In recent days, numerous central bank bureaucrats have given us hints that another round of pump priming is more or less imminent. It started with John Williams, president of the San Francisco Fed who mused about 'QE without a limit'. The FT reported:

“The US will make little progress tackling high unemployment before 2014 unless the Federal Reserve eases policy further, one of the central bank’s leading officials has warned in the run-up to a meeting next week where the option of “QE3” will be on the table.

The comments by John Williams, president of the Federal Reserve Bank of San Francisco, show how the weak economy is pushing the central bank towards action to support growth.

[…]

If the Fed launched another round of quantitative easing, Mr Williams suggested that buying mortgage-backed securities rather than Treasuries would have a stronger effect on financial conditions. “There’s a lot more you can buy without interfering with market function and you maybe get a little more bang for the buck,” he said.

He added that there would also be benefits in having an open-ended programme of QE, where the ultimate amount of purchases was not fixed in advance like the $600bn “QE2” programme launched in November 2010 but rather adjusted according to economic conditions.

“The main benefit from my point of view is it will get the markets to stop focusing on the terminal date [when a programme of purchases ends] and also focusing on, ‘Oh, are they going to do QE3?’” he said. Instead, markets would adjust their expectation of Fed purchases as economic conditions changed.“

(emphasis added)

Mr. Williams, so the FT, is thought to be 'close to the center of gravity' on the FOMC. We take this to mean that he has the helicopter pilot's ear.

So if indeed the Fed were to embark on 'open-ended QE' that is predicated on developments in the vaunted 'economic data', or putting it differently, is dependent on recent economic history (a method also known as 'driving forward with one's eyes firmly fixed on the rear-view mirror'), what happens if said data fail to improve?

Will the Fed then just keep printing forever and ever? As an aside, financial markets are already trained to adjust their expectations regarding central bank policy according to their perceptions about economic conditions. There is a feedback loop between central bank policy and market behavior.

This can easily be seen in the behavior of the US stock market: recent evidence of economic conditions worsening at a fairly fast pace has not led to a big decline in stock prices, as people already speculate on the next 'QE' type bailout. This strategy is of course self-defeating, as it is politically difficult for the Fed to justify more money printing while the stock market remains at a lofty level.

Of course the stock market's level is officially not part of the Fed's mandate, but the central bank clearly keeps a close eye on market conditions. Besides, the 'success' of 'QE2' according to Ben Bernanke was inter alia proved by a big rally in stocks. Such increases in stock prices are seen as a spur to spending, as the perceived wealth of stockholders increases. In the view of Bernanke and his colleagues, spending is what it's all about. The central bank chief holds that we can consume ourselves to prosperity. It follows from this that one should also be able to print and deficit spend oneself to prosperity, but oddly enough, it hasn't worked thus far. A reason to revisit long-cherished beliefs? Not at all! We must 'do more' of what hasn't worked thus far.

Following an unexpected earnings miss by market bellwether AAPL, the stock market had a perfect opportunity to sell off, but went sideways instead. Mr. Hilsenrath's piece I the WSJ (see further below) may well have provided the rationale - click for better resolution.

The remarks of Williams were then given another boost by Sarah Bloom Raskin, who announced the the upcoming FOMC meeting would be used to 'debate the benefits of a new bond buying plan'.

“Federal Reserve Governor Sarah Bloom Raskin said the Fed next week will debate whether to begin a program to speed economic growth and reduce unemployment through large-scale purchases of bonds.

Another round of Treasury purchases “is something that will be debated in the upcoming FOMC meeting,” Raskin said yesterday in response to audience questions after a speech in Boulder, Colorado, referring to the Federal Open Market Committee.

“It will be debated against the backdrop of the dual mandate” to ensure stable prices and maximum employment.“

(emphasis added)

We once suggested that the writing of the bureaucratese FOMC statements could be delegated to something akin to the postmodernism generator. Just put a collection of stock phrases into a computer program that then prints them out at random in grammatically correct sentences. Mrs. Bloom-Raskin already sounds as if she were connected to one.

However, the final confirmation that something is in the works came yesterday when Jon Hilsenrath of the WSJ penned an article entitled 'Fed Moving Closer to Action'. Everybody knows by now that Hilsenrath is the media mouthpiece employed by the Fed. Kind of like the Oracle of Delphi, only with greater accuracy. In fact, Western media have become like the Pravda of the Soviet Union. They are no longer engaged in journalism, they simply relay vetted messages from government officials. The astonishing thing is that they no longer even try to deny it – see this recent article in the NYT, in which it is openly admitted that in order to 'retain access', every word emanating from the presidential campaigns or the White House has to be 'approved' by the apparatchiks before it sees print. Anything even remotely controversial is duly blotted out. These days, if you really want the truth ('pravda' ironically is the Russian word for 'truth'), you apparently actually have to watch Russian TV stations (such as RT) and read Russian newspapers.

Anyway, Hilsenrath writes:

“Federal Reserve officials, impatient with the economy's sluggish growth and high unemployment, are moving closer to taking new steps to spur activity and hiring.

