All eyes will be on the Fed this week, as they deliberate whether to raise rates for the first time in nearly a decade. The decision will be arduous, to say the least, as there has been a growing divergence in fundamental indicators, and global markets have already tightened conditions on the Fed’s behalf.

If you forced me to place a wager one way or the other, I would lean towards no rate increase. But I’m no oracle so let’s walk through some of the data the Fed will be looking at and you can make up your own mind.

First we’ll discuss the areas of strength in the economy that warrant a rate hike, then we’ll go over the arguments in favor of leaving rates unchanged.

The most recent revision to GDP showed that the US economy grew at a 3.7% rate during the second quarter, a pace that is at the higher end of the spectrum of post-financial crisis growth. While you can argue the ramifications of a slower first quarter and perhaps a weakening outlook (which we’ll get to), the fact is that the US is currently producing more goods and services than ever before in history.

One of the supposed weak spots in the economy that has grabbed headlines is the lack of business investment. Again, looking back at the second quarter, the level of investment rose nearly 4% from year ago levels. This outpaced GDP growth over the same period, and indicates that businesses are investing in future growth and production.

The health of the private sector can be seen from a number of angles. Job growth continues to be robust with jobless claims (a very reliable leading indicator of an approaching recession) near all-time lows, job openings at all-time highs, and the economy adding an average of over 200,000 jobs per month. More people are currently employed than ever before in US history.

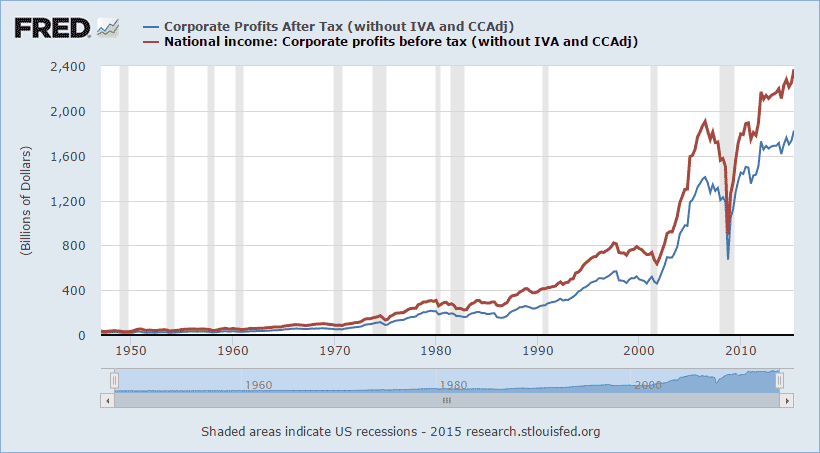

Corporate profits, both before and after tax, also rose to their highest levels ever during the second quarter. Taxes collected on corporate income set a new record as well.

The list goes on.

Personal income is up over 4% from year ago levels. When you consider that there is relatively little inflation, real personal income is also up over 4% from year ago levels. As far as real disposable personal income, it is at an all-time high.

Consumer spending, a key driver of the economy, is up 3.5 percent year-over-year, and it too is at record levels.

Both consumer sentiment (University of Michigan) and consumer confidence (The Conference Board) remain in uptrends.

The yield curve is still positively sloped, indicating a healthy economic environment with associated recession probabilities (over the next year) at roughly 3%.

With all these positives, you might be convinced that a rate hike is a done deal. Before you jump to that conclusion, let’s consider the opposing arguments. These come in two broad categories. The first is with regard to the Fed’s dual mandate, and the second involves the contrast between current conditions vs. future conditions.

As you well know by now the Fed’s congressional mandate has two components: promote maximum employment and achieve price stability (defined as 2% inflation).

With the labor market continually improving and the unemployment rate at a post-recession low of 5.1%, it would initially appear that the “maximum employment” part of the mandate has been met. A deeper look however, reveals two areas of weakness.

The U-6 rate, a broader measure of unemployment that includes discouraged and underemployed workers, remains somewhat elevated when compared to pre-financial crisis levels. It currently stands at 10.3%.

The other issue is wage growth. With all the improvement in labor markets since the financial crisis, average weekly earnings have grown by roughly 2% per year since the recession ended. This is a soft figure and points toward continued slack in the labor market.

