How it began

This yarn (Aussie for story or tale) about Australia's housing bubble, arguably of even greater proportions than the US and UK bubbles is largely the story of one man, my old mate (Australian vernacular for buddy) John Symond.

I met up with Symond at the 1978 Victorian Racing Club's fabled Melbourne Cup Carnival, an historic event in the Australian horse racing calendar centered around the historic 3200m Melbourne Cup, always run on the first Tuesday in November which is Spring in the Land Down Under. Symond was then running a boutique finance business out of Sydney specializing in structured finance for the purchase of Thoroughbred racehorses and breeding stock and was attending the carnival to meet with existing clients and scoop up some new ones.

I was there to see my Champion race filly Scomeld make her bid for glory in the Group I VRC Oaks over 2500m, the country's premiere event for 3 year old fillies (females) held on the 3rd day of the carnival. Scomeld was sent out favourite for the $250,000 purse event and I had $50,000 on her with the local bookmakers to win. In those days I was running North Australian Rubber Mills Limited a public company based in Brisbane, Queensland which had the distinction of being the first company listed on the Queensland Stock Exchange. $50,000 was a lot of money in those days and was enough to buy a very nice house in one of Brisbane's better areas, so whilst I wasn't betting the house on my filly, I was at least betting a house!

Wednesday, Oaks day, dawned bright and clear with Flemington's fabled roses in full bloom. At a little after 4:30 in the afternoon, Scomeld with Australia's leading jockey Mick Dittman in the saddle stormed down the Flemington running rail to win the VRC Oaks by 3 lengths running away and enter the annals of racing history!!

Shortly after, Symond introduced me to a new client that he had in tow, John Messara, a young stockbroker from Sydney who wanted to get into the horse racing business. We retired to the Members bar (men only of course) and I shouted (Australian for bought) champagne for the bar for the rest of the afternoon. Symond and Messara in the spirit of collegiality had decent bets on Scomeld so the three Johns watched the video replay while the champagne flowed and we extolled the virtues of the mighty Scomeld. We were young, life was good and our motto was "fast horses and friendly women"!!

Little did we know what fate had in store for us.

Messara made the horse business his life and went on to found the world famous Arrowfield Stud https://www.arrowfield.com.au/ in the lush Hunter Valley, north of Sydney. Together with the Late Robert Sangster, one of nature's gentlemen and John Magnier of Ireland's Coolmore Stud and recently Manchester United fame, he instigated the now common practice of "Shuttle Stallions", the bringing of Northern Hemisphere Stallions to Australia and later New Zealand to stand the southern breeding season before "shuttling" back to their Northern Hemisphere studs. Access to these great horse's bloodlines is the most significant event in Australian horse breeding history and Messara deserves his share of the credit for this innovation.

Your humble correspondent continued his love of race horses for many years, inventing and founding QRIS, the Queensland Racing Incentive Scheme, a mathematically based marketing innovation to promote locally bred horses, since copied shamelessly around the world including several states in US, UK, Ireland, France, NZ and of course every state in Australia.

When those adventures ended the mystery of financial markets called and the great search for the elusive Danielcode began.

The third and by far the most important of the three John's present in the Member's bar at Flemington Racecourse in 1978, John Symond, reinvented himself to become a confrere of the great and the good, a familiar of Premiers (State leaders) and Prime Ministers, a mover and shaker of industry, the recipient of his country's most prestigious civic award the AM (Member of the Order of Australia) and one of the richest men in the country!!

To understand this story we need to go back to pre 1990. Australia, "The Lucky Country" has always prospered due to firstly its bountiful supply of agricultural and of recent times mineral wealth. Setbacks, such as there have been since the great depression were short and swift. I will tell you more about Australia in subsequent articles but the focus of this story is John Symond and the housing bubble. Symond's thoroughbred horse financing business came to a shuddering halt when his principal financiers the State Bank of South Australia collapsed in 1991 with debts in nominal terms of $3.1 Billion! In the aftermath, Symonds who had personal guarantees to the bank for much of his businesses financing was treated roughly. I doubt if Symond, an affable and good natured chap could fairly be said to have ever hated anyone but he certainly harbored a deep loathing and distrust of banks and bankers.

Australia, one of the most over regulated countries on earth has long held to the "Four Pillars" policy in Banking. With a strong centrist Federal Governmental system, successive Treasurers have upheld a policy that has ensured a shared quasi monopoly for just four national banks, the Commonwealth Bank previously owned by the Federal government and now privatized, Westpac, formerly the Bank of New South Wales, the National Bank formed from a merger of the old CBC and CBS Banks and Australian and New Zealand Bank (ANZ) which too arose after a number of mergers. These four giants and their predecessors dominate the Australian banking scene. There have been and are a number of smaller State banks but they are insignificant for the purposes of this story. Foreign banks have had limited access under the guise of investment banks but retail banking is the preserve almost exclusively of the Four Pillars.

