"By a continuing process of inflation, government can confiscate, secretly and unobserved, an important part of the wealth of their citizens."

~John Maynard Keynes

This year will mark my 32nd year in the business. I began my career in 1980 after spending several years in corporate life, which I did not find to my liking. I had too much of an independent streak and eventually came to the realization that I'd be much better off starting my own business. When I entered the financial world interest rates were beginning to peak, as the long upward climb in inflation was coming to an end under the leadership of Paul Volker at the Fed. It is hard to believe today that interest rates on treasuries were as high as 15.7%. The yields on money market funds were over 18%. Inflation rates were over 14%, with oil prices at $40 a barrel. Gold and silver would eventually peak at $850 and $50 an ounce, respectively.

Where the Debt Supercycle Begins

I spent my first decade in the business as a broker before transforming my business to a fee-based money management firm. All I sold in the 1980's was fixed income. Who wanted to invest in stocks when you could get double-digit returns in guaranteed deposits at a bank or by investing in government debt? I still remember one of my first trades—a 10-year treasury note paying a 15% interest rate.

What I did not realize at the time was the U.S., and the western world in general, was about to embark on what we now refer to as the "Debt Supercycle"—a theory articulated by the investment strategists at Bank Credit Analyst out of Canada. The Debt Supercycle is a description of the long-term decline in U.S. balance sheet liquidity and the rise in indebtedness during the WWII period. Economic expansions in the post-WWII world were associated with the buildup in debt as Western governments introduced automatic stabilizers through entitlements such as unemployment benefits, Social Security, Medicare, and deposit insurance at financial institutions. During the early stages of debt buildup, government policies were successful in preventing the frequent trends toward depressions that plagued the pre-WWII economy. Western economies would experience periodic corrections during recessions, but these recessions did not reverse the long-term trend of debt buildup that continued to grow with each successive decade.

These trends would lead to growing illiquidity, making our financial markets more fragile and susceptible to the threat of a deflationary event like we experienced recently in the great credit crisis of 2008–2009. These periodic recessions were fought by governments with more deficit spending and credit creation. Thus, the bigger balance sheet excesses became, the more painful the eventual corrective process became as well. The financial stakes became higher in each new economic cycle, putting ever-increasing pressure on governments to reflate demand, by whatever means were available.

According to the Bank Credit Analyst, the Debt Supercycle reached an important inflection point in the recent economic meltdown of 2008–2009. Authorities reached the limit of their ability to get consumers to take on more credit. The result was that governments were forced to leverage up instead. This is where we are today: authorities spend, borrow, and print money to fight off the deflationary impact of private sector deleveraging. Welcome to the final chapter of the Debt Supercycle—a period of trillion-dollar deficits that are being monetized by trillion-dollar expansions of central bank balance sheets, otherwise known as money printing. Once fiscal policy is pushed to the limits of sustainability, the Debt Supercycle will come to a violent end. This is exactly what is happening to Europe now.

