A long, long time ago...I can still remember; how that music used to make me smile. And I knew if I had my chance that I could make those people dance and, maybe, they'd be happy for a while.

As America goes; so goes the world!

In 1967 and most of 1968 I had the pleasure and opportunity of living in America and working for Tidewater Marine in Louisiana; quite an eye opener for a country boy from the sleepy rural town of Sutton Forest west of Sydney, Australia. My recollection of the four months I spent working in the corporate head office in New Orleans and with Tidewater's Attorneys were instructive to say the least as I learned how to drink Bourbon "Coonass style" and Cutty Sark whisky, fall in and out of love with those fabulous New Orleans gals and learn (when sober) to drive on the wrong side of the road.

But when John Laborde, Tidewater's President, commonly known as "bigfoot" gave me three days to recover from my Mardi Gras hangover and dispatched me to the heart of the offshore oil industry, Morgan City on Bayou Boeuf, I thought I had died and gone to heaven.

But when John Laborde, Tidewater's President, commonly known as "bigfoot" gave me three days to recover from my Mardi Gras hangover and dispatched me to the heart of the offshore oil industry, Morgan City on Bayou Boeuf, I thought I had died and gone to heaven.

Despised by the city dwellers, Morgan City was a rough and tough bayou town replete with tool pushers, divers, anchor handlers, tug drivers and the quirky individuals who made up the crews of the supply ships handling "mud", piping and every required piece of equipment as they drove down the canals in the predawn fog to supply the Gulf oil rigs.

Bars were everywhere along the levees and a fight a night was practically guaranteed. My drinking buddy Lanny Martin, was a heavily tattooed ex con known as the best winch man in the Tidex anchor handling fleet. He could fight almost as well as I could; he was twice my size and awesome with a bottle of whisky in his belly.

In those days it was seriously hard to get barred from a Morgan City bar (and perhaps still is), but to our endearing credit, Lanny and I were eventually barred from almost every bar in town. Soon, I found new friends in the town of Franklin, just north of Morgan City and moved into a real house as opposed to the ubiquitous trailers that were habitat de rigueur for junior Tidewater staff in Morgan City. My new friends, the Sheriff of Franklin, his family with particular emphasis on his lovely daughter Jeanette customarily spent the weekends at their holiday home on an offshoot of Bayou Boeuf so I became intimately familiar with levees, whisky and rye. Then, and for many years thereafter I mistakenly thought that Cutty Sark made their whisky just for me!

I often say that if I could have practiced the law in Louisiana I would never have left, but the requirements of another two years to become familiar with Louisiana"s Napoleonic Code were too daunting to a young man fresh out of law school in Sydney and busting to get on with life. Eventually sanity and sobriety prevailed and I returned to Sydney to begin my career in the boring world of corporate law, takeovers and three piece suits. My days on the bayou are amongst my fondest memories, so when, in the autumn of 1971 Don McLean's American Pie entered the collective consciousness of Americans, dwellers down under, ballad lovers everywhere and a motley collection of economists who went on to sinecures as senior officers, punters and players and even Governors of those historically flawed institutions, Governments and Central Banks I, better than anyone knew what he meant.

Being the good hearted people they undoubtedly are, the bankers wanted to emulate Don McLean and make the people dance and indeed they did and the people were happy for a while. The simple catalyst for happiness in this godless age of me, mine and have it now, is to treat the populace to extravagance without limit. "Of course you can have more toys sweetie (or a new car, house, music playing gizmo or mobile phone); here's the money, go and buy it. Even better tell them that you will "buy" it so long as they lend you the money."

And so assets morphed into credit and you could "have it now" if you could make the payments. Often just pretending you could make the payments was enough. Whether you could actually ever afford the asset became irrelevant as bankers drove the credit cycle to its ultimate illogical conclusion; but the people were happy for a while. And then the music stopped!

But February made me shiver With every paper I'd deliver. Bad news on the doorstep; I couldn't take one more step.

In a global economy geared to a one way bet on ever rising stock markets, housing and asset prices, the loss of momentum to continue the superior performance by the asset over its underlying loan is having a leveraged effect quite out of proportion to reality. In the UK, Times Online shrieked with a headline pronouncing the housing mortgage market as the worst in 30 years as mortgage approvals slumped almost 50% year on year, but despite the consistent theme of interest rates rolled out by talking heads and journalists, UK house prices are off only 5% and the 2 year fixed interest rate on home mortgages is still at just 6%.