Under this restrictive regime which still exist today, competition between banks was and is largely non existent. Before 1992, buying a house was a painful process as it inevitably meant a meeting with "The Bank Manager". Banks in this not so distant past made loans to house purchasers from their own funds either accrued savings and deposits or loans that the bank had on its own balance sheet. The point is that banks had an ongoing responsibility for the mortgages they wrote and they took it seriously. At the dreaded bank manager's interview the supplicant went cap in hand to ask the bank to extend them a mortgage to buy their home. Bank's usually wouldn't lend more than 60% of the purchase price and steered you to their subsidiary finance company for the next 20%. This got around the interest rate limits that banks could charge as their finance subsidiaries had no such limit. Mortgage brokers were rare and sorry creatures eking out a living on the 1% commission that some banks would pay them for introducing a client.

A typical home loan therefore finished up being a first mortgage (always principal and interest) to the bank at probably 8.5%, a second mortgage to the bank's tame finance company at 12% and you had to find the 20% or more equity while restricting the cost of the mortgages to 25% of the household income. Interest only loans were the preserve of private investors who often pooled funds under the management of an Attorney.

Before the bank would extend this largess, the applicant had to be a "good customer" with a proven credit history with that bank; produce a written valuation from a bank approved valuer who actually went out and inspected the house, and produce written evidence of your ability to pay back the loan including principal. No fairy stories here! Tax returns and pay slips together with an asset statement signed by an accountant were de rigueur!! If you couldn't prove your income and stable employment, don't apply. The manager always made the point that the bank was doing you a huge favour and expected all of your banking to be conducted with them forever. As all home mortgages in Australia are personally guaranteed by the mortgagor for their full worth (that's why they wanted that asset statement), the mortgagor entered economic serfdom.

Needham's Law Number 3: "All Asset Bubbles are caused by Structural Changes that Induce then Incentivise Misallocation of Capital"

For Australia, the seeds of the housing bubble were sown in 1985 when a capital gains tax was levied on all asset sales at the already onerous personal tax rate with one significant exception...the taxpayers' primary residence or family home was completely exempt. This created an immediate incentive to have a bigger, better home representing more of your assets (usually 100%) than had historically been prudent. We immediately saw a movement towards upgrading the family home be it by trading up, building extensions or upgrading the property as the dead hand of traditional banking kept house prices in check by simply limiting access to funding.

The powder trail was laid and awaited only a spark to ignite.

John Symond was to be that spark.

In 1992 John Symond was a man with a secret. Although we didn't know it at the time, Symond had discovered the secret of securitization! Armed with warehousing loans and credit facilities no longer under the control of the dreaded Four Pillars, Symond launched the most hated word in the Australian banking scene squarely at his erstwhile nemesis the banks...competition!!

Symond's new vehicle Aussie Home Loans https://www.aussie.com.au/ aimed its attack squarely at the traditional banks. Giant billboards began appearing depicting the hapless homeowner teetering above a bank's powerful edifice with the soon to be famous slogan "Aussie...we'll save you"! Symond became an overnight media star with his laconic but always powerful attack on the former monopoly stakeholders, the banks. Deep down all decent Australians loath and fear their bank. They were, and probably still are viewed not just as an evil necessity, but as just plain evil. This was fertile ground for Symond who delighted in rubbing that little sore patch. In Australian lingo Symond "gave it to them" with a vengeance.

Symond marshaled his troops, bright young things usually in small SUV's emblazoned with Aussie's signage and armed with mortgages that of all things offered "choice" a word absent from the lexicon until then. Moreover these kids were nice! They came to your house when it suited you, they actually wanted your business and they were knowledgeable. They knew where to find the best deals and they dealt with most of that boring, indecipherable paper work.

Imitators like Wizard Home Loans and a score of clones soon followed. Grant Fox, legendary stand-off-half for the famed New Zealand All Blacks Rugby team became a Wizard franchisee; mortgage broking had become a mainstream business. The banks began to fight back against these usurpers' encroachment on their hallowed turf of high rates and no risk but it was too late. Pandora's Box was well and truly breached and the Australian Mortgage Industry was born.