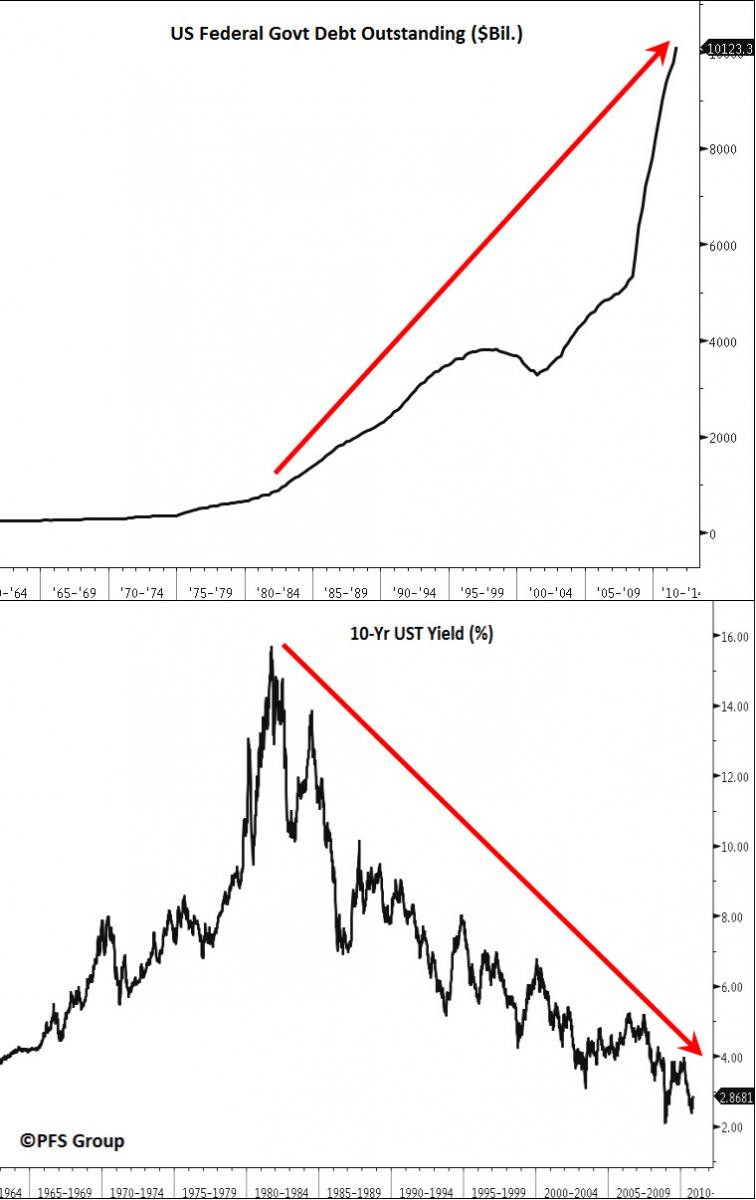

A graphic depiction of this Debt Supercycle can be seen below. As of this writing, outstanding U.S. federal debt is close to $15.3 trillion dollars. For the first time in my lifetime US federal debt now exceeds U.S. GDP. In personal terms each U.S. citizen now owes $180,559.1

Our politicians have been acting irresponsibly, paying only lip service to the nation's rapidly growing debt burden. It has been argued that our debt is not as bad as it appears and we have plenty of options and time to resolve this issue. Some argue for higher taxes, others for dramatic spending cuts. The truth is that neither will work alone. There aren't enough taxpayers to pay the bill, even if we raise tax rates to 100% on "the rich". Spending cuts will also not solve our problems unless we eliminate all forms of entitlements and drastically reduce the size of our military. In the end, our only option will be to pursue a combination of tax increases, entitlement and spending reductions, and a steady dose of inflation. This is the policy we pursued after WWII and it is now the official policy of the U.S. government, a policy referred to as "financial repression".

"I do not think it is an exaggeration to say history is largely a history of inflation, usually inflations engineered by governments for the gain of governments."

~Friedrich August von Hayek

I would like to address the unusual phenomenon of the Debt Supercycle and why it has gone on for well over three decades without a major crisis until recently. Politicians, and the Keynesian economists who support them, have long argued that debt imbalances don't matter. What matters is the economy's ability to grow and it is government's job to make sure it grows through whatever means necessary. On the surface this argument seems plausible. The two graphs below illustrate the popularity of this view.

Source: Bloomberg

From 1978 to today, the U.S was able to grow its total debt from 9 billion to trillion, an annualized growth rate of 13.7%.2 While U.S. debt was growing during this period of time, the interest rate paid on that debt steadily declined. This confounded experts who would have predicted higher rates of inflation and certainly higher rates of interest. This can be explained. At the end of the 1970s, inflation rates were hovering over 14%, bond yields on U.S. treasuries had risen to over 15%. The U.S. Government had been financing its growing deficits by urging the Fed to monetize its debt by printing money to buy U.S. treasuries. This is what led to the rising inflation rates during the 1970s. This philosophy came to an end with President Carter's appointment of Paul Volcker to head up the Federal Reserve.

From Printing Presses to the Bond Market

Volcker and other central bankers convinced their respective governments that they could tame the inflation monster by financing deficits through the bond market rather than the current practice of monetizing (printing money to pay off) the debt. Stung by a wave of rising inflation, governments turned to their central banks for advice. The advice given had three components: one, raise short-term interest rates in order to restrain bank borrowing by individuals and businesses; two, cut government borrowing; and three, use the bond market to finance budget deficits by selling bonds to domestic and overseas investors.

It was argued, and rightly so, that when a government taps the bond market it is drawing from the existing stock of savings—no new money is created. Large institutions such as insurance companies, pension funds, mutual funds, and individual investors would supply the necessary capital to finance government deficits. The inducement to supply this capital was high real interest rates, an interest rate that was well above the inflation rate. It worked. The migration of credit expansion from within the monetary sector to outside it was the single biggest reason why OECD government inflation fell below five percent throughout the '80s, '90s, and the 2000s. As shown in the graphs above, it led to rising debt levels and falling interest rates.

Another process that occurred during this period that facilitated government debt financing was the revolution that was occurring in the capital markets. Peter Warburton described this process in his seminal work "Debt and Delusion," from which I now quote:

The capital markets' revolution of the late 1980's and the 1990's was facilitated by several parallel developments, of which five stand out. First, the incapacity of the banks, due to non-performing loans; second, the adoption of liberal credit policies by governments; third, the displacement of discretionary consumer borrowing by obligatory government borrowing (to finance budget deficits); fourth, the concentration of management of private wealth in the hands of large funds; and fifth, the increased use and acceptance of financial derivatives….

