Good or Bad Economy?

Is the economy strong or weak? The safe answer is – both. GDP and median income growth have remained weak, but employment and consumer spending are healthy. Manufacturing and construction hiring and wage gains have been anemic while leisure, healthcare, and business services have been energized.

Since the real estate crash bottomed in 2008 we have witnessed a below average growth cycle when combing weak industrial infrastructure with strong consumer-oriented production comprising our GDP. Historic declines in interest rates and debt service costs have sponsored a consumer spending cycle that after 7 years has returned most metrics of consumption back to previous peaks.

The Good

The good news is the slow and steady economic growth backed by about $12 trillion in global central bank asset purchases (printing money) has encouraged consumers to return to restaurants and bars and travel at very robust levels.

Car sales led by pickup trucks and SUVs have led the consumption wave. Per capita car and truck sales are well below their former peak, but nominal sales are still near prior peaks and growing at record rates. While it makes sense that this 7-year auto consumption boom has likely plateaued, the slack in the economy leaves room for another leg up should the global recovery finally reach normal rates of growth. Our Federal Reserve is keenly aware it can’t allow a recession to occur in the US, so an extended easy credit consumer spending wave may continue.

Capital investment in transportation manufacturing is leading the durable goods growth cycle.

Global air travel led by China, US and India passenger volumes has also supported a lofty transport industry. More air travel has spurred massive passenger plane investments adding to a high-octane transportation sector. The future here should remain elevated as air travel is expected to double over the next 20 years led by much faster passenger growth rates in China, US and India.

When we isolate “consumer” oriented capital investment it becomes clear that manufacturing geared to the consumer has been expanding at rapid rates similar to the 90s up until 2003. Another 5 years of growth to match the last up cycle may be needed to bring our economy to healthy GDP growth rates and over-heating.

The Bad

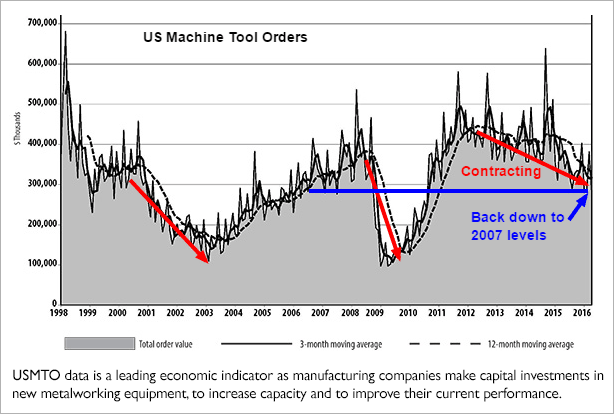

An industry we are personally connected to has a very different perspective than the optimistic charts above. Even in nominal dollars there has been almost no growth over the past 17 years in machines used for metal fabrication by US companies. The contraction since 2012 after a post-2008 dead cat bounce recovery highlights the constriction in basic industrial companies budgeting for capital expenditures. The sharp 4% decline in durable goods orders reported today will maintain the cloud of pessimism pervading our general industrial economy and machine tools in particular.

It has been decades since machine tool orders have been this persistently bleak. The strong bounce from depression-level orders in 2010-2011 merely brought the industry back from the brink only to be dashed again since 2012 as metals and then oil prices collapsed. 2016 may mark almost 5 years of sharp contraction in this barometer of industrial health. A US or global recession at this vulnerable juncture would be devastating. If oil falls beneath and copper under .93, watch out for a GDP recession, deflation of stock market earnings and massive efforts by central banks to buy even more assets. For now, we continue to expect a modest expansion cycle to continue and edge machine tool orders back to a very modest growth on trailing 12-month comparisons.