From here events take a predictable turn. With the financial stars aligned for mortgage brokers, mortgage originators, financial packagers and securitisers, valuers, conveyancers, lawyers and a horde of assorted hangers-on the US model to bubbledom was adopted. We got lo-doc and no-doc loans; no longer did you have to prove your income; you just "stated" it and paid a few points more in rate. Principal was deferred, wrapped or made into a "balloon" that was never paid as mortgages were refinanced before the new shrubs in the garden could grow more than a few feet. With almost unlimited access to funding, Aussies and Kiwis (natives of New Zealand) went on a buying binge unequalled in history. Houses had no established intrinsic worth anymore, all you had to know is that they were going up 20, 40, 60% a year so you just HAD to get into that market and buy that house right now. This indeed was the way to health, wealth and happiness.

Those of us old enough to remember previous booms were continually proven wrong.....$360K for that piece of junk I said; they"re joking!! The opening bid was 600K!!

Property developers rushed to service this bountiful market with crowded subdivisions hours from the workplace and nary a tree in sight; new apartments in resort areas were sold from glossy brochures before a sod was turned and in Melbourne and Sydney buyers stood in queues to place non refundable deposits on the latest piece of nausea being touted as "Inner City Living".

Developers became rich beyond their dreams, architects had their photos in the glossies; lawyers (who do most of the property transfers Down Under) had a new generation of sheep to shear and real estate agents who had largely morphed from washing machine and used car salesmen began to become celebrities and people of quality. The media cottoned on that life was now all about "the home" and soon our monopoly cable service (Aussie Rupert Murdoch of course) began to air such exciting and originally named shows as "Position, Position, Position" for which aged ex-models were recycled as TV presenters to ooh and aah with the ever nifty and well groomed salesperson as they speculated over the amazing amount this old banger (the house, not the presenter) would bring at its upcoming auction.

How much your house had increased in value since its purchase or latest refinance was the ONLY topic of conversation at parties and coffee houses!

The people loved it; never before had so many felt so wealthy and it's all so easy. Governments loved it too as Stamp Duty (sales tax on property contracts), and property taxes make fiscal prudence and budgeting for States a thing of the past. Some states introduce a "wealth" tax to get their grubby hands on the windfall profits being made by home owners.

Brisbane and Perth join the party as Queensland and Western Australia's huge supplies of mineral wealth suck in newcomers to service the endless demand from Asia. This is real wealth as Iron Ore from the Hammersley Ranges and Coal from North Queensland goes to feed the hungry steel mills of Asia. The economy of Western Australia surges with massive Liquid Gas fields on the North West Shelf coming on stream; The Pilbara groans as bauxite, gold, diamonds, mineral sands and zinc are torn from the earth and the never ending chant of growth, growth, growth goes on. With that growth comes people and demand for housing, and John Symond's miracle of securitisation means that the lenders no longer carry the risk of the mortgages they granted. No more are they traditional lenders who are accountable for their actions and carry the risk on their balance sheets; now they are merely originators who clip the ticket and the new owners of the mortgage are unknown and far away as these once docile packages are sliced, diced securitized, repackaged, assigned phony credit ratings, sold and resold. The only imperative now is to get into the game!

Growth, Growth, Growth

By 1994 the Paris based think tank the OECD would trumpet of Australia "House prices worlds highest"

AUSTRALIA has by far the most overvalued houses in the Western world, with prices 52 per cent higher than justified by rental values, the OECD says.

In a new analysis of the housing boom sweeping developed nations, the OECD also says the price of housing relative to incomes is 50 per cent higher in Australia than in other countries as a group. The Australian Institute of Health and Welfare said 1.7 million people were in "housing stress" in 2004, spending more than 30 per cent of their income on accommodation.

The report said average household debt had skyrocketed as a proportion of household disposable income. From 49 per cent of income in 1990-91, the debt ratio trebled to 143 per cent in 2004.

"The major component of this rise in household debt has been the even greater increase in borrowing for housing," the report said. "Such borrowing has grown more than four-fold in real terms since 1990."

The table below followed:

OVER- VALUATION OF HOUSES (% in 2004)

| Country | Our over-valued home | Housing debt (% of income in 2003) |

| Australia | 52 | 120 |

| UK | 33 | 105 |

| Ireland | 15 | 92 |

| Spain | 13 | 67 |

| Denmark | 13 | 188 |

| Canada | 13 | 77 |

| New Zealand | 8 | 129 |

| USA | 2 | 78 |

| Japan | -21 | 58 |

| Germany | -26 | 83 |

SOURCE: OECD ECONOMIC OUTLOOK.

There are two points of interest to us from these figures. Firstly they relate to 2004 when the property bubble had yet to peak in US and Down Under, yet even then the housing debt percentages for Australia and New Zealand (along with a few others) which I have highlighted are simply astounding. What they are now as the bubble continues is truly scary.