If this powerful shift from traditional bank borrowing towards the capital markets in North America and Western Europe had not taken place, it is most probable that there would have been a much longer period of recession and consolidation in the aftermath of the late 1980's property bust….

Deprived of the easy option of selling bonds to investment funds and individuals, the government would probably have resorted to greater monetization of their borrowing….

If this traditional course of action had been followed, then there is little doubt that inflationary fires would have been rekindled in the western economies during the 1990's by pressing additional liquidity (cash and bank deposits) into the hands of consumers and firms, the demand for goods, services and assets would have increased relative to their available supplies. After a couple of years or so, the outcome of excessive money creation would have been a resurgence of consumer price inflation, following the pattern of the 1970's and early 1980's.

This process worked for an extended period of time with occasional hiccups and financial failures: the bankruptcy of Orange County, the Mexican peso crisis in late 1994, the collapse of Barings Bank in 1995, the Asian currency crisis in 1997, and the Russian debt default and the bankruptcy of Long Term Capital Management in 1998.

The Rise of Derivatives

By the 1990s, a new pattern—which continues to this day—was beginning to emerge: an increasing frequency of "rogue waves" or "black swan" events.3 With the increasing role of large financial institutions as intermediaries within the financial system, a large important part of capital transfers were being done in secret through the derivatives market. Transactions between investment banks and mega-funds such as hedge funds were increasingly being transacted in secret in the OTC derivatives market far from the public gaze.

Derivatives were the ultimate leverage tool used by hedge funds and the proprietary trading desks of large banks in gearing up the financial system. The use of derivatives enabled these financial entities the ability to gain control of a larger asset portfolio with a smaller commitment of capital. Derivatives, in effect, gave artificial support to both the bond and equity markets. They also facilitated the massive leveraging of the financial system with debt-to-asset ratios rising from 12-1 to 40-1 by the time of the 2008 financial crisis. Most importantly, the synthetic support given the bond and equity markets by these leveraged instruments were critically dependent on the downward progression of interest rates and the shape of the yield curve. A small tremor in the structure of interest rates would undermine the profitability of these leveraged trades leading to forced selling in the bond, equity, and commodity markets, which explains much of what happened during 2007–2009.

Risk On/Risk Off and the "Paranormal" Market

The fact remains that our financial system is still highly leveraged. As Bill Gross recently wrote in his 2012 Investment Outlook, "Towards the Paranormal": "most developed economies have not, in fact, delevered since 2008…credit as a whole remains resilient or at least static because of a multitude of quantitative easings (QE) in the U.S., U.K., and Japan...and now Euroland countries."4

Because interest rates are now zero-bound, according to Gross, it raises the possibility of a fat left-tailed possibility of unforeseen delevering or the fat right-tailed possibility of central bank inflationary expansion. The result is we face a number of years in the future where economies will exhibit different aspects of the New Normal which Gross describes as "Sub," "Ab," or "Paranormal" (to be explained below).5

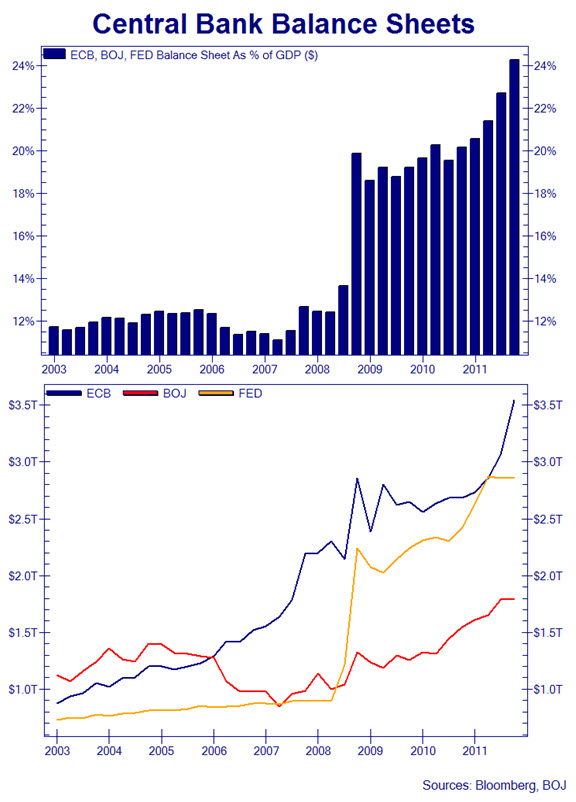

The global financial system is still leveraging up. However, this time it is governments that are doing the leveraging. Today, sovereign debt is being issued in copious quantities. The vast majority of this debt is being used to finance non-productive consumption. All of the world's major governments are spending and living well beyond their means leaving central banks to return once again towards aggressive debt monetization to desperately ensure interest rates remain subdued and the financial system abundantly liquid. As Grant Williams explained with the following image below, "currently the central banks of the top three developed world entities: the Eurozone, the US and Japan have balance sheets that amount to roughly trillion...What does this mean? It means that nearly trillion in world economic growth is artificial and exists only courtesy of central bank intervention...It also means that central banks will never unwind their 'assets'...It also means that in this age of ongoing consumer and corporate deleveraging, central banks will have no choice but to continue monetizing."