In the US, Bernanke is actually looking prescient as apart from the bailouts of his mates on Wall Street, the savage cuts in official rates mean that all those mortgage resets are going to be done at much more affordable rates. Or are they? If you've been wondering what all the fuss in LIBOR has been about, consider that most of the ARMs are based on LIBOR, the London interbank overnight rate and not the US Fed rate.

In India's silicone valley, Bangalore, executive houses are off 20% and much the same in Japan. In New Zealand, the national median price was up from 7,500 in February to 9,000 in March - an increase of 1.6 per cent from 3,500 in March last year so the music is still playing in parts. As the ANZ Bank, one of the four pillars of banking Down Under drove house mortgage rates to 9.47% hastening the inevitable end of our particular version of the great housing boom, the Australian Stock Exchange revealed an unreported billion of margin lending against shares as disaster and scandal hit that niche industry where ANZ Bank and Merrill Lynch have been the key lenders.

So bye-bye, miss american pie, drove my chevy to the levee but the levee was dry. And them good old boys were drinkin' whiskey and rye singin', "this'll be the day that I die. This'll be the day that I die."

The ticking time bomb of credit impaired debt is now synonymous with the mortgage crisis. In the same way that Bear Sterns had to be rescued because of its counterparty contracts in derivatives, the mortgage debacle too has a big counterparty; Governments. After a decade of rising prices and its attendant opportunities for increased leverage, the reality of "living within your means" has become a forgotten concept.

The ticking time bomb of credit impaired debt is now synonymous with the mortgage crisis. In the same way that Bear Sterns had to be rescued because of its counterparty contracts in derivatives, the mortgage debacle too has a big counterparty; Governments. After a decade of rising prices and its attendant opportunities for increased leverage, the reality of "living within your means" has become a forgotten concept.

Mortgage markets all over the world are like the levees; dry!

Not because of any lack of liquidity as central banks insist and not because of interest rates which are low by historic standards but simply because so many bought assets they could never realistically afford. The great credit beast has come full circle and is beginning to bite. Note that I say "beginning". Despite assertions to the contrary, "The Great Moderation" as NZ Reserve Bank boss Alan Bollard calls the global deleverage is only in chapter 1. The world has waxed fat on an historic property boom and now it must endure the waning. Property cycles are long and slow. If you're looking for a bottom, start thinking in terms of 7-8 years. That is the average time for property cycles.

So we can keep the obfuscations and forecasts simple. The biggest bubble of all time is the housing bubble and there are more infected than just the US. UK and Spain and Ireland played the game with gusto. Australia and New Zealand are still in denial and Hong Kong and Japan were also infected as are parts of India. Ambrose Evan-Pritchard at the Times Online gives us an elegant global summary:

America, of course, is already in recession although the cascade of defaults, business closures, and job losses has barely begun. Japan is in recession too, according to Goldman Sachs;. Britain, Ireland, Spain, Italy, and New Zealand, are tipping into housing slumps and demand implosions of varying severity. Ontario and Quebec have stalled. Canada's growth is the weakest in fifteen years, hence the half point cut by the Bank of Canada yesterday. Australia is on borrowed time, whatever the price of coal and iron ore. Household debt is 175pc of disposable income, up in La La Land with England, Ireland, Denmark, and the Dutch. The wholesale funding market for mortgages that underpins this nonsense remains frozen. Together these countries and regions make up roughly 45pc of the global economy, and over half global demand. Europe will suffer 40pc of the entire 0bn global losses stemming from the credit crunch. Euro banks alone will lose 3bn (compared to 4bn for the US). "Loss recognition will need to catch up," said the IMF. The report contains a grim chapter on what may happen along the vast arch of over-heating silliness from the Baltics to the Black Sea, funded by Austrian, Swedish, German, Belgian, and Italian banks.

So this all sounds rather fun, don't you think. Highly predictable and well foreseen for a long time by many. The only part of this story that is surprising is that those who would not see were the central banks and their masters, governments. Those who had the obligation to control the bad behavior of the naughty children with the money bags. The ultimate counterparty to housing losses is government. If the problem gets big enough, and it will, governments will be blamed and governments will fall. Like all defaulting counterparties, government action be it through the Fed and Bank of England accepting ever lower quality paper for repos, or forcing GSEs to push more money at the wealthy through increased jumbo loans or crying crocodile tears at the slow pace of mortgage work outs, they are only postponing the day of reckoning.

The bills must eventually be paid and some are coming due in unexpected ways.