Since their June policy meeting, officials have made clear—in interviews, speeches and testimony to Congress—that they find the current state of the economy unacceptable. Many officials appear increasingly inclined to move unless they see evidence soon that activity is picking up on its own.

Amid the recent wave of disappointing economic news, conversation inside the Fed has turned more intensely toward the questions of how and when to move. Central bank officials could take new steps at their meeting next week, July 31 and Aug. 1, though they might wait until their September meeting to accumulate more information on the pace of growth and job gains before deciding whether to act.

Fed officials could take some actions in combination or one after another. Fed Chairman Ben Bernanke, in testimony to Congress last week, listed several options under consideration, including a new program of buying mortgage-backed or Treasury securities, new commitments to keep short-term interest rates near zero beyond 2014 or an effort to push already-low benchmark short-term interest rates even lower.“

(emphasis added)

It seems pretty clear from all this that mortgage backed bonds will be the vehicle of choice (see also comments by Alan Blinder in an op-ed at the WSJ, were he discusses the methods the Fed could use to get bank credit inflation going again). This is probably the preferred option because of the perceived shortage of highly rated collateral in the market. Moreover, it doesn't smack so much of the Fed financing the government, even though technically speaking it only ever buys already existing treasury debt from third parties – albeit sometimes within days of it coming into existence.

To the extent that the Fed buys securities from non-banks, deposit money in the system will increase directly. If it buys securities only from banks, it may well end up mainly increasing excess bank reserves deposited at the Fed. However, banks are avid buyers of treasuries themselves, so the funds do indirectly tend to support government spending (it is easy for fractionally reserved banks sitting on a mountain of excess reserves to create deposits in favor of the government).

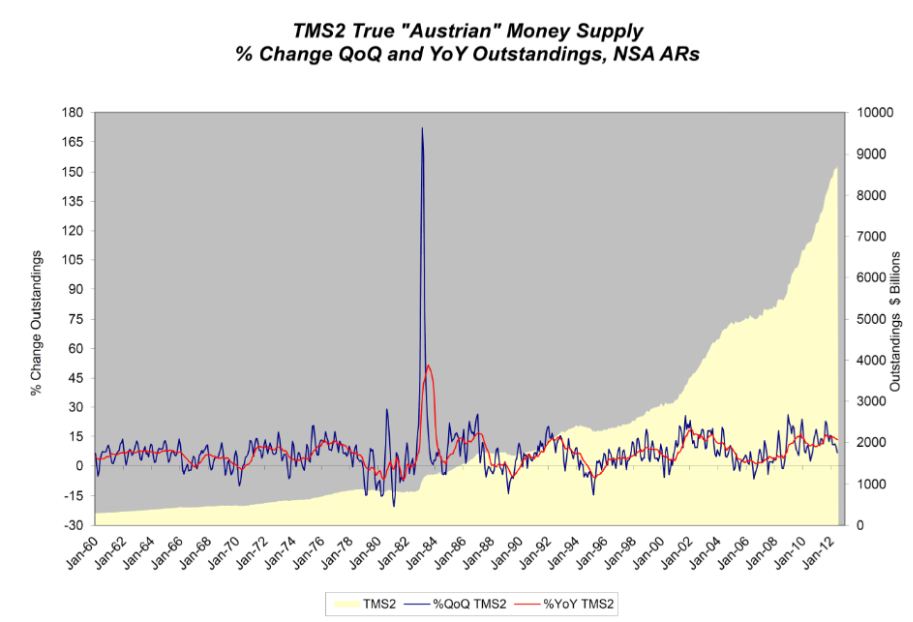

Given that the only goal of more 'QE' can be to goose the money supply (failing that, it would have zero effect), the question should be: is there too little money in the economy? Judge for yourself:

The US broad true money supply TMS-2, via Michael Pollaro. It has increased from .3 trillion at the beginning of 2008 to .719 trillion as of the end of June 2012 - click for better resolution.

Of course the above is a bit of a trick question. The money supply can never be 'too small'. Any size of money supply will be as good as any other to render the services money is supposed to render. Numbers in accounts are really meaningless per se – it is not important how much money there is, but what it can buy. Today, a dollar buys 97% fewer goods and services (a rough estimate) than 100 years ago. Evidently if things that cost 0 today were to cost as they did in the year of the Fed's founding, we could make do with a far smaller money supply.

Increasing the money supply however always has ill effects, even though a temporary 'sugar high' for the economy can often be bought that way. If increasing the money supply were a good thing, then everybody should be allowed to contribute to the exercise, since one can never have enough of a good thing. We should all have the right to run our private printing presses – after all, what difference can it possible make whether the Fed prints the money or the commercial banks create new deposits, or everybody gets in on the act? If additions to the money supply are desirable, why should Joe Six-Pack's privately printed notes not also be desirable?

It is by posing such simple questions that one can immediately unmask the absurdity of the Fed's activities.