Last month Atlantic writer Derek Thompson shared some interesting data on how much the American economy has prospered over the last century. Using Census Bureau data, Thompson showed how the percentage of income an average American household spends on various goods.

What stuck us as especially interesting was the fact that in 1901 roughly 43% of the household budget was for food. By 2003 that had shrunk to only 13%. During that same period the yield on an acre of corn went from roughly 25 bushels per acre to 150 bushels per acre thanks to mechanization, cheap and plentiful fertilizers, insecticides, herbicides, and seed genetics.

By coincidence the ‘Age of Oil’ was essentially launched in 1901 with the discovery of the prolific Spindletop well drilled in South Texas. The energy provided by natural gas and crude oil have had an incredible impact on the productivity of the agricultural sector – with some expert studies indicating Western agricultural practices utilize 10 calories of petroleum energy to produce one calorie of food (other global agricultural regions are not so energy intense).

Prior to the Age of Oil the energy input was much closer to the energy output of the food produced. Experts claim that without hydrocarbons the agricultural sector could only feed 3 billion people – less than one-half the current global population of 7 billion.

Knowing the historical relationship between energy and agriculture products, and the relentless year after year growth in global demand for both crude oil and grains, it did not surprise us to find the extremely high correlation between crude oil prices and the United Nation’s FAO global food index since 2000 (charts below courtesy the Financial Times). The FAO food index is a global basket of food commodities.

The coefficient of determination (‘r squared’) between the price of Brent crude and the FOA food index for the last twelve years is 0.932 - meaning that 93.2% of the change in the price of food as measured by the FAO food index is statistically ‘explained’ by the change in the price of oil during this period.

The coefficient of determination (‘r squared’) between the price of Brent crude and the FOA food index for the last twelve years is 0.932 - meaning that 93.2% of the change in the price of food as measured by the FAO food index is statistically ‘explained’ by the change in the price of oil during this period.

This is an extremely high level of statistical correlation over a statistically significant time frame.

With correlations so high one of the questions analysts have asked is whether the elevated level of crude oil prices will continue – or if they will plunge in the latter half of 2012 as some have forecast?

Trends Point to Elevated Oil Prices

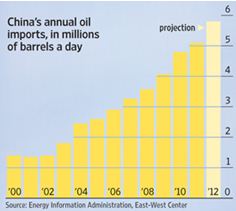

China's crude-oil imports have jumped to near-record levels in March leading some analysts to speculate that the country is filling its’ expanding strategic petroleum reserves. Some claim China's growing thirst for oil could underpin already-high crude prices, pushing the country's oil imports above market expectations.

Oil Demand Strong. China announced its oil imports reached 5.57 million barrels a day in March, the third-highest month on record and a rise of 8.7% from the year-ago month. For the quarter, China's crude imports rose 11% from the year-ago quarter, a much stronger pace than full-year 2011's increase of 6%, according to China's General Administration of Customs.

Oil Demand Strong. China announced its oil imports reached 5.57 million barrels a day in March, the third-highest month on record and a rise of 8.7% from the year-ago month. For the quarter, China's crude imports rose 11% from the year-ago quarter, a much stronger pace than full-year 2011's increase of 6%, according to China's General Administration of Customs.

The Financial Times notes that “China has been increasing its oil purchases even though prices have soared, a rare occurrence for a country that usually steps out of the market when prices are high”.

Meanwhile Japan will be without nuclear power for the first time in nearly 50 years when the last operating reactor shuts down in May. The incremental impact on global demand for crude oil and natural gas will be substantial since nuclear power generated 28% of electrical power in Japan prior to last year’s accident. Utilities have already maximized LNG-fired electricity output, leaving crude oil and fuel oil to meet additional needs.

The Financial Times reports that oil traders believe that Japan’s nuclear cutback could add between 450,000 and 800,000 barrels a day to world demand for crude and fuel oil – a significant quantity in a market where substantial supplies remain offline due to disruptions caused by the Arab Spring.

The International Energy Agency forecasts that some nuclear power plants will be restarted in August to meet peak electrical demands seen during the summer months – but they had forecast that plants would be back online last August and last February, neither of which was correct. Some experts claim Japan may be nuclear free for a number of years – further straining the global crude oil supply and demand balance.

Oil Supply Flat. Meanwhile the Economist published an interesting chart and article last month on the long term global crude oil production trends. While global metals and food output has climbed 30% or more since 2002 the output of crude oil has only expanded by only around 10% - and has been flat for the last seven years.

Oil Supply Flat. Meanwhile the Economist published an interesting chart and article last month on the long term global crude oil production trends. While global metals and food output has climbed 30% or more since 2002 the output of crude oil has only expanded by only around 10% - and has been flat for the last seven years.

The Arab Spring continues to adversely impact global oil production and investments. Higher food prices and the uncertainty involved in building new governments will not be conducive to investments which might increase production any time soon.

Add into the mix the expropriation of exploration and production rights, and massive fines imposed for relatively minor offshore spills, imposed by certain South American countries and the outlook for increased capital expenditures in frontier areas is suspect.

Last, Bill Powers of the Powers Energy Investor, has noted the amount of excess crude oil productive capacity available to meet growing global demand has reached alarmingly low levels. Every year the global demand for crude oil increases by around one to two percent while existing fields deplete. Production needs to grow every year just to meet incremental demand increases. When excess production capacity falls to current levels Bill notes that oil prices tend to become very volatile and unstable – but tend to trend upward.

Last, Bill Powers of the Powers Energy Investor, has noted the amount of excess crude oil productive capacity available to meet growing global demand has reached alarmingly low levels. Every year the global demand for crude oil increases by around one to two percent while existing fields deplete. Production needs to grow every year just to meet incremental demand increases. When excess production capacity falls to current levels Bill notes that oil prices tend to become very volatile and unstable – but tend to trend upward.

Summary. We expect crude oil and food prices to remain highly correlated – and up-trending – over the next several years. If our forecast is correct it should be a very positive environment for companies in both sectors.