Secondly, compare the figures for the USA market which you no doubt know intimately, with those for Australia and NZ to put the relative size of these bubbles into perspective. Arguably the bubble Down Under is the greatest bubble of all.

Last week the Sydney Morning Herald published the following:

Capital city median weighted house prices

Date: January 8, 2008 Median weighted house prices, September quarter 2007

Australia $442,758

Sydney $538,400

Perth $455,000

Melbourne $431,000

Brisbane $383,500

The Real Estate Institute of Western Australia (REIWA) says Perth's house prices have continued to rise with the median house price in Perth now $466,000. The surge in Perth prices is being driven by the biggest mining boom for generations, perhaps ever.

Here's the rub guys: with an average median capital city price of over $450,000 for these four major Australian cities, the average wage for Australians, even though growing at over 5% per annum is $57,324 according to the Australian Bureau of Statistics report of November 2007. Now realise that for Sydney, Perth and Melbourne, median house prices are approaching 8 times average earnings. In Australia, interest on home loans that are owner occupied are not tax deductible so this becomes a straight forward equation.

The Median Multiple measures the ratio of the median house price to the median annual household income. This measure has historically hovered around a value of 3.0 or less, but in recent years has risen dramatically, especially in markets with severe public policy constraints on land and development and in markets with economically driven demand factors.

Housing access and affordability occupy a special place in the psyche of Australians, Kiwis and their politicians. We in the Great South Lands are hardwired that we have a right to own our homes. No politician dare do otherwise than support this universal view. As politicians blather about streamlining the development process to increase the supply of new homes, the nasty reality is that like all bubbles, it can't go on for ever. Markets are mean reverting to greater or lesser degree as even the elasticity of financial innovation has limits and the housing numbers we are discussing just don't work. The asset bubble mindset is based on the "greater fool" theory that there will always be a greater fool than you to pay an ever sillier price for that already overpriced house next year. Strangely the greater fool theory does work. Human greed and avarice knows no bounds and given the virtually unlimited availability of house purchase funding which created the bubble, the party will continue until someone takes the punch bowl away. These spoilsports are the other side of the equation, the investors, pension funds and banks who bought all of those oh so cleverly crafted mortgage packages which were reshaped from plain old mortgages to exotic investment grade bonds by the alchemy of Wall Street, and a significant group of others on the other side of the world that you will learn about another day.

Two Levers and some Sugar

It can be fairly said that the Down Under housing bubble came about as a happy coincidence of John Symond's securitisation initiative and Government policy. We have seen how changes to the capital gains tax regime set the stage for Symond. To this you have to add the "sugar"; the First Home Owners Grant. This joint Federal and State funding initiative provides a Government grant of $7000 for first home owners. The present policy originates from 2000 but a previous version provided $17,500 as a grant.

The scheme is not means tested and there is a mini industry of advisers processing applications for prospective purchasers. Ostensibly the rationale for the grant was to offset the additional costs of the Goods and Services Tax (GST) a catch all sales tax (on top of existing hidden sales taxes) introduced in 2000. Whatever the merits of the original policy, it is now a direct subsidy to new buyers whose target market is new homes.

Interest Rates

Then we add the two primary levers of fiscal management available to Government, interest rates and what I call "fundability". The Reserve Banks of Australia and New Zealand exercise a high degree of prudential supervision over the Four Pillars (same Four Pillars in NZ!). Effectively the Reserve Banks control mortgage rates through their official interest rate policies. Australia and New Zealand have seen high interest rates relative to US and European rates in the past decade for reasons presented as inflation targeting but really for another purpose. Inflation Down Under, in the things that matter but are not included in official calculations, is through the roof and certainly well into double digits. Costs in the basic needs of fuel, food and shelter (housing) would make an honest banker blush; but this is overcome through the simple use of hedonics. This should sound familiar to US readers.

Historically however interest rates are low. Outgoing Prime Minister John Howard based his appeal to young voters for the past decade on historically low interest rates and he should know! In a previous life when Howard was Treasurer in the Fraser Liberal Government, he pushed interest rates to 17.6%!!

Fundability

I use this term to describe not only liquidity but access to that liquidity. This is the big lever that is never discussed as Government spin doctors have hoodwinked the media into endlessly focusing on interest rates. A quarter percent rise or reduction in interest rates brings headlines. A quarter percent move on the average Down Under mortgage is $10 per week. With gas more than doubling in the past five years, a tank of petrol costing well over $100 and cigarettes at $13.20 a packet this is hardly earth shattering news. What really drives the housing market is the fundability. This combines easy access with innovation that reduces or eliminates the deposit gap and means as the RAMS web site says "You can have it now!" RAMS a listed public company in Australia and a latecomer to the mortgage party really summed up the mortgage marketing appeal with its website bellowing: "With a RAMS 100% Home Loan no deposit is required so you don't have to wait until you save and it makes it easy for you to buy your first home right now."