There are no line-in-the-sand targets when it comes to the employment component of the Fed’s dual mandate, and so while these two items could be better, they are probably not enough to derail a Fed rate hike on their own.

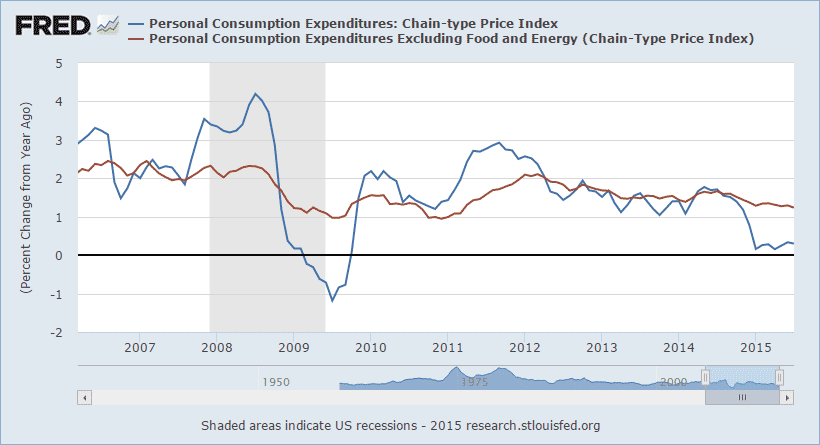

The larger issue, in my opinion, comes down to the Fed’s price stability mandate - achieving 2% inflation. The Fed has been unable to achieve target inflation levels since 2012 (chart below).

Fed commentary has suggested a willingness to raise rates with inflation below target, with the caveat that inflation remains on a path to reach 2%. In the chart above, you can see that headline inflation (blue line) is flat-lining near zero, and core inflation (the Fed’s preferred measure) is at 1.2% and falling.

If we look for signals earlier in the production process, we find that producer prices are actually 0.8% lower than one year ago, with core producer prices also in a downtrend and only up 0.6% for the year.

Import prices also plunged lower last month and are currently down 11.4% year over year.

In my mind these figures highlight the deflationary pressures that exist around the globe, and are one of the primary reasons we could see the Fed keep rates unchanged.

On a more subjective note, both the IMF and the World Bank have urged the Fed to delay a rate increase until at least 2016, as they believe it may have negative global repercussions for many emerging market countries.

Earlier in the article I mentioned global forces having already tightened monetary policy for the Fed. What I was referring to is the strength of the dollar. As the dollar strengthens, it lowers demand for our exports, and also lowers the cost of imports. Both these factors suppress domestic manufacturing and act negatively upon net exports, one of the four components of GDP. A stronger dollar also carries with it deflationary forces, as commodity prices fall.

In theory, a rise in short-term interest rates, even a minuscule one, makes the dollar more attractive. This could exacerbate the problems of a strong dollar which have already been felt heavily in some markets, particularly energy.

Then there is the issue of China and global growth. The Fed is supposed to be focused on the US economy, but they and everyone else understand that the global economy is struggling. Growth is slowing or almost nonexistent for many of our trading partners, and this acts as a headwind for the US economy. It adds additional deflationary pressures and also increases the risk of further dollar appreciation as other countries seek to devalue their own currencies in order to drive growth.

Throughout history the Fed has typically tightened economic policy for one reason, to slow an overheating economy. This time is different. Instead of tightening monetary policy to suppress above trend growth and inflation, it is being done to “normalize” interest rate policy.

I could see the Fed going either way with their decision next week. On one hand it’s counterintuitive to have crisis-level interest rate policies in place when the economy is robust, and on the other, global growth is slowing and the Fed’s congressional dual mandate is not being met, nor appears on track to be met in the near future.

Wrapping things up, I think it’s important to note that if the Fed does hike rates next week, we are still going to be at crisis-level low interest rates. A quarter point will affect market psychology a heck of a lot more than it will affect underlying economic fundamentals.

This hike has been telegraphed for so long that we might actually see the opposite reaction many are expecting. It’s conceivable that US markets will take a rate hike in stride, as it will reduce uncertainty in the marketplace and demonstrate the Fed’s confidence in the economy. The pullback that we saw recently also may have extinguished a lot of the selling pressure that was pent up in anticipation of the hike.

The preceding content was an excerpt from Richard Russell's Dow Theory Letters. To receive their daily updates and research, click here to subscribe.