US retail giant Wal-Mart is rationing rice sales to protect dwindling supplies as the global price skyrockets and producers such as Australia struggle to keep up with demand. The drastic move is the first time that food rationing has been introduced in the US. Growing appetites in China and India, drought in Australia and pests in Vietnam have contributed to the rice shortage and soaring prices. While Americans suffered some rationing during World War II for items such as petrol, light bulbs and stockings, they have never had to limit consumption of a key food item. In Britain, where Wal-Mart owns Asda supermarkets, rice is being rationed by shopkeepers in Asian neighborhoods to prevent hoarding. The Times 04/24/08.

All actions have consequences. For 20 years I have been amazed that successive governments have promoted irrigated cotton farming and rice growing in Australia by making water available at near zero cost and funding the infrastructure required for large scale irrigation. Why successive governments have subsidized the growing of rice, the thirstiest of all crops (7 parts water for 1 part rice), in the driest continent on earth is a mystery ranking up there with the US decision to subsidize the uneconomic conversion of corn into ethanol!

The consequence is that Australia's largest river system the Murray-Darling is effectively destroyed.

Dry rivers; dry levees and dry mortgage lenders.

Them good old boys all over the world are drinking whisky and rye in desperation as all the dry levees become apparent.

And as the flames climbed high into the night To light the sacrificial rite, I saw satan laughing with delight The day the music died.

For those unfortunates seduced by the "buy and hold" mantra beloved of fund managers the world over (what else are you going to say when the tail falls out of the markets), the hangover from the great credit party is just beginning. US and international markets have actually held up splendidly in the face of what is so obviously coming down the track.

This is the International Market Index. At this week's close it is only 11.25% off its October 2007 top. At its January low made near its first Danielcode target at 857 it was down 21.7%, not nearly enough to reflect the wealth destruction that is wending its way through the myriad barriers erected by desperate governments and their functionaries. The rectangle at 672 is the likely target for this index in the current corrective cycle. Four months down from the high hardly rates as a correction..

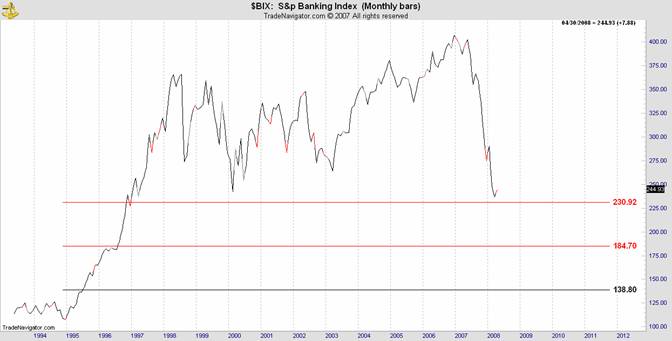

The following chart is the S&P Banking Index. The 230.92 Danielcode retracement level which is presently providing support is exactly the same level to which the International Market index and others will eventually gravitate. You don't need to be a rocket scientist or even an economist to know that absent systemic Fed intervention this index would be at least one and probably two degrees lower. That too will come. As the driver of capital weighted indices in US we can extrapolate this assumption to other indices.

Below is my favorite toy. As a reflection of investors hope and optimism it is marvelous indicator. UK Telegraph on 14 April ran the following analysts note: Goldman Sachs and Wells Fargo warn 'delusional' investors on stocks. Wall Street faces the growing risk of an equities bloodbath in coming months as the credit crunch spreads to the wider economy and earnings crumble, according to a pair of grim reports issued by Goldman Sachs and Wells Fargo.

This chart might restore a sense of perspective. The dot com correction went almost exactly to the Danielcode retracement at 760. This level is called the 4th iteration or simply level 4. It is the same level that is holding the banking index at present and the same level that predicts 672 as the most probable level for the IMI to attain.

As a minimum we can assume this level will be reached by the S&P in its initial correction. Globally the great mortgage rort is many times larger and has far greater consequences than the dot com bubble so realistically we should be thinking of a level 4 correction as a minimum number for the S&P. Does this all sound reasonable now?

This is what it is going to look like. Ignore the timeline, my freehand skills are limited:

1097 is the minimum number we should expect for a purely corrective move. More dire possibilities lie below. Don't get too excited. This market isn't going to crash. They are not allowed to now. We don't want to scare the horses or even the punters! It will just be a slow relentless grind punctuated by spectacular rallies. Great trading for those who can see. We are just 6 months from the high. Have a look where the market was 6 months from the 2000 top. How did that turn out?