The unavoidable conclusion is that Government wanted and assisted in engineering this historic property bubble.

The New Zealand Herald of June 24, 2007 reported:

Median house prices in Auckland are now outstripping those in all of Australia's major cities, except Sydney and Perth.

Auckland's median of NZ$450,000 ranks ahead of Canberra on A$395,000 (NZ$436,000), Melbourne on A$380,000, and Brisbane on A$345,000.

And a new international housing affordability survey describes Auckland, Wellington and Christchurch as "severely unaffordable". Of 157 international locations, Auckland ranks 21st least affordable city in which to buy a home, with its median price almost seven times the median household income.

Melbourne ranks a few places behind on 23rd, with its median price 6.6 times the median income. Sydney, meanwhile, sits in 7th place with an affordability rating of 8.5. Its median house price is A$516,000. Christchurch is 31st on the list (with an affordability rating of 6) and Wellington is 47th (rating of 5.4). Los Angeles tops the list - with an affordability rating of 11.4.

Nationally, Australia and New Zealand have a housing affordability ratio of 6.6, compared with 5.5 in Britain and 3.7 in the United States. The internationally accepted standard for affordability is that the median house price does not exceed three times the median household income.

International Business Times lead with this headline today:

Australian property prices soar 10 percent in 2007: SYDNEY - The Australian property prices has inflamed 10 percent growth in 8-months period ended August 2007, an indicative results released by RP Data on Wednesday. The city with the most affordable homes, Adelaide, where the median house price is just $365,508, displayed the strongest growth in the 12 months to 31 July 2007 with overall property price increases of 17.2%.

During this same period, many other Australian cities also saw dramatic price rises, such as Brisbane (17.2%), Darwin (16%), Adelaide (17.2%), Canberra (11.8%), and Melbourne (11.4%)."

Sydney retains its mantle as Australia's most expensive housing market with a median house price of $561,199. This is followed by Perth ($508,140), Canberra ($475,554), Brisbane ($424,207), Melbourne ($407,544), Darwin ($385,506), and Adelaide ($365,508).

In a sign that patches of Australia are not doing so well, ABC news today reported that houses in the lower income western suburbs of Sydney are reported to be down 7% while prices in the more affluent inner northern suburbs are up 10-11.5% year on year. Is this the mortgage belt creaking? In general terms the Australian financial system is heavily regulated as well as being largely shielded from foreign competition and our regulators are deadly serious about their jobs. The excesses seen in US particularly regarding Adjustable Rate Mortgages with low teaser rates have not been apparent Down Under so the explosive trigger of interest rate resets is not apparent here.

Problems start to arrive

Jesse Livermore noted that "problems" had a host of relations; mothers, brothers, cousins and aunts. Some of these are already on our shores and others are coming to visit us soon.

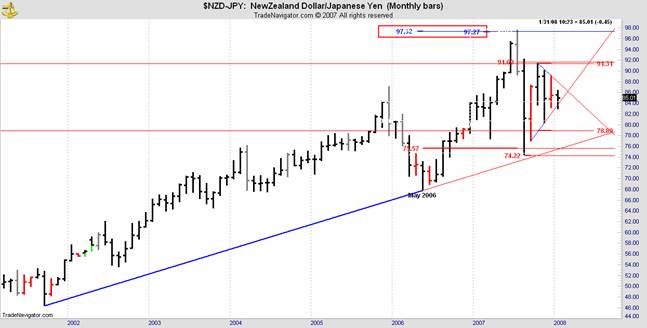

These are crucial charts for the fiscal health of the lands Down Under.

AUD-JPY Monthly

NZD-JPY Monthly

We have picked every turn in these charts for the past two and a half years (see Archives at www.thedanielcode.com ) and we watch them very closely indeed. So should you. The Danielcode will tell you when it is time to panic so I suggest you learn more about this enigmatic but oh so accurate fortune teller. Those of a nautical bent already have their "grab" bag in hand.

In these charts you can see not only what has been, but what is and will be again. The omens are not propitious!

In Part 2 later this week I will show you the "Today" picture Down Under and what is coming swiftly down the track, but start by remembering this unusual word "URIDASHI". It has played a big part in your life without you even knowing where it lived! It is going to be even more important in your future.

Copyright © 2008 John Needham