hikes, there may not be a choice in the matter. The diagram from Citi below illustrates the quandary in which India and Indonesia find themselves.

Both countries better prayer that higher interest rates in the developed world don’t become a reality. More seriously, they need to rectify the issues which have led to their growing current-account deficits, and quickly. Both actually have similar problems which need addressing, namely:

Cutting fuel and other subsidies. Indonesia has made some progress on this front while India hasn’t. It goes a long way to explaining some of the entrenched inflation issues in both countries. I get that it’s politically sensitive particularly when you’d rather bribe voters with subsidies in an election year. But it needs to be done, and soon.

Reducing bureaucracy. There’s a reason that Indonesia and India are ranked 128 and 132 out of 185 economies for doing business, according to the World Bank.

Tackling corruption once and for all. The current Indonesian President promised to crack down on corruption but has had little success. Indian corruption hasn’t gotten any better despite endless political scandals. It’s a huge issue holding both economies back.

Welcome foreign investment. It’s amazing how unwelcoming both countries are to foreign investment. When I was a portfolio manager, I used to deal with the maddening situation of many Indian companies capping foreign ownership in their stocks. I had to ask permission from the company whether there was room for our fund to buy stock. Indonesia isn’t much better, as the continued imposition of regulations and taxes on foreign mining companies with operations in the country attests.

These are but a few examples of what India and Indonesia need to do to rebalance their economies. Hopefully, this crisis acts as a catalyst for reform.

What It Means for Markets

What does all of this mean for markets then? If I’m right and the world can’t afford higher interest rates, that’ll mean central banks will fight to keep rates low by printing more and more money. Whether a small cut to QE happens this month or not, a rather quick reversal shouldn’t be ruled out. And other countries will print away regardless.

In this environment, oversold bond and gold markets may outperform, as they’ve been done for the past few weeks. Stocks may rebound at some point but should lag other assets, given their relative outperformance in the months prior.

[Listen: John Doody: I'm Sticking to My Guns - $2,000 Gold by Year End]

Regular readers will know that my preference is to invest for the long term ie. 3-5 years. On this basis, I still prefer overweights in gold and cash versus stocks and bonds. With yields low, bonds guarantee low-to-negative real returns. Stocks are more attractive than bonds, particularly in Asia where valuations are reasonable compared with the likes of the U.S.. But the view here remains that the bear market in stocks which began in 2000 hasn’t finished and consequently valuations can potentially go a lot lower from here.

Gold is attractive as a hedge against further money printing and currency debasement. Meanwhile cash is the ultimate contrarian play! Everybody hates it. But it’s likely to come in handy if risk assets get beaten up at some point - which is the base case here. In terms of currencies, the Singapore dollar, Thai baht (especially after recent tumult) and U.S. dollar are favored. The dollar is a flawed currency but should be a beneficiary of an eventual flight to safety. At least, initially.

Source: Asia Conf.