Source: Grant Williams, "Things That Make You Go Hmmm..."

This creates an unstable dynamic whereby market participants focus their attention on divining opaque and unpredictable moves by "the powers that be" rather than the real and economic value of various assets. This anticipation by highly leveraged financial players of policy reflation is what underpins the highly speculative nature of our current global marketplace. When reflationary policies are delayed or not forthcoming, the markets deleverage and go into "risk off" mode. This drives the dollar higher and treasury yields lower. When the monetary bazookas are unleashed the "risk on" trade is executed and stocks and commodities rise universally. This "risk on/risk off " trade is now part of the new Paranormal that Gross describes in his 2012 Investment Outlook.

When Markets Rebel

The question as to which fat-tail risk (left or right) the markets experience boils down to a game of confidence that governments and their respective central banks are playing with the bond markets. The risk to government is that because of zero-bound interest rates, governments have been financing a good portion of their debt short-term. The rate of interest is low which helps to reduce deficits. The danger is that since a good majority of debt is short-term it will have to be rolled over. As long as confidence is maintained, debt will continue to roll over at existing low interest rates. The real danger is when the markets lose confidence in policymakers. That is: if the markets rebel and demand higher rates of return. It is a rise in interest rates which now directly threatens the solvency of many governments. Record debt levels are not a burden to government as long as interest rates remain low. It is when confidence is lost and rates rise that the solvency issue comes into question. This is the nightmare scenario that keeps central bankers up at night; a warning Sidney Homer wrote in his "A History of Interest Rates":

Many besides the government have been encouraged to borrow at short who in an earlier age would have borrowed at long term just to be sure the funds would be available if needed. The dangers of this procedure became sadly evident in the 1970's, when certain borrowers, such as Penn Central and New York City, suddenly found the refunding market closed to them.6

Summary

We now live in a new era of uncertainty—Pimco's new "paranormal," if you will. Our financial system continues to leverage up as governments replace the private sector in gearing up their balance sheets. Central banks are now embarked on a policy of reflation, monetizing a major portion of rising government deficits. The ECB's balance sheet expanded by 7B (euro 727B), or 36% last year, to a record .5T. The Fed expanded its balance sheet by 3B to .92T, an increase of 21%.

We are now at a state where the sovereign bond market has grown to become the largest financial bubble in history; a bubble that could succumb to three potential market shocks. The first type of shock would come from a spike in commodity prices triggered by additional rounds of quantitative easing. It could be as simple as an "act of God" such as an earthquake, tsunami, or the failure of an important agricultural crop. The bond market would react in fear that higher commodity prices would be absorbed in the price of goods and services via loose monetary policy.

A second shock could be triggered as a result of political instability and loss of confidence in government policy. An example is what is occurring right now in Europe regarding an attempt toward a fiscal union or the debt ceiling debate in the U.S. The bond market would view negatively a failure by governments to rein in spending and control their deficits.

The third shock would emanate from a potential default or restructuring of a sovereign debt that would lead to a domino effect in the banking system. A large international bank or group of banks might not be able to meet their obligations which would lead to a rise in fear of uninsurable losses among the banks or their counterparties.

As the bond market continues to expand through sovereign debt expansion and central bank monetization, it is moving further away from reality as a result of speculative activity. This makes sovereign debt extremely sensitive to any unanticipated event. The probability of another black swan or rogue wave is beginning to multiply—from a failed bond auction, to larger than expected deficits, to political rancor over spending cuts. Sovereign debt can no longer be looked upon as a risk-free asset. For the reasons cited above I continue to avoid U.S. treasury debt as the rates of return bear no resemblance to reality or are commensurate with the risk they entail. Caveat emptor!

[1] https://www.usdebtclock.org

[2] Federal Reserve Flow of funds Account, Q3 2011, p.9

[3] Debt & Delusion: Central bank follies that threaten economic disaster., by Peter Warburton, p.12-14

[4] Towards the Paranormal, Bill Gross, January 2012, p.1

[5] Ibid, p.4

[6] A History of Interest Rates, by Sidney Homer and Richard Sylla, 3rd edition, p.333