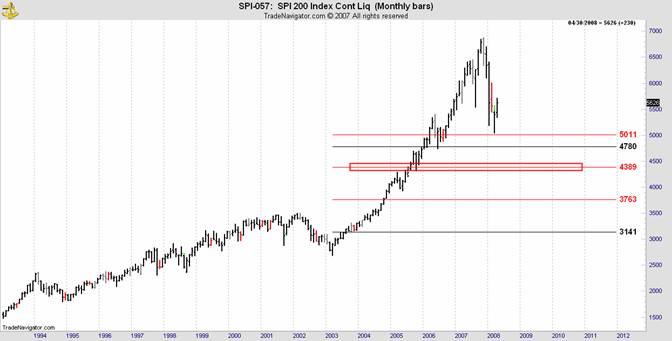

Closer to home, this is the monster you get with billion in margin lending in a relatively small market. This is the Australian SPI 200:

The margin lending was unregulated and unreported so it has come as a surprise to punters to see that company directors lining up for margin loans to gobble up those generous bonuses in stock options have faced margin calls and lost control of their own companies as the lenders rushed to liquidate the margined shares before the inevitable injunctions were launched.

Showing their greater expertise in margin call liquidations, Merrill Lynch dumped the lot in 3 days whilst the ANZ, trying to put a positive spin on its corporate behavior, solemnly intoned that it would offer its seized stock over a six month period so as not to pressure the market. The natural response to this ongoing stupidity was to launch a raft of legal injunctions as bargaining chips if nothing else, and a swage of Attorneys from Brisbane to Perth duly obliged.

Studying the movements of the SPI is a very exact science best undertaken by those with experience in fortune telling from the contents of chicken gizzards, a pastime admired and relied on in Roman times, but a casual observation shows this market bouncing from its Daniel target one degree lower than the S&P which it apes. That adjustment means that we should see the first leg of the bear market reach 3763 as a minimum. Then we'll see some real margin calls!!

Commodities

Corn gapped up into its Daniel number at 570 and has spent the month wandering. There are much higher targets above if required.

continued

Wheat is showing off its prowess in recognizing its Daniel number sequence as it ticks off all the DC numbers.

Oil stopped its relentless charge at 118.98 just ticks from its next sequential Danielcode target and has spent the week having a breather. There are two degrees of DC targets at 122 and more above if that resistance gives way.

Rice is putting in a serious blow off move. I published this chart in "Rice!.The New Gold" for Financial Sense on 9th April with Rice sitting at its Daniel number of 2142. Look at the price movement in the past fortnight! There are more DC numbers above 2521.

Gold and Silver

Gold is back on its best behavior making turns diligently at its DC numbers

as is Silver

DX We have been following the DX in some detail for Financial Sense. In February I showed readers the two degrees of Danielcode support at 70.40 and this index obliged by pausing its headlong rush to oblivion just above the DC price level at 70.70. In "Hostage Gold!" (see FSO archives) I detailed the inverse correlation of Gold and Silver to DX.

Now, mainstream media seems to be getting the idea with this from Bloomberg today: April 25 (Bloomberg) --

The dollar rose the most in two days against the euro since December as traders increased bets the Federal Reserve will stop cutting interest rates while the European economy showed signs of a slowdown. ``We have gone from a situation where the market was excessively pessimistic about the U.S. to perhaps a little bit complacent about what comes next, and that has benefited the dollar,'' said, head of global currency strategy at Bank of America Corp. in New York.

You know that is nonsense. DX stopped where it did because it again recognized its DC number, as it has all the way from the top. That's a much better reason!

The future direction of Oil, Gold and Silver are linked to the next phase in DX. Thursday's high was at its Daniel number and Friday's high is at the next number in the sequence. The DC levels in the following chart were posted at the Danielcode Online on Sunday so my clients knew what to expect.

To assist clients with the task of trading the Daniel number sequence, I introduced them to our new T.03 proprietary turn indicator only this morning. I nominated today as a turn day for DX, Gold and Silver among other markets on the daily charts. I might be wrong by the time you read this but it is looking good so far!!

S&P The great entertainer has spent the week playing with its DC retracement of a minor range on the daily chart. The black line at 1398 is a common ratio particularly in equity indices (Dan 12:7..and swore by him that liveth forever that it shall be for a time, times, and a half.)

Whilst scrupulously observing its Daniel number sequences on the 151 minute chart.

Have you noticed how the same Danielcode ratios are equally definitive on monthly, weekly and daily charts and shorter time periods. It is a universal market controller.

I invite you to visit the Danielcode Online to learn more about this enigmatic market definer.

But not a word was spoken; The church bells all were broken. And the three men I admire most: The father, son, and the holy ghost, They caught the last train for the coast The day the music died.

Copyright © 2008 John Needham