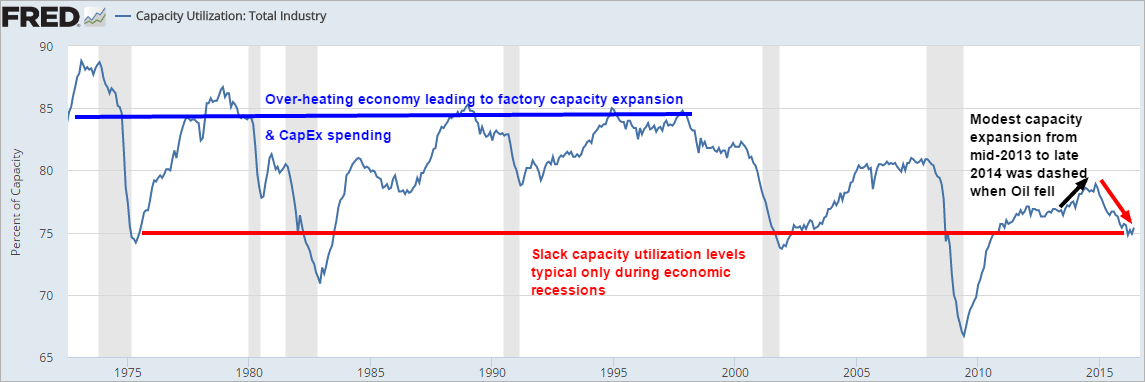

Historically, almost all US expansion cycles lead to consumption growth that usurps 80 to 90% of manufacturers' capacity causing a rise in capital expenditures and factory expansion. We might have to compare with previous “recessions” to find the equivalent weakness in total industrial manufacturing utilization rates. Without above trend demand growth, we should expect capacity to shrink until utilization rates finally rise closer to 80%. A further decline under 75% would likely signify a quarter or 2 of GDP contraction despite a buoyant consumer services sector.

Energy and mining have been major culprits depressing overall industrial production and capacity usage despite strong consumer durable spending. Perhaps the good news here is that oil and metal prices have had a bounce after the headwinds of almost zero new orders were reached in the 1st quarter. Coal has been destroyed politically (look for a bounce here should the GOP win), oil fracking has been derailed economically and mining is still struggling to put its bottom in the rear view mirror.

Machines servicing the agricultural economy have also added insult to injury with sharp oversupply contractions coinciding with the collapse of oil and crop prices since 2014. Weather and supply will eventually conspire to send crop prices back up and deliver new order growth. Will La Nina elevate crop prices in 2017-2018? Cycles would favor a 2016 base with a major up cycle peak due by the end of the decade.

When looking at “all” machinery orders it still indicates a modest recession in the basic industrial sector of our economy since 2014. Manufacturers have responded with massive cost cutting, outsourcing, inventory and head count shrinkage that began in 2008. Cost cutting has reached levels in 2016 that will lead to bankruptcy, selling assets and permanently eliminating capacity unless the current headwinds become tailwinds. If oil, copper and crop prices begin a new leg above their 2015 highs, then new industrial durable goods orders would finally break sharply upwards along with above trend GDP growth >3%.

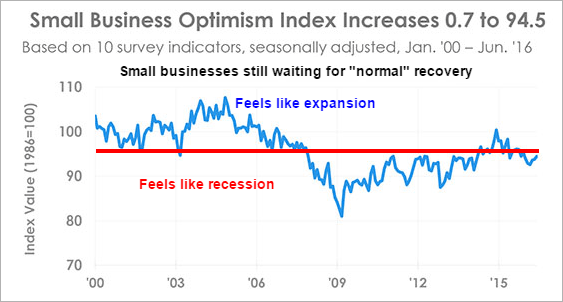

When grading this economic recovery since 2009, the consumer surveys would give it an average rating at its peak while small businesses would say we are still teetering on the cusp of a recession. Once we see the Michigan consumer sentiment and small business optimism levels return to 100+, then we can declare that a full recovery has arrived. For the next year we only see a 2%+ GDP supporting improved margins, but lackluster revenue growth. For a leading indicator, we continue to encourage watching price trends in basic commodities such as oil and copper until global growth is on more